Gold’s long-term bull market is increasingly being driven by a force larger than inflation, interest rates or geopolitical tensions: the world’s growing debt burden.

That is the central thesis of Sprott’s latest market outlook, which argues that investors are witnessing the later stages of a decades-long debt cycle in which rising government borrowing, persistent deficits and mounting interest costs are beginning to undermine confidence in sovereign debt markets.

As governments accumulate liabilities faster than economies can grow, policymakers face difficult choices between fiscal austerity, higher inflation, financial repression or some form of debt monetization, the asset manager said.

In such an environment, gold’s role changes, as the report highlights. Rather than simply serving as an inflation hedge, the metal becomes a store of value independent of governments and financial systems.

Sprott argues that the world is moving toward a regime where preserving purchasing power matters more than generating yield, creating a favorable backdrop for gold over the long term.

Central banks are voting with their reserves

According to Sprott, one of the strongest signals supporting gold comes from central banks themselves.

Official sector purchases reached 244 tonnes during the first quarter of 2026, extending a buying trend that has persisted for several years. At the same time, some countries have reduced holdings of US Treasuries and other sovereign debt instruments to raise liquidity during periods of market stress.

Sprott highlights Turkey’s recent actions as an example. Faced with rising energy-import costs, the country liquidated most of its Treasury holdings while largely retaining gold reserves through swap transactions rather than outright sales. The distinction is significant. Treasuries were treated as transactional assets that could be sold when cash was needed, while gold remained core collateral.

The broader trend suggests central banks increasingly view gold not as a speculative asset but as a strategic reserve. Amid growing geopolitical tensions, sanctions risks and concerns about long-term currency stability, gold offers something sovereign bonds cannot: an asset with no counterparty risk.

This sustained central-bank demand has also helped establish a durable floor beneath the gold market, with purchases often accelerating during periods of price weakness.

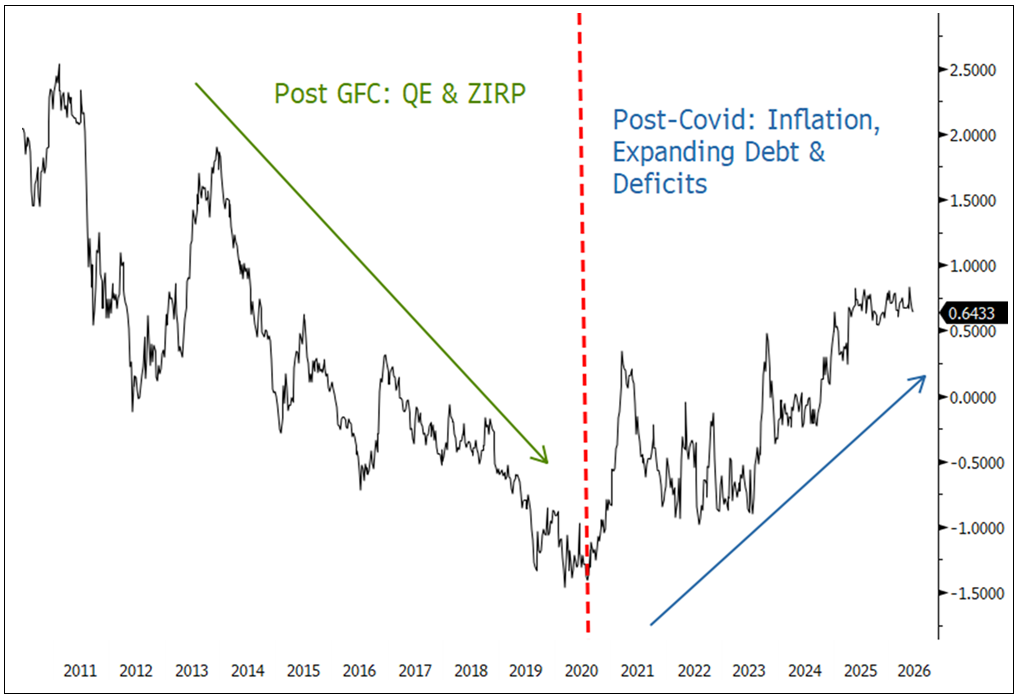

Bond markets are flashing warning signs

The report argues that the most important development in global markets is occurring not in gold but in government bonds.

Across major economies, yields have climbed sharply despite efforts by central banks to ease monetary conditions. In the United States, long-term Treasury yields have risen to levels not seen since before the global financial crisis, while similar moves have occurred across Europe, Japan and other developed markets.

Traditionally, lower policy rates helped pull bond yields down. That relationship is beginning to weaken. Investors are increasingly demanding higher compensation for inflation uncertainty, growing debt issuance and concerns about fiscal sustainability.

U.S. 10-year Treasury term premium, weekly. Source: Sprott

U.S. 10-year Treasury term premium, weekly. Source: Sprott

The US illustrates the challenge. Federal debt has climbed to roughly 120% of GDP, while annual deficits remain near 5% of GDP and are projected to increase further. Interest payments on the debt are approaching $1 trillion annually and continue to rise as governments refinance obligations at higher rates.

According to Sprott, investors are beginning to focus less on central-bank policy and more on the long-term ability of governments to manage debt loads. The result is rising term premiums, higher borrowing costs and growing questions about the future role of sovereign bonds as safe-haven assets. As confidence in debt-backed assets weakens, demand for hard assets such as gold tends to strengthen.

Gold’s structural bull case remains intact

While gold faces short-term headwinds from rising yields and periodic liquidity pressures, Sprott believes the larger forces supporting the metal remain firmly in place.

The report describes an emerging environment characterized by fiscal dominance, where governments become increasingly constrained by debt levels and rising interest costs. Policymakers may be forced to prioritize financial stability and debt management over strict inflation control, creating conditions that historically lead to currency debasement and negative real interest rates.

At the same time, mine supply growth remains limited while central banks continue to absorb a significant share of newly available metal. This combination of constrained supply and steady official-sector demand strengthens the market’s underlying fundamentals.

For Sprott, the current gold market is not simply reacting to inflation or geopolitical headlines. It reflects a broader reassessment of monetary assets in a world where debt continues to expand faster than confidence in the financial system.

If that debt cycle continues along its current path, gold’s role as a store of value may become increasingly important—not only for central banks, but for investors seeking protection from the long-term consequences of rising deficits, growing debt burdens and the gradual erosion of purchasing power.

In the short term, gold remains subject to market conditions such as inflationary pressures from the US-Iran war. On Tuesday, the metal extended its decline to about $4,230/oz., once again erasing its gains for the year.