Delek US Stock: Not Recommended for Purchase, Yet Still Reasonable to Hold at Present

DK Outperforms Industry Peers Over Six Months

In the last half-year, Delek US Holdings, Inc. (DK) has delivered stronger returns than both the Oil Refining & Marketing sub-industry and the broader Oils & Energy sector. DK’s share price climbed by 28.4%, outpacing the sub-industry’s 27.8% gain and the sector’s 27.5% increase.

Image Source: Zacks Investment Research

Recent Financial Highlights

Delek recently reported its fourth-quarter 2025 results, posting adjusted earnings per share of $0.44—far better than the expected $0.25 loss. This turnaround from a $2.54 loss in the prior year was fueled by improved performance in both Refining and Logistics, as well as a 12.2% reduction in overall costs. Revenue rose by 2.3% year-over-year to $2.4 billion, beating consensus estimates by 6.3%.

With the industry landscape shifting and DK’s robust quarterly results, the company remains a notable contender in the downstream sector. The key question for investors is whether to buy, hold, or wait for a better entry point.

Examining the factors behind Delek’s recent momentum can help determine if the stock has further room to grow or if patience is warranted.

What Sets DK Apart as an Investment

- Enhanced Enterprise Optimization Plan: DK has raised its annual cash flow improvement target to at least $200 million, up from the original $80–$120 million. This boost, achieved through cultural and operational changes, reflects greater efficiency and positions the company for sustainable profitability.

- Swift RIN Monetization Strengthens Finances: The company quickly monetized a significant portion of its 2023 and 2024 RINs, generating about $360 million in the fourth quarter alone—well ahead of schedule. These proceeds were used to reduce debt, lowering annual interest expenses and enhancing financial stability.

- Consistent Shareholder Returns: DK maintained its commitment to shareholders by distributing approximately $15 million in dividends and repurchasing $20 million in shares during the fourth quarter. Management has reiterated its intention to uphold dividends and pursue buybacks, reinforcing investor confidence.

- Healthy Balance Sheet: As of December 31, 2025, DK’s net debt (excluding Delek Logistics) stood at a manageable $273.8 million. This financial strength gives the company flexibility to pursue strategic initiatives and continue rewarding shareholders, even during market downturns.

Risks That Could Affect DK’s Outlook

- Exposure to Regulatory and Legal Uncertainty: A portion of DK’s recent gains is linked to Small Refinery Exemptions, which remain subject to ongoing litigation and regulatory decisions. This introduces unpredictability and exposes the company to risks beyond management’s control.

- Major Planned Maintenance at Big Spring Refinery: In the first quarter of 2026, DK will undertake a significant turnaround at its Big Spring facility, reducing throughput to 22,000–28,000 barrels per day. While necessary for long-term reliability, this will temporarily impact production and profitability.

- Sensitivity to Crack Spread Volatility: DK’s earnings are closely tied to refining crack spreads, which are inherently cyclical and can be affected by economic, supply, or geopolitical shifts. A downturn in spreads could quickly erode profitability, regardless of internal improvements.

- Complex Organizational Structure: The company’s majority ownership of a master limited partnership adds financial and operational complexity, making it harder for investors to assess true performance and potentially leading to a persistent valuation discount.

Conclusion: Is DK a Buy Right Now?

DK’s execution on its optimization strategy, rapid RIN monetization, disciplined capital returns, and solid balance sheet all point to meaningful operational progress and improved financial flexibility. The company has raised its cash flow targets, reduced debt, and consistently rewarded shareholders, setting the stage for more durable profitability.

However, ongoing regulatory uncertainty, planned refinery downtime, exposure to volatile crack spreads, and structural complexity present notable risks. Given these factors, investors may want to wait for a more attractive entry point rather than buying DK stock at this time.

Alternative Energy Sector Picks

For those interested in the energy sector, several stocks currently hold higher Zacks rankings:

- USA Compression Partners (USAC): With a valuation of $4.02 billion, this company provides essential natural gas compression services and operates one of North America’s largest compression equipment fleets, serving a broad range of oil and gas clients.

- Oceaneering International (OII): Valued at $3.57 billion, Oceaneering offers engineered solutions such as remotely operated vehicles and subsea services, primarily for offshore energy, as well as advanced technology for aerospace, defense, and entertainment.

