Saia (NASDAQ:SAIA) reported fourth quarter 2025 sales that surpassed expectations

Saia (SAIA) Q4 2025 Earnings Overview

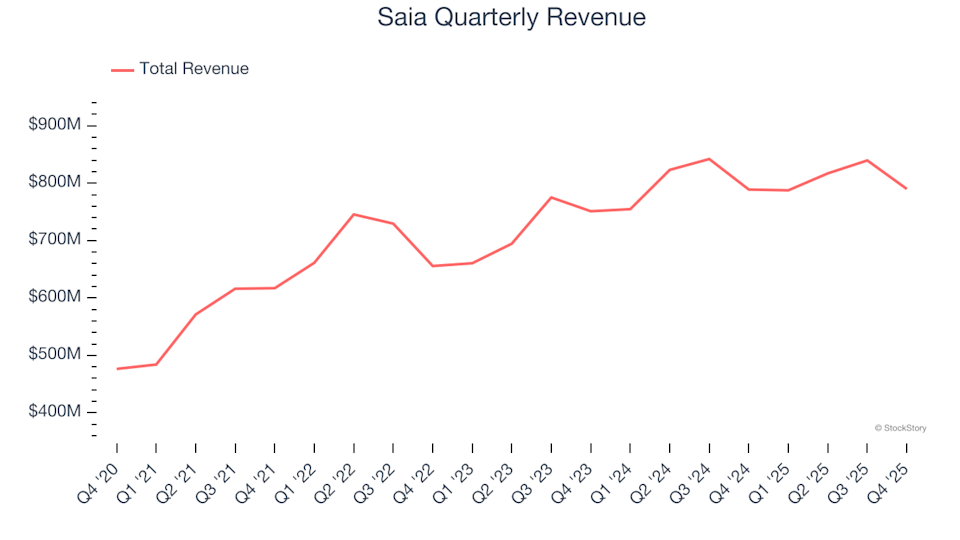

Saia, a leading freight transportation and logistics company listed on NASDAQ (SAIA), released its financial results for the fourth quarter of 2025. The company surpassed revenue forecasts, posting $790 million in sales, which remained unchanged compared to the previous year. However, its GAAP earnings per share came in at $1.77, falling 7% short of analyst predictions.

Wondering if Saia is a good investment right now?

Q4 2025 Performance Highlights

- Total Revenue: $790 million, exceeding analyst expectations of $777 million (flat year-over-year, 1.7% above estimates)

- GAAP EPS: $1.77, missing the consensus estimate of $1.90 by 7%

- Adjusted EBITDA: $127 million, below the projected $135.3 million (16.1% margin, 6.1% shortfall)

- Operating Margin: 8.1%, a decrease from 12.9% in the same period last year

- Free Cash Flow: $37.48 million, a significant improvement from -$2.90 million a year ago

- Sales Volume: Down 1.5% year-over-year (compared to a 10.1% increase in the prior year’s quarter)

- Market Cap: $10.88 billion

Fritz Holzgrefe, Saia’s President and CEO, remarked that the company’s core business performed as anticipated, though the quarter was negatively affected by unexpected costs related to prior-year accidents, resulting in approximately $4.7 million in higher self-insurance expenses. Excluding these costs, he emphasized the team’s dedication to customer service and operational discipline, highlighted by a record-low claims ratio of 0.47% for the quarter.

About Saia

Saia (NASDAQ:SAIA) shifted its focus from selling produce to specializing in freight transportation, providing logistics solutions across the industry.

Revenue Trends

Examining a company’s long-term revenue trajectory is key to understanding its business strength. While any company can have a strong quarter, sustained growth is a better indicator of quality. Over the past five years, Saia achieved a robust 12.2% compound annual growth rate in sales, outperforming the average for industrial companies and demonstrating strong customer demand for its services.

Although Saia’s long-term growth has been impressive, recent results show a slowdown. Over the last two years, annualized revenue growth dropped to 5.9%, falling below its five-year average and suggesting a deceleration in demand.

In the latest quarter, Saia shipped 1.46 million tons. Over the past two years, the company’s tonnage grew at an average annual rate of 5.6%, closely matching its revenue growth and indicating stable pricing strategies.

Recent Revenue and Outlook

For Q4, Saia’s revenue of $790 million was flat compared to the previous year but still surpassed Wall Street’s estimates by 1.7%.

Looking forward, analysts project a 4.2% increase in revenue over the next year, a modest pace that suggests potential challenges in demand for Saia’s offerings.

If you’re interested in emerging opportunities in the tech sector,

Profitability: Operating Margin

Operating margin is a crucial profitability metric, showing the percentage of revenue remaining after covering core operating expenses. It allows for comparison across companies regardless of their debt or tax situations.

Over the last five years, Saia has maintained an average operating margin of 14.6%, positioning it among the more profitable companies in the industrial sector. This is particularly notable given its relatively low gross margin, which is largely determined by its business model. High operating margins in this context reflect strong management and operational efficiency.

However, Saia’s operating margin has declined by 3.8 percentage points over the past five years, raising concerns about rising costs. Ideally, revenue growth should have led to better economies of scale and improved profitability.

In Q4, Saia’s operating margin dropped to 8.1%, down 4.8 percentage points from the previous year. This decline outpaced the reduction in gross margin, suggesting increased spending on areas like marketing, research and development, and administrative expenses.

Earnings Per Share (EPS) Analysis

Tracking long-term EPS growth is important for assessing whether a company’s expansion is translating into higher profitability for shareholders.

Saia delivered an impressive 12.8% annual EPS growth rate over the past five years, mirroring its strong revenue performance and indicating consistent per-share earnings as the business scaled.

However, over the last two years, annual EPS has declined by 15.3%, underperforming the 5.9% revenue growth in the same period. This drop is primarily linked to a shrinking operating margin, rather than changes in interest or tax expenses.

For Q4, Saia reported EPS of $1.77, a decrease from $2.84 in the same quarter last year and below analyst expectations. Despite this short-term miss, the focus remains on long-term EPS growth. Wall Street forecasts Saia’s full-year EPS to reach $9.52 in the next 12 months, representing a projected 12.2% increase.

Summary and Investment Considerations

Saia’s latest quarter saw the company outperform revenue expectations, but it fell short on EBITDA and EPS. The stock price dropped 3% to $393.96 following the earnings release. While this quarter’s results were underwhelming, a single report does not define the company’s overall quality. When evaluating whether to invest, it’s important to consider Saia’s long-term business fundamentals and valuation, not just recent performance.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

CandyBomb x ROBO: Trade futures to share 340,000 ROBO!

OPNUSDT now launched for pre-market futures trading

Join the BGB holders group—unlock Spring Festival Mystery Boxes to win up to 8888 USDT and merch from Morph

Trading Club Championship (Margin)—Trade to share 58,000 USDT, with up to 3000 USDT per user!