Opendoor or Zillow: Which Real Estate Tech Stock Has Greater Growth Potential Today?

U.S. Housing Market Challenges and Digital Real Estate Strategies

The American housing market continues to face obstacles due to high mortgage rates and a shortage of available homes, presenting a complicated landscape for online real estate companies. In this climate, Opendoor Technologies Inc. and Zillow Group, Inc. are taking different paths to capture market share and drive long-term growth. Opendoor is refining its data-centric, asset-light home-flipping approach with its “Opendoor 2.0” initiative, while Zillow is investing in its all-in-one housing platform, which combines property search, financing, and home tours. Investors are weighing which of these strategies may offer the best risk-adjusted returns. Let’s take a closer look at both companies.

Why Consider Opendoor?

Opendoor is gaining traction with its “Opendoor 2.0” transformation, focusing on increasing the number of homes it acquires, improving profitability per transaction, and speeding up the resale process. In the fourth quarter of 2025, Opendoor boosted its home purchases by 46% from the previous quarter, acquiring 1,706 homes—a significant shift from its earlier high-margin strategy. The company reported that its October 2025 acquisitions are on track to be the most profitable for that month in its history, with over half of those homes already sold or under contract and a much faster sales pace than in previous years.

Innovation is central to Opendoor’s progress. The expansion of its Cash Plus program provides sellers with more options and reduces the company’s financial exposure. Opendoor Checkout, now available in 40 states, streamlines the buying process with mortgage preapprovals, buyer protections, and digital closing tools. The company’s reach now covers nearly all homeowners in the contiguous United States. Additionally, Opendoor is leveraging artificial intelligence for underwriting, pricing, and operations, which is enhancing conversion rates, pricing accuracy, and resale speed while lowering costs.

Opendoor has also demonstrated improved cost management, with fixed operating expenses and infrastructure costs declining both quarter-over-quarter and year-over-year. The proportion of homes remaining on the market for more than 120 days has also dropped. Leadership remains committed to achieving adjusted net income profitability over the next 12 months by the end of 2026.

Despite these improvements, Opendoor’s short-term financial results still reflect its transition, as it works through older inventory. Fourth-quarter revenues fell due to lower starting inventory and faster sales of legacy homes, which also pressured contribution margins and kept adjusted EBITDA negative. The company anticipates further revenue declines in the first quarter as it rebuilds inventory under its updated model.

Why Consider Zillow?

Zillow is focused on expanding its integrated “housing super app,” aiming to capture more of the residential transaction process—from buying and selling to renting and financing. The company is strengthening connections between consumers and real estate professionals, while adding new services to enhance its ecosystem and increase transaction volume.

In the fourth quarter of 2025, Zillow’s Residential segment continued to grow, supported by better performance from Premier Agent and improved digital shopping tools. New features, such as AI-powered search, enhanced touring experiences, and improved partner integrations, are designed to boost user engagement and conversion rates. Zillow’s Rentals division is also growing, thanks to more multifamily partnerships and a larger inventory of listings.

The company is advancing its transaction capabilities, with growth in Zillow Home Loans and better integration between financing, touring, and agent services. These efforts are intended to increase the number of transactions that stay within Zillow’s platform. Management is focused on ongoing product improvements and operational efficiency to benefit both partners and consumers.

However, Zillow still faces a challenging market, with affordability issues and fluctuating mortgage rates limiting transaction volumes. While its marketplace model is capital-efficient, the company’s near-term revenue growth is constrained by the broader market’s slow recovery, making performance heavily dependent on improved housing activity.

Comparing Zacks Consensus Estimates for Opendoor and Zillow

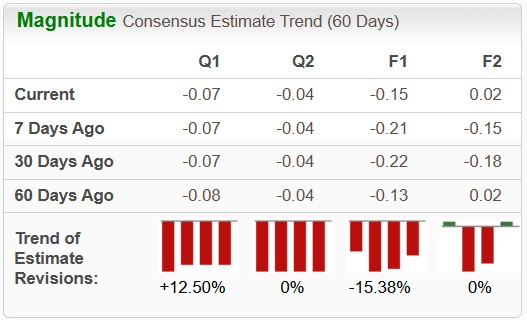

According to Zacks, Opendoor’s projected sales for 2026 are expected to decrease by 1.5% year-over-year, but earnings per share are forecasted to rise by 42.3%. Over the past two months, Opendoor’s 2026 earnings estimates have dropped by 15.4%.

Opendoor Earnings Estimate Trend

Image Source: Zacks Investment Research

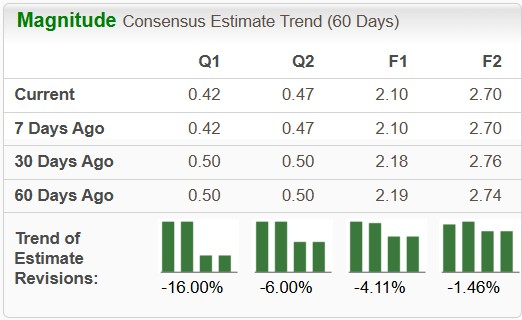

For Zillow, Zacks projects a 15.1% increase in sales and a 28.1% rise in earnings per share for 2026. However, Zillow’s 2026 earnings estimates have declined by 4.1% in the last 60 days.

Zillow Earnings Estimate Trend

Image Source: Zacks Investment Research

Stock Performance and Valuation: Opendoor vs. Zillow

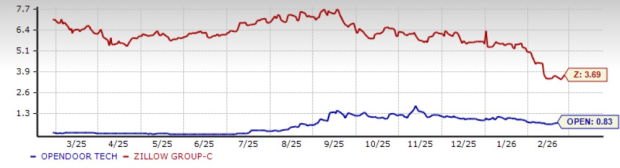

In the past year, Opendoor’s share price has soared by 278.3%, significantly outperforming both the broader technology sector and the S&P 500. In contrast, Zillow’s stock has declined by 38.9%, underperforming its peers and the overall market.

One-Year Price Performance: Opendoor and Zillow

Image Source: Zacks Investment Research

Opendoor is currently valued at a forward 12-month price-to-sales (P/S) ratio of 0.83, which is well below the industry average of 3.87. Zillow’s forward P/S ratio stands at 3.69 for the same period.

Forward 12-Month P/S Ratios: Opendoor and Zillow

Image Source: Zacks Investment Research

Summary and Outlook

Opendoor stands out as the more aggressive growth opportunity, thanks to its expanding acquisition efforts, broader product offerings, and focus on improving profit margins under the “Opendoor 2.0” strategy. The company’s disciplined approach to underwriting and faster home resales could enhance operating leverage as the housing market stabilizes.

Zillow, on the other hand, benefits from its capital-light business model, diverse revenue streams, and integrated platform. However, its higher valuation and dependence on a market rebound may limit short-term upside compared to competitors.

Given the current valuation gap and Opendoor’s greater sensitivity to market improvements, Opendoor may be better positioned to deliver strong returns if the housing market recovers.

Both Opendoor and Zillow currently hold a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Duolingo: Guidance Crashes Again, Has Green Bird Really Become a "Dead Duo"?

SpaceX's $50B Public Offering: An In-Depth Look at Starlink's Driving Force

Hayward's Fourth Quarter Results: An Easy-to-Understand Overview of the Company Beyond the Figures

Market Strategist Says XRP Target Just Changed. Here’s Why