一个潜在错杀区域 260415

注:本文原发于跨资产星球东八区4月13日的内容。部分内容已删减,完整版可在文末获取。

过去的一段时间是科技板块过去 50 年最弱的一段相对收益期之一,这一定价结果主要源于两个新问题:1)hyperscaler 的 ROI 持续被市场质疑,2)AI disruption risk 正在重写很多科技子行业的终局假设。

Over the recent period, tech has gone through one of its weakest stretches of relative performance in the past 50 years. This pricing outcome is mainly driven by two new questions: 1) the market keeps questioning hyperscaler ROI, and 2) AI disruption risk is rewriting terminal-state assumptions across many tech sub-sectors.

不止如此,华尔街近期最火热的讨论还包括了对‘Magnificent 7 能否永远跑赢市场’的系统性怀疑,资方的恐惧集中聚集在担忧买到 AI 时代的 Kodak、IBM、Nokia、Blackberry 这种被新技术浪潮直接碾碎商业模式的旧巨头。软件行业尤其如此,过去被长期增长信仰和低贴现率支撑的终值价值,如今第一次被认真打折。

More than that, one of Wall Street's hottest recent debates has been the systemic doubt over whether the Magnificent 7 can outperform the market forever. Capital's fear is increasingly concentrated on buying the AI-era equivalents of Kodak, IBM, Nokia, or Blackberry, old giants whose business models were crushed outright by a new technology wave. Software is especially exposed: the terminal value that used to be supported by a long-duration growth belief and low discount rates is now, for the first time, being seriously marked down.

结果就是大科技内部相关性下降、分化上升:

The result is that correlations inside big tech have fallen while dispersion has risen:

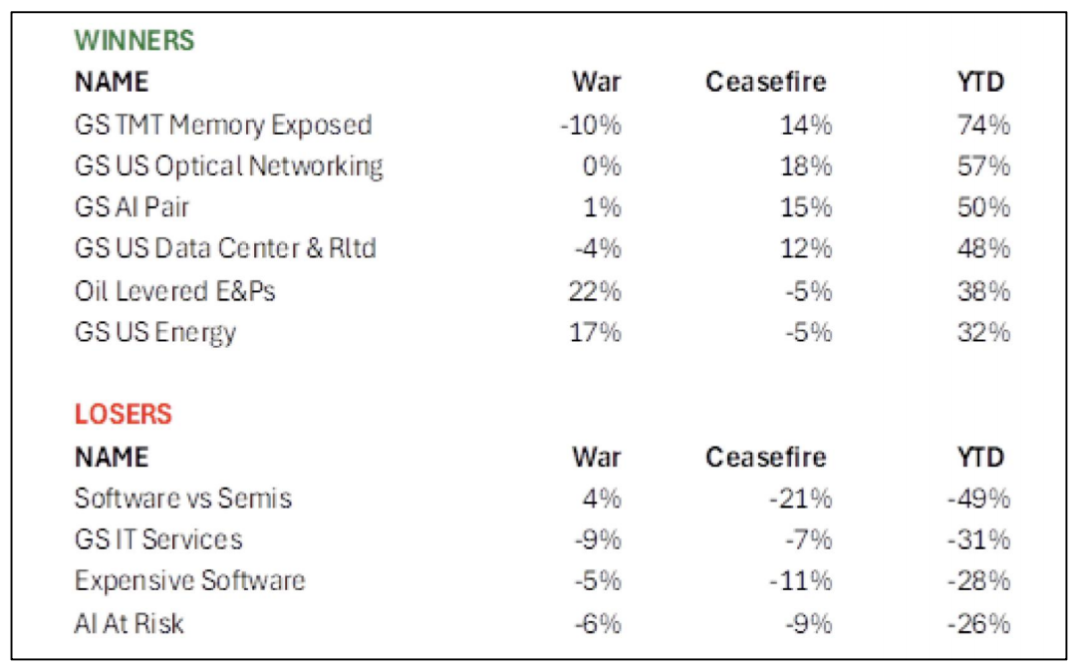

图:不同主题交易篮子的战中/停火/年初至今表现

上图是一个分篮子的表现统计。光网络、数据中心,存储与内存这些主题,不仅 YTD 表现最好,战争期间回撤也相对有限,停火后反弹又最快(很明显是当前市场最愿意在回调中继续加仓的主线),对应地,软件、IT 服务、以及广义的 AI at risk 方向,在冲突期间被明显加空,停火后甚至继续遭遇更强的做空。也就是说,科技内部的一个存在至今的趋势是铲子们的确定性和实际应用上的不确定性,可以预期的是,这种情况在可见视野范围内仍会持续。

The chart above is a basket-by-basket performance breakdown. Themes such as optical networking, data centers, storage, and memory not only have the best YTD performance, but also saw relatively limited drawdowns during the war and then rebounded the fastest after the ceasefire. Clearly, these are the market's preferred core positions to keep adding on pullbacks. By contrast, software, IT services, and the broader AI-at-risk complex were heavily shorted during the conflict and kept facing even stronger selling after the ceasefire. In other words, a persistent trend inside tech has been certainty in the picks-and-shovels segment versus uncertainty around end applications. This dynamic is likely to remain in place for the visible future.

