M&T Bank Stock Slides Despite Record Earnings and 459th-Ranked Trading Volume Surge

Market Snapshot

M&T Bank Corporation (MTB) experienced a 1.48% decline in its stock price on March 5, 2026, despite a significant surge in trading volume. The stock’s volume rose by 77.63% to $0.31 billion, ranking it 459th in daily trading activity. This performance contrasts with recent earnings and operational updates, including a 11% increase in its quarterly dividend and a $2.85 billion annual net income for 2025. The mixed signals between strong earnings and a modest price drop highlight investor uncertainty amid evolving market conditions.

Key Drivers

Earnings Outperformance vs. Price Decline

M&T Bank’s Q4 2025 results exceeded expectations, with earnings per share (EPS) of $4.72, surpassing forecasts by 5.59%. Revenue of $2.47 billion met projections, yet the stock fell 1.68% post-announcement. This disconnect suggests that while the bank outperformed on the top line, investors may have been cautious about broader macroeconomic risks, such as interest rate volatility or credit quality concerns. The decline also followed a 1.68% drop in Q4 net income from $792 million in Q3 2025, signaling potential short-term operational challenges.

Annual Performance and Dividend Strategy

For 2025, M&T achieved record net income of $2.85 billion and an EPS of $17.00, driven by robust net interest income and disciplined cost management. The bank also increased its quarterly dividend by 11% and repurchased 9% of outstanding shares, reflecting confidence in capital returns. However, these positives were partially offset by a 7% decline in Q4 net income compared to Q3, raising questions about the sustainability of its earnings momentum. The 11% dividend hike, while attractive to income-focused investors, may have been priced into the stock ahead of the announcement.

Net Interest Income and Loan Growth Outlook

M&T projected net interest income between $7.2–7.35 billion for 2026, supported by an expected 140–142 billion in average loans and 165–167 billion in deposits. This aligns with broader industry trends of banks expanding credit portfolios amid a stable interest rate environment. However, the bank’s net interest margin (NIM) has faced pressure in recent quarters, with Q4 2025 NIM declining slightly from 3.02% in Q3. Investors may be weighing the balance between loan growth and margin compression, particularly as competition intensifies in regional banking markets.

Earnings Presentation and Strategic Focus

The bank’s upcoming Q1 2026 earnings presentation on April 15 will be critical for investor sentiment. CFO Daryl Bible emphasized M&T’s commitment to operational efficiency and transparency, aiming to build a scalable enterprise. While these goals are positive, the lack of concrete guidance on cost-cutting measures or technological investments may leave some investors unconvinced. Additionally, the bank’s tangible book value per share increased by 7% in Q4, indicating asset quality resilience, but this metric alone may not be sufficient to drive long-term growth expectations.

Sector-Wide Dynamics and Investor Sentiment

Broader sector events, such as ex-dividend dates for peers like Bank of America and Wescanto, may have influenced M&T’s trading activity. The bank’s recent performance also occurred amid mixed results from regional banks, with some reporting earnings beats and others missing targets. M&T’s ability to maintain its earnings trajectory while navigating a potential slowdown in loan demand or rising credit costs will be pivotal. For now, the market appears to be pricing in caution, as reflected in the stock’s decline despite solid annual results.

Outlook and Strategic Challenges

Looking ahead, M&T’s 2026 guidance for net interest income and loan growth suggests confidence in its core business. However, the bank must address near-term headwinds, including a 13.7% decline in non-interest income and rising non-interest expenses in Q4 2025. Management’s focus on efficiency and scale will be critical in maintaining profitability. If M&T can execute its strategic priorities without sacrificing credit quality or operational margins, it may regain investor confidence. Until then, the stock’s performance will likely remain sensitive to macroeconomic signals and sector-specific developments.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

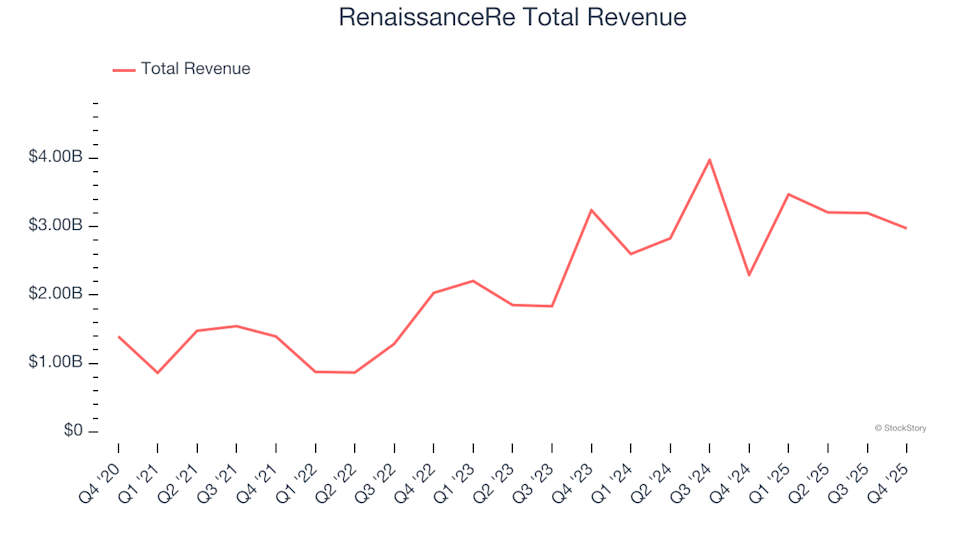

Reflecting on the Fourth Quarter Results of Reinsurance Stocks: RenaissanceRe (NYSE:RNR)

Orion Properties: A Tactical Play on a Strategic Pivot's Execution Risk

