PEN shares climb after surpassing Q4 earnings and revenue expectations, with improved profit margins

Penumbra, Inc. Reports Strong Q4 2025 Results

Penumbra, Inc. (PEN) announced its financial results for the fourth quarter of 2025, posting adjusted earnings per share of $1.18, up from $0.85 in the same period last year. This result exceeded analyst expectations by 5.36%.

On a GAAP basis, earnings per share reached $1.20, compared to $0.86 in the previous year. For the entire year, adjusted EPS climbed to $3.84, marking an 82.9% increase year-over-year.

Revenue Highlights

During the quarter, Penumbra generated $385.4 million in revenue, reflecting a 22.1% year-over-year increase on a reported basis and 20.9% growth at constant exchange rates. This figure surpassed consensus estimates by 6.74%.

Annual revenues totaled $1.40 billion, representing a 17.5% rise from the prior year (16.9% at constant exchange rates).

Following the February 25 announcement, PEN shares rose 1.7%, closing at $344.39 on Friday.

Segment Performance

Penumbra divides its operations into two geographic segments: United States and International.

- United States: Revenue reached $299.1 million, accounting for 77.6% of total sales, up 20.6% year-over-year.

- International: Sales grew 27.7% (20.9% at constant exchange rates) to $86.3 million, making up 22.4% of total revenue.

Product Category Breakdown

Penumbra reports sales in two main product categories:

- Thrombectomy: $254.7 million in revenue, up 15.7% year-over-year (14.7% at constant exchange rates).

- Embolization and Access: $130.7 million in sales, a 22.1% increase (20.9% at constant exchange rates).

Profitability and Margins

Gross profit for the quarter rose 24.4% to $262.1 million. The gross margin improved by 123 basis points to 68%, despite a 17.6% increase in cost of revenue.

Operating expenses for selling, general, and administrative functions increased 22.4% to $181.1 million. Research and development costs were $21.8 million, up 8.9%. Adjusted operating profit reached $59.2 million, compared to $42.8 million a year earlier, with the adjusted operating margin expanding by 181 basis points to 13.4%.

Financial Position

At the end of Q4 2025, Penumbra held $544.8 million in cash and marketable investments, up from $340.1 million at the close of 2024.

Acquisition and Guidance Update

In January 2026, Penumbra entered into a definitive agreement to be acquired by Boston Scientific in a cash and stock deal valued at $374 per share, or roughly $14.5 billion in enterprise value. The transaction is expected to close in 2026, pending shareholder approval and customary conditions. As a result, Penumbra has suspended its financial guidance for 2026.

Analyst Perspective

Penumbra finished Q4 2025 with earnings and revenue above expectations. Growth in both thrombectomy and embolization/access products was largely driven by strong U.S. performance, and margin expansion was notable.

During the quarter, Penumbra shared results from the STORM-PE randomized controlled trial. The study demonstrated that mechanical thrombectomy, particularly computer-assisted vacuum thrombectomy combined with anticoagulation, provided greater reduction in right heart strain than anticoagulation alone for patients with acute intermediate-high risk pulmonary embolism. Additional benefits included improved thrombus reduction, heart rate, oxygen needs, and functional outcomes.

Zacks Rank and Notable Medical Stocks

Penumbra currently holds a Zacks Rank #4 (Sell).

Other medical sector stocks with stronger rankings include:

- Intuitive Surgical (ISRG): Zacks Rank #1 (Strong Buy). Q4 2025 adjusted EPS was $2.53, beating estimates by 12.4%. Revenue of $2.87 billion exceeded forecasts by 4.7%. Long-term earnings growth is projected at 15.7%, above the industry average of 12.7%. The company has surpassed earnings estimates in the last four quarters, with an average surprise of 13.24%.

- Cardinal Health (CAH): Zacks Rank #2 (Buy). Q2 fiscal 2026 adjusted EPS was $2.63, topping estimates by 10%. Revenue reached $65.6 billion, up 0.9% over consensus. Long-term earnings growth is expected at 15%, compared to the industry’s 9.6%. Cardinal Health has beaten earnings estimates in the last four quarters, with an average surprise of 9.3%.

- Align Technology (ALGN): Zacks Rank #2 (Buy). Q4 2025 adjusted EPS was $3.29, exceeding estimates by 10.1%. Revenue of $1.05 billion outperformed forecasts by 5.3%. Long-term earnings growth is estimated at 10.1%, above the industry average of 9.5%. The company has beaten earnings estimates in three of the last four quarters, with an average surprise of 6.16%.

Stocks Poised for Significant Growth

Zacks analysts have selected five stocks expected to potentially double in value in the coming months:

- Stock #1: A disruptive company with impressive growth and resilience

- Stock #2: Positive momentum suggesting a buying opportunity

- Stock #3: Among the most attractive investments currently available

- Stock #4: Leading a rapidly expanding industry

- Stock #5: A modern omni-channel platform ready for expansion

Many of these picks are not widely followed by Wall Street, offering early investors a unique opportunity. Previous recommendations have achieved gains of +171%, +209%, and +232%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Daily Mirror-owner faces largest loss in ten years as Google traffic declines

Target’s newly appointed CEO reveals his strategy for revitalizing the company

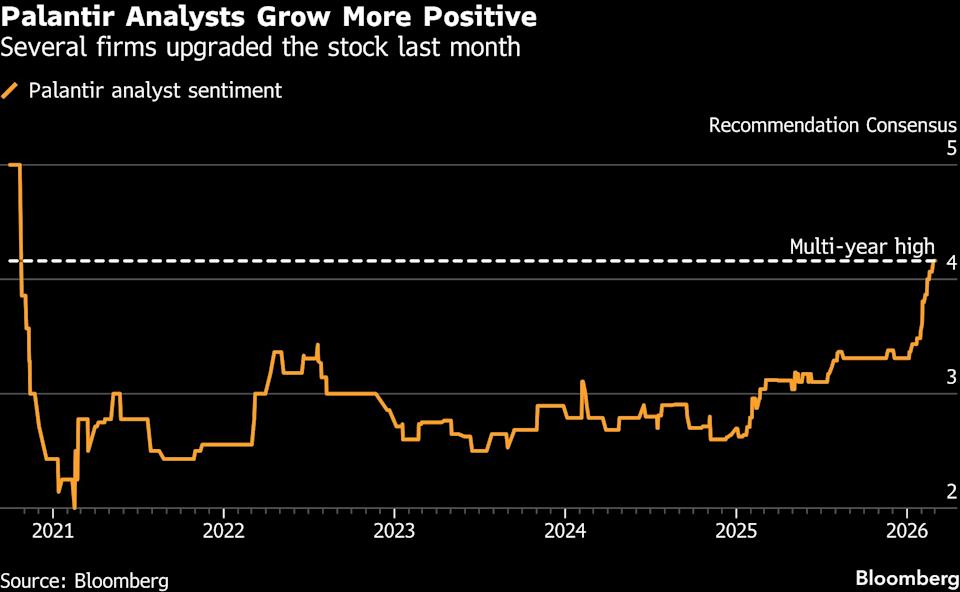

Palantir Returns to Wall Street’s Recommended Stocks Following a 38% Drop

Options Income Daily: MU, SOFI, CRWV and More