- Nabors Industries (NBR): With a $1.13 billion market cap, Nabors is a global leader in drilling rigs and services, supporting both land and offshore operations in over 20 countries through innovative technology.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

How does MetLife's stock performance stack up against other insurance companies?

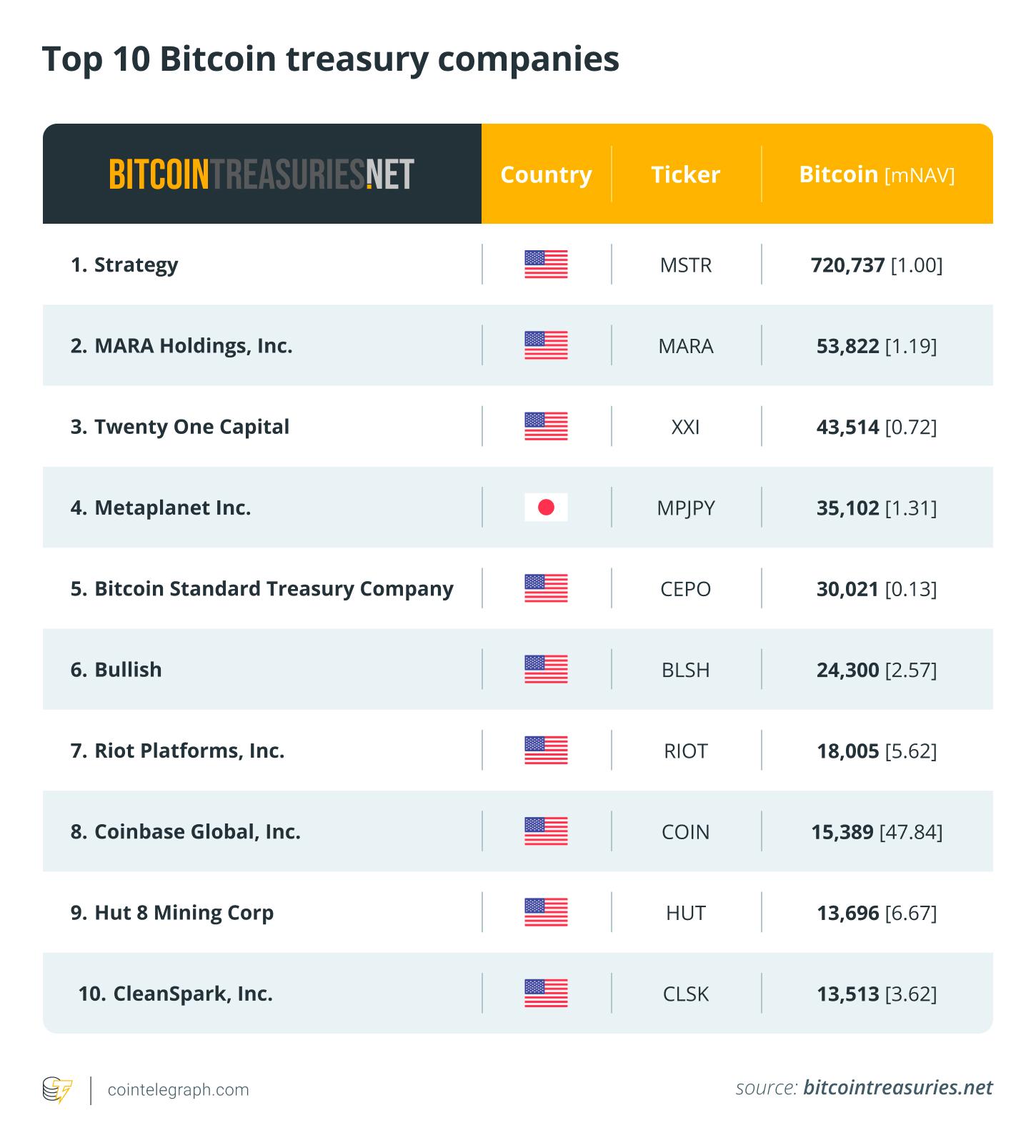

Why Peter Thiel’s Founders Fund walked away from an Ether treasury bet

Rising energy prices from the Iran war could help Russia pay for fighting in Ukraine

Target shares climb 7% following announcement of ambitious long-term growth plan