但与此同时,被做空的一批科技,和科技之外更广义成长股里有没有潜在错杀对象?

At the same time, are there potential names being indiscriminately sold off among the shorted parts of tech and the broader growth universe outside tech?

可能也的确是有的...

There probably are...

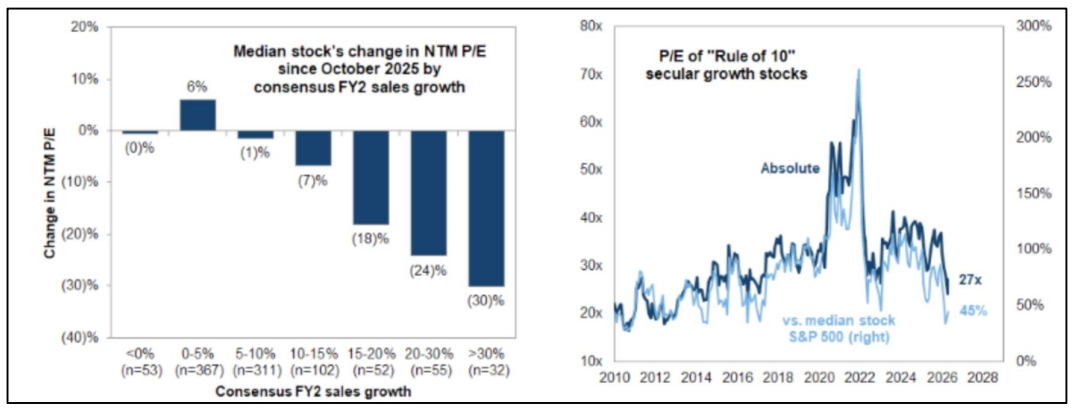

以 GS 的 Rule of 10 篮子为例,其中,在剔除最被做空的软件之后,那些非软件成长股的中位数当前 P/E 29x,相对标普中位数溢价约 53%,同样已经接近过去十年区间底部;而市场一致预期 2027 年销售增速仍是标普中位数的 3 倍。

Take GS's Rule of 10 basket as an example. After excluding the software names that have been hit the hardest on the short side, the median P/E of those non-software growth stocks is now 29x, about a 53% premium to the S&P median, which is likewise close to the bottom of the past decade's range. Yet the market still expects their 2027 sales growth to be roughly 3 times the S&P median.

那些真正高质量的非软件成长股,估值已经降了不少,但成长性并没有塌掉:

Those truly high-quality non-software growth names have already seen their valuations come down a lot, but their growth has not collapsed:

图:体现出的是一个潜在错杀的广义成长击球区域

如果未来只是温和增长放缓而非深度衰退的宏观背景成立,那么 secular growth 中尤其是非软件成长股的部分将开始重新具备配置吸引力,这部分做的,是从冲击叙事切到有真实增长、 有供给约束、且没被 AI 直接替代的事情。

If the future macro backdrop turns out to be one of only a mild growth slowdown rather than a deep recession, then the secular-growth complex, especially the non-software growth segment, will start to regain allocation appeal. What this part of the market is doing is shifting away from pure shock narratives toward businesses with real growth, supply constraints, and no direct AI substitution risk.

部分已经验证增长,但估值明显降温的资产,

Some assets have already validated their growth, yet their valuations have clearly cooled,

在当前时间点其预期回报已经要好于继续追高少数核心高位对象:

and at the current point in time their expected returns already look better than continuing to chase a small number of crowded core winners at elevated levels:

(注意进退有据,不要抢跑抄底)!

(Stay disciplined on entries and exits; do not rush to catch the bottom.)

图:AXON(日线图,截至 260413(UTC+8))

图:CVNA(日线图,截至 260413(UTC+8))

图:SMCI(日线图,截至 260413(UTC+8))

图:DASH(日线图,截至 260413(UTC+8))

图:ANET(日线图,截至 260413(UTC+8))

完整内容订阅链接:

免责声明:文章中的所有内容仅代表作者的观点,与本平台无关。用户不应以本文作为投资决策的参考。

你也可能喜欢

AlchemistAI(ALCH)24小时内波动47.9%:SolanaAI代理社交热度与成交量激增共振

阿斯麦 ASML26Q1财报电话会全文

标普警告:银行对交易巨头风险敞口飙升,美国金融生态系统陷入“内生性脆弱”

XCX(XelebProtocol)24小时内波动51.3%:交易量放大下的低流动性价格震荡