MKS Instruments Shares Drop 2.03% Following Varied Earnings and Changing Institutional Holdings, Placing 457th in Daily Trading Volume

Market Overview

On March 5, 2026, MKS Instruments (MKSI) ended the trading session down 2.03%, marking its weakest showing in several months. The stock saw $310 million in trading volume, placing it 457th in daily activity. This decline followed a mix of earnings results, guidance updates, and shifting institutional positions. While this drop contrasts with the 8.96% rally in October 2025 after robust third-quarter results, it reflects the ongoing volatility in the semiconductor and AI equipment industries.

Main Factors Impacting Performance

Earnings Fluctuations and Forward Guidance

The recent movement in MKS Instruments’ share price stems from mixed signals in its fourth-quarter 2025 results. The company posted earnings per share of $2.47 and revenue of $1.03 billion, narrowly surpassing revenue estimates but missing EPS projections by $0.04. Looking ahead, MKS provided first-quarter 2026 guidance of $1.72 to $2.28 EPS, which has left investors uncertain. The guidance suggests cautious optimism, with expectations for wafer fabrication equipment demand to pick up in the latter half of 2026, but acknowledges near-term challenges. Analysts have maintained a “Moderate Buy” recommendation with a $273.46 price target, though the stock’s high P/E ratio of 55.89 indicates skepticism about short-term performance.

Changes in Institutional Holdings

Recent shifts in institutional ownership highlight differing perspectives on MKS’s prospects. Roubaix Capital cut its stake by 37.2% in the third quarter, reducing its holdings to 33,588 shares valued at $4.16 million. In contrast, Vanguard Group and Cooke & Bieler LP increased their positions by 4% and 7.7%, respectively. These mixed moves reflect concerns about earnings volatility and the company’s significant debt load, with a debt-to-equity ratio of 1.53. Additionally, insiders sold 63,295 shares worth $16.14 million over the past three months, representing 0.51% of ownership, further contributing to investor caution.

Strategic Position in AI and Semiconductor Sectors

Despite recent earnings challenges, MKS remains focused on high-growth markets such as AI technologies and advanced packaging. CEO John Lee has highlighted the company’s strengths in flex laser drilling and proprietary chemistry for HDI boards, which are essential for next-generation semiconductor production. The third quarter of 2025 saw a 10% year-over-year increase in revenue, driven by AI-related demand. However, this growth has not consistently translated into earnings outperformance, as fourth-quarter results missed expectations. MKS’s $100 million voluntary debt repayment in October 2025 and $147 million in free cash flow (15% of revenue) demonstrate financial discipline, though margin pressures in a competitive landscape remain a concern.

Dividend Policy and Analyst Perspectives

The company recently raised its quarterly dividend to $0.25 per share (annualized $1.00), up 13.6% from the previous payout. While this increase reflects confidence in cash flow, the yield of 0.4% is still modest compared to industry peers. Analysts remain cautiously positive, with Bank of America and Cantor Fitzgerald lifting their price targets to $255 and $300, respectively, in early 2026. However, the consensus “Moderate Buy” rating signals a split view, as some, like Weiss Ratings, continue to recommend holding the stock. With a beta of 1.93, MKS is also more sensitive to market fluctuations, adding risk for those seeking stability.

Future Prospects and Industry Landscape

MKS’s outlook is closely linked to the cyclical trends of the semiconductor sector and the ongoing demand for AI infrastructure. The company has benefited from its involvement in advanced packaging and photonics, but faces margin pressure from fierce competition and supply chain issues. Management’s forecast for fourth-quarter 2025 revenue of $990 million (plus or minus $40 million) and its emphasis on wafer fab equipment growth in late 2026 point to long-term potential. However, the recent 2.03% share price drop highlights the market’s need for more consistent short-term results to support the company’s premium valuation.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

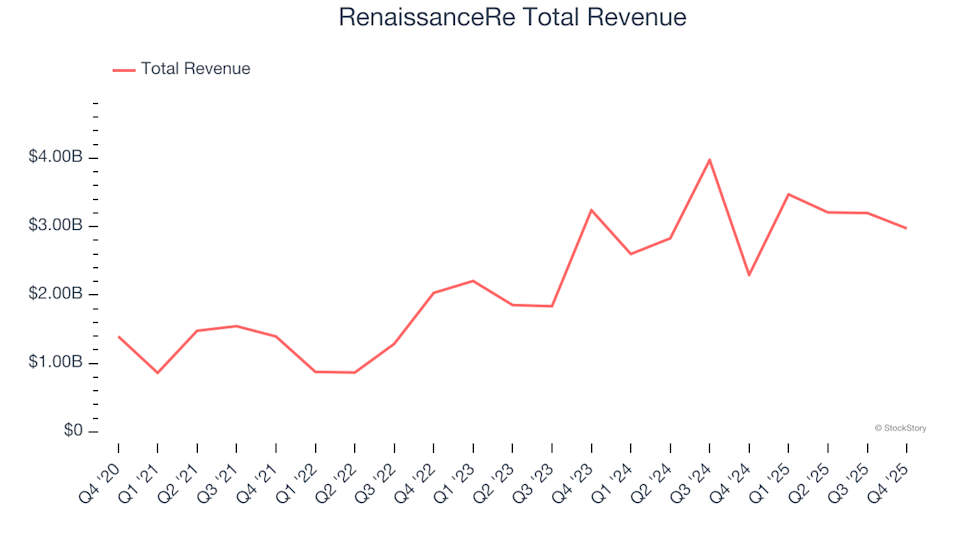

Reflecting on the Fourth Quarter Results of Reinsurance Stocks: RenaissanceRe (NYSE:RNR)

Orion Properties: A Tactical Play on a Strategic Pivot's Execution Risk

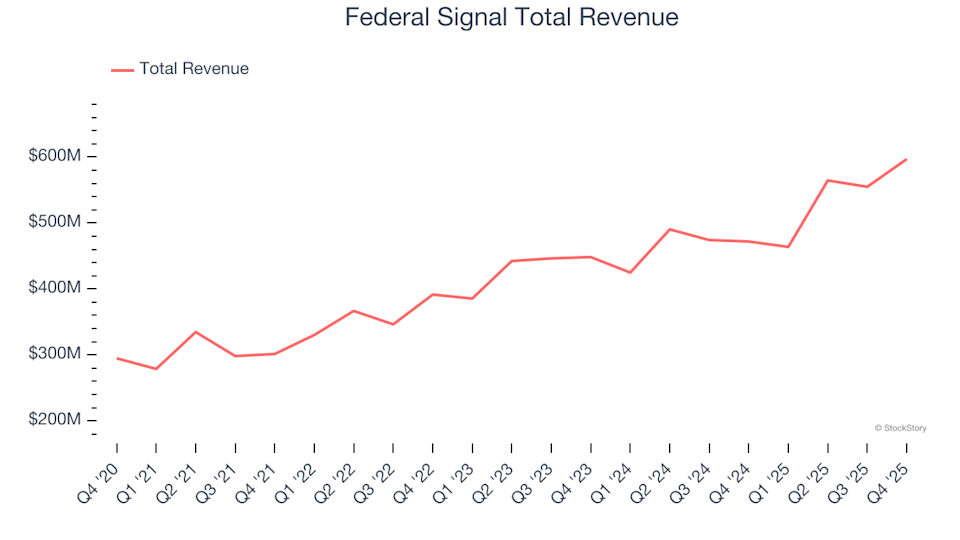

Heavy Transportation Equipment Stocks Q4 Analysis: Comparing Federal Signal (NYSE:FSS) With Its Competitors