Cheniere Energy Reports Fourth Quarter Earnings Below Expectations, Year-Over-Year Revenue Increases

Cheniere Energy, Inc. Q4 2025 Earnings Overview

Cheniere Energy, Inc. (LNG) announced adjusted earnings of $2.87 per share for the fourth quarter of 2025, falling short of the Zacks Consensus Estimate of $3.83. This result also represents a decline from the $4.33 per share reported in the same period last year. The decrease was mainly attributed to reduced total margins per MMBtu of LNG delivered, along with increased income tax provisions and higher net income allocated to non-controlling interests.

The company’s revenue reached $5.5 billion, surpassing analyst expectations of $5.2 billion and marking a 23% increase from the $4.4 billion reported a year earlier. This growth was largely driven by a 24.5% rise in LNG sales.

Dividend and Financial Highlights

For the fourth quarter of 2025, Cheniere’s board maintained a quarterly cash dividend of $0.55 per share, payable to shareholders of record as of February 6, 2026.

Adjusted EBITDA for the quarter was $2 billion, up approximately 30% year-over-year, primarily due to higher LNG delivery volumes. Distributable cash flow (DCF) for the period totaled $1.5 billion.

Project Updates and Strategic Initiatives

In December 2025, Train 4 of the Corpus Christi Liquefaction (CCL) Stage 3 Project achieved substantial completion, following the earlier completion of Trains 1 through 3. That same month, Cheniere’s subsidiaries submitted applications to the Federal Energy Regulatory Commission (FERC) to boost LNG capacity at both the Stage 3 project and the CCL Midscale Trains 8 & 9 Project by roughly 5 million tonnes per annum (mtpa).

In February 2026, the company also requested FERC approval for the CCL Expansion Project. Additionally, Cheniere Marketing International LLP entered into a long-term sales and purchase agreement with CPC Corporation, Taiwan, for up to 1.2 mtpa of LNG deliveries from 2026 to 2050. Production from Train 5 of the Stage 3 project began in February 2026.

During the same month, Cheniere’s board authorized a major increase to the company’s share repurchase program, raising the total authorization to over $10 billion for 2026-2030, which includes a $9 billion addition to the $1.2 billion remaining under the previous authorization as of December 31, 2025.

Capital Allocation and Shareholder Returns

The company completed its “20/20 Vision” capital allocation plan ahead of schedule, investing over $20 billion since 2022 and delivering more than $20 per common share in run-rate DCF. In the fourth quarter and full year 2025, Cheniere allocated about $1.7 billion and $6.1 billion, respectively, toward growth initiatives, debt reduction, and shareholder returns. The company repurchased approximately 4.8 million shares in the fourth quarter and 12.1 million shares over the year, spending roughly $1 billion and $2.7 billion, respectively. Additionally, Cheniere repaid $300 million in long-term debt during the fourth quarter of 2025.

Cost Structure and Balance Sheet

Total costs and expenses for the fourth quarter were $1.6 billion, representing a 39% decrease from the prior year’s quarter. As of December 31, 2025, Cheniere held $1.1 billion in cash and cash equivalents. Net long-term debt stood at $22.5 billion, resulting in a debt-to-capitalization ratio of 63.5%.

2026 Outlook

For the full year 2026, Cheniere projects consolidated adjusted EBITDA between $6.7 billion and $7.2 billion. The company expects distributable cash flow to range from $4.35 billion to $4.85 billion, reflecting anticipated LNG production and the expected completion of the remaining three trains at Corpus Christi Stage 3. Substantial completion of Trains 5 through 7 is also anticipated in 2026.

Cheniere Energy currently holds a Zacks Rank #3 (Hold).

Other Notable Earnings Reports

- TechnipFMC plc (FTI): Reported adjusted earnings of $0.70 per share for Q4 2025, exceeding the consensus estimate of $0.51 and up from $0.54 a year ago. The strong performance was driven by robust results in both the Subsea and Surface Technologies divisions. Revenue was $2.5 billion, slightly below expectations but higher than the $2.4 billion reported last year. As of December 31, 2025, FTI had $1 billion in cash and $395.7 million in long-term debt, with a debt-to-capitalization ratio of 10.5%.

