Written by: Crypto Miao

“Choosing the right corporate structure is crucial for Web3 companies going global. It not only optimizes tax burdens, but also reduces risks and enhances global operational flexibility.”

Whether leveraging a single-entity structure to enjoy low tax rates or establishing a multi-entity structure based on business needs, a well-designed structure can significantly enhance a company's international competitiveness and help it thrive in the Web3 ecosystem.”

Due to their decentralized nature, Web3 companies face unique legal, tax, and operational challenges in international expansion.

Choosing the right corporate structure not only helps companies operate in compliance, but also optimizes tax burdens, reduces risks, and enhances market flexibility to adapt to different regional legal frameworks, technical infrastructures, and market demands.

I. What is an Overseas Structure

An overseas structure refers to the organizational structure and management model that a company builds during globalization, aiming to coordinate global resources, adapt to the characteristics of different markets, and achieve efficient cross-border operations.

The design of an overseas structure directly affects a company's global competitiveness and operational efficiency. It requires consideration not only of equity structure, but also future structural adjustments, tax costs, intellectual property management, financing activities, and overall maintenance costs, among other factors.

II. Types of Overseas Structures

Tax optimization is a key consideration in the choice of Web3 corporate structures, as the global tax framework's impact on digital assets is becoming increasingly significant. When building holding companies overseas, Hong Kong, Singapore, and BVI are popular choices.

(1) Single-Entity Structure

1. Hong Kong

Hong Kong implements a low-tax regime, mainly including profits tax, salaries tax, and property tax, without levying VAT, business tax, or similar taxes. For corporate income tax, the portion of annual profits not exceeding HKD 2 million is taxed at 8.25%, and the portion exceeding HKD 2 million is taxed at 16.5%. Dividends received from Hong Kong offshore companies with a shareholding of more than 5% are exempt from overseas dividend tax.

Hong Kong has signed Double Taxation Agreements (DTA) with about 45 countries and regions worldwide, covering key markets such as Mainland China, ASEAN, and Europe. This extensive network creates broad tax planning opportunities for companies, especially in reducing withholding tax on cross-border dividends and interest.

2. Singapore

Singapore's corporate income tax rate is 17%, slightly higher than Hong Kong. However, Singapore's tax regime is relatively friendly to technology and R&D enterprises, allowing companies to enjoy multiple exemptions and deduction policies. In addition, Singapore exempts overseas dividends and capital gains (subject to relevant conditions).

Furthermore, Singapore offers a range of tax incentives, such as the Regional Headquarters (RHQ) and Global Trader Programme (GTP), providing more tax planning possibilities for companies.

Singapore has signed DTAs with over 90 countries worldwide, covering major global economies, including China, India, and the EU. This provides companies with a very broad scope for tax planning, especially in reducing withholding tax on cross-border dividends and interest.

3. BVI (British Virgin Islands)

BVI, with its zero-tax regime, strong privacy, and flexible structure, has become the preferred offshore jurisdiction for global cross-border investment, asset protection, and tax optimization, especially suitable for holding companies and business scenarios in the crypto industry.

BVI does not levy corporate income tax, capital gains tax, dividend tax, or inheritance tax, resulting in extremely low tax costs.

BVI companies do not disclose shareholder and director information and can further conceal the ultimate controller through Nominee services, ensuring business privacy and asset security.

As internationally recognized offshore entities, BVI companies are widely accepted by major global financial centers (such as Hong Kong, Singapore, London, etc.), making it easy to open accounts in multinational banks and efficiently conduct international payments, trade settlements, and capital operations.

Main tax rate comparison:

(2) Multi-Entity Structure

Adopting a multi-entity structure allows for more effective tax planning. Domestic companies can set up one or more intermediate holding companies in low-tax countries or regions (usually Hong Kong, Singapore, BVI, or Cayman) to invest in the target country. By leveraging the low tax rates and confidentiality of offshore companies, the overall tax burden can be reduced, company information protected, parent company risks diversified, and future equity restructuring, sales, or IPO financing facilitated.

Case 1: Intermediate Layer Control: China → Singapore → Southeast Asia Subsidiary (e.g., Vietnam)

The Chinese parent company invests in Vietnam through a Singapore holding company. Singapore has signed bilateral DTAs with both China and Vietnam, allowing the withholding tax rate on dividends to be reduced to as low as 5%. Compared to direct Chinese control of a Vietnamese subsidiary, the rate can be reduced by 50% (the China-Vietnam DTA sets it at 10%).

As an intermediate company, the transfer of Singapore company shares is usually not subject to capital gains tax; if the Vietnamese subsidiary shares are transferred directly, Vietnam's capital gains tax (20%) may apply. The Singapore structure also aligns better with the transaction habits of European and American investors, improving asset sale liquidity.

Additionally, the Singapore company can serve as a regional headquarters, managing subsidiaries in different countries, making it easier to attract international investors or spin off for IPOs. Singapore's developed financial market allows the holding company to issue bonds or obtain international bank loans, reducing financing costs.

Case 2: VIE Agreement Control: BVI → Hong Kong → Operating Company

Due to strict regulation and high operational risks for the Web3 industry in some regions, a "VIE" (Variable Interest Entities) agreement control framework can be adopted, with a BVI company holding a Hong Kong company that invests in the operating company (as in the cases of Alibaba, Tencent Music, New Oriental, etc.). The offshore holding company controls the operating company through a layered VIE agreement structure.

The BVI company, as the top-level holding entity, is exempt from capital gains tax on future equity transfers and protects the founders' privacy.

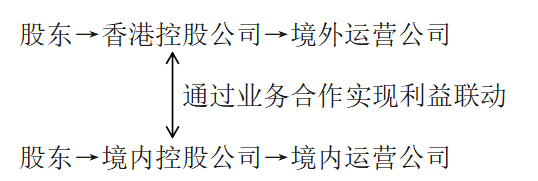

Case 3: Parallel Structure of Domestic and Overseas Companies:

The parallel structure of domestic and overseas companies can be applied in situations where, due to market and regulatory uncertainties, or for reasons such as financing, geopolitics, qualifications, or data security, different domestic and overseas companies need to collaborate on different business segments. For example: Mankun Research | Web3 Entrepreneurship, is the "front shop, back factory" model of Hong Kong + Shenzhen compliant?

Overall tax rates are lower. Overseas companies can choose to register in tax-favored regions (such as Hong Kong, Singapore, Cayman Islands, etc.), which usually have lower corporate income tax rates or capital gains tax exemptions than domestic regions. Through business cooperation, profits can be reasonably allocated, enjoying tax deductions in various locations and reducing the overall tax burden.

Independent operation of domestic and overseas entities. Under a parallel structure, domestic and overseas companies operate as independent legal entities, each subject to the tax jurisdiction of their respective locations. This means both companies can pay taxes according to local tax laws, avoiding the issue of global income consolidation due to equity association.

III. Conclusion

Choosing the right corporate structure is crucial for Web3 companies going global. It not only optimizes tax burdens, but also reduces risks and enhances global operational flexibility. Whether leveraging a single-entity structure to enjoy low tax rates or establishing a multi-entity structure based on business needs, a well-designed structure can significantly enhance a company's international competitiveness and help it thrive in the Web3 ecosystem.