Sterling or Granite: Which Infrastructure Stock Offers a Better Investment Opportunity?

U.S. Civil Construction: Market Overview

Ongoing robust public investment and steady private sector demand are key drivers in the U.S. civil construction sector, fueling projects in transportation, water infrastructure, and major site developments. Within this environment, Sterling Infrastructure, Inc. (STRL) and Granite Construction Incorporated (GVA) have emerged as prominent players. Both companies are well-positioned to capitalize on multi-year project pipelines, thanks to their focus on selective bidding, margin improvement, and operational excellence. Their strategies center on disciplined project selection and execution, aiming for sustainable growth and profitability.

Sterling Infrastructure: Growth Drivers

Headquartered in Texas, Sterling Infrastructure has seen continued strength in demand for its services across transportation, utilities, and mission-critical site development. The company’s E-Infrastructure segment, which includes data centers, manufacturing, and distribution facilities, has been a significant growth engine, aligning Sterling with high-potential markets driven by digital transformation and industrial expansion. Sterling’s emphasis on complex, large-scale projects and reliable execution has contributed to consistent operational performance as infrastructure spending remains strong.

In the third quarter of 2025, Sterling’s revenue from data center projects surged by over 125% compared to the previous year, reflecting heightened demand for hyperscale facilities. The company reported a signed backlog of $2.6 billion, a 64% increase year over year. When including anticipated awards and future phases of ongoing megaprojects, Sterling’s total potential work exceeds $4 billion, providing solid visibility for future revenues in critical and industrial sectors.

Despite these strengths, Sterling faces some challenges, such as slower activity in residential markets and delays in permitting for certain large projects, which could impact project timing. Additionally, the complexity of projects and competitive bidding environments introduce execution risks, especially as labor availability and input costs fluctuate, potentially affecting margins if schedules shift.

Looking forward, Sterling expects its robust pipeline in data centers, e-commerce, and manufacturing to drive growth through 2026 and beyond. With major multi-phase projects progressing and clients maintaining investment commitments, the company is well-positioned to continue expanding while enhancing revenue stability.

Granite Construction: Strategic Positioning

Based in California, Granite Construction benefits from steady public infrastructure spending, supported by transportation funding and a disciplined approach to project selection. The company targets high-quality projects in its core markets, prioritizing contract structures that foster collaboration and minimize execution risks. Granite’s vertically integrated construction and materials operations provide greater control and margin potential on large infrastructure projects.

At the close of the fourth quarter of 2025, Granite reported a record Construction and Materials Portfolio (CAP) of $7 billion, marking a 31.6% increase from the previous year. Nearly half of this CAP consists of best-value projects, indicating a strategic shift toward contracts that offer higher margins and reduced risk. The construction segment’s revenue grew 14% year over year to $940 million, reflecting successful project execution and improved portfolio quality. This expanding CAP ensures strong revenue visibility as infrastructure funding remains favorable.

However, Granite’s involvement in large, complex public projects brings execution and timing uncertainties. Factors such as weather, changes in federal infrastructure policy, and varying project completion rates can influence short-term revenue trends. The company also continues to integrate recent acquisitions and focus on maintaining consistent margins.

Looking ahead, Granite anticipates ongoing revenue growth and margin improvement, supported by its high-quality project mix, investments in materials, and prudent capital allocation. With reliable public funding and a growing portfolio of collaborative projects, Granite is positioned to sustain its operational momentum into the next year.

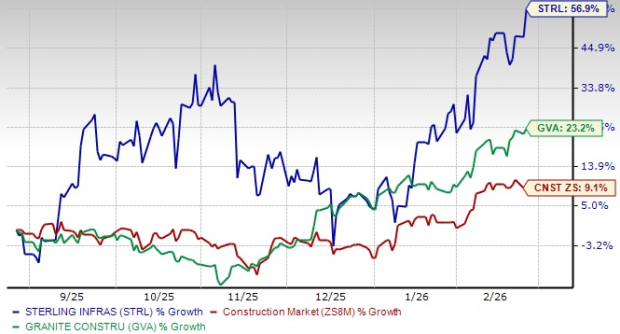

Stock Performance and Valuation Comparison

Over the past six months, Sterling’s stock has outperformed both Granite and the broader construction sector, as shown in the chart below.

Source: Zacks Investment Research

In terms of valuation, Sterling has consistently traded at a higher forward 12-month price-to-earnings (P/E) ratio compared to Granite over the past year.

Source: Zacks Investment Research

These technical indicators suggest that Sterling offers a stronger growth trajectory but at a premium valuation, while Granite provides slower growth with a more attractive valuation.

EPS Estimate Trends: STRL vs. GVA

Recent analyst estimates show that Sterling’s expected earnings per share (EPS) for 2026 have been revised upward to $12.25 from $11.95 over the past month, indicating anticipated earnings growth of 17.2% and projected revenue growth of 18.8%.

Sterling's EPS Trend

Source: Zacks Investment Research

In contrast, Granite’s 2026 EPS estimate has been adjusted downward to $6.35 from $6.38, reflecting expected earnings growth of 16.2% year over year.

Granite's EPS Trend

Source: Zacks Investment Research

Which Infrastructure Stock Is More Attractive?

Both Sterling and Granite are set to benefit from ongoing U.S. infrastructure investment, but their near-term prospects differ. Sterling’s growth is increasingly driven by mission-critical projects, especially in data centers and large industrial developments, supported by a growing backlog and accelerating revenue in its E-Infrastructure segment. Granite, on the other hand, has greater exposure to public transportation and civil works, with a record CAP and a rising share of best-value contracts that enhance visibility and margin stability.

From an earnings momentum perspective, Sterling stands out, with upward revisions to its 2026 EPS estimates and stronger projected revenue growth. Granite’s estimates have softened, indicating a more cautious outlook despite solid operational performance and portfolio improvements.

Currently, Sterling holds a Zacks Rank #2 (Buy), while Granite is rated Zacks Rank #4 (Sell), making Sterling the more compelling choice for investors seeking higher earnings momentum and exposure to faster-growing segments of the construction industry.

View the full list of Zacks #1 Rank (Strong Buy) stocks here.

Top Semiconductor Stock Highlight

A lesser-known company specializing in semiconductor products—distinct from industry giants like NVIDIA—is poised to capitalize on the next wave of market growth. As it gains more attention, it presents an appealing opportunity for investors.

With robust earnings growth and a rapidly expanding customer base, this company is well-positioned to meet soaring demand in Artificial Intelligence, Machine Learning, and the Internet of Things. The global semiconductor market is forecast to grow from $452 billion in 2021 to $971 billion by 2028.

Discover this stock for free >>

Additional Resources

For the latest stock recommendations from Zacks Investment Research, you can download the report on the 7 Best Stocks for the Next 30 Days. Get your free report here.

Sterling Infrastructure, Inc. (STRL): Free Stock Analysis Report

Granite Construction Incorporated (GVA): Free Stock Analysis Report

Original article published by Zacks Investment Research

Zacks Investment Research

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Walker & Dunlop (WD) Shares Are Down Today

Exclusive-QIA, Visa and ADIA set to anchor SoftBank's PayPay IPO, sources say

SIREN plunges after 1M token deposit: Will $0.30 support fall next?

Tricolor Noteholders File Lawsuit Against JPMorgan, Barclays, and Fifth Third