- ProPetro Holding Corp. (PUMP): Achieved adjusted earnings of $0.01 per share in Q4 2025, outperforming the expected loss of $0.13 per share and improving from a $0.01 loss a year earlier. This was supported by a 16.3% year-over-year reduction in costs and expenses. Revenue reached $290 million, beating the consensus estimate of $280 million, with strong contributions from the Wireline and Hydraulic Fracturing segments. However, total revenue declined 9.6% from the prior year’s $321 million due to lower service revenues in Hydraulic Fracturing and Cementing. As of year-end, PUMP had $91.3 million in cash and $45 million in borrowings under its ABL Credit Facility.

- Ovintiv Inc. (OVV): Posted adjusted earnings of $1.39 per share for Q4 2025, surpassing the consensus estimate of $0.98 and up from $1.35 a year ago. The increase was driven by higher production volumes and improved realized prices for plant condensate, natural gas liquids, and natural gas. Total revenue was $2.1 billion, down 1.9% year-over-year due to lower oil production and prices, but exceeded expectations by 10.2%. As of December 31, OVV had $35 million in cash and $4.4 billion in long-term debt, with a debt-to-capitalization ratio of 28.2%.

Analyst Insights and Top Stock Picks

Zacks’ research team has identified five stocks with the potential to double in value in the coming months. Among these, the Director of Research, Sheraz Mian, highlights a lesser-known satellite communications company poised for significant growth as the space industry expands. Analysts anticipate a major revenue surge in 2025. While not all picks achieve outsized returns, this selection could outperform previous high flyers such as Hims & Hers Health, which gained over 200%.

Further Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

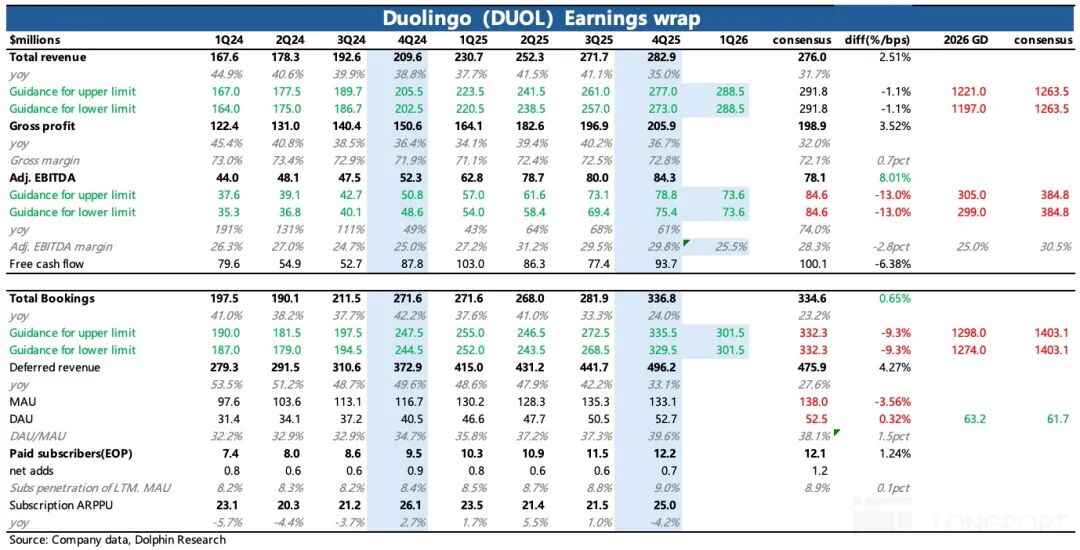

Duolingo: Guidance Crashes Again, Has Green Bird Really Become a "Dead Duo"?

SpaceX's $50B Public Offering: An In-Depth Look at Starlink's Driving Force

Hayward's Fourth Quarter Results: An Easy-to-Understand Overview of the Company Beyond the Figures

Market Strategist Says XRP Target Just Changed. Here’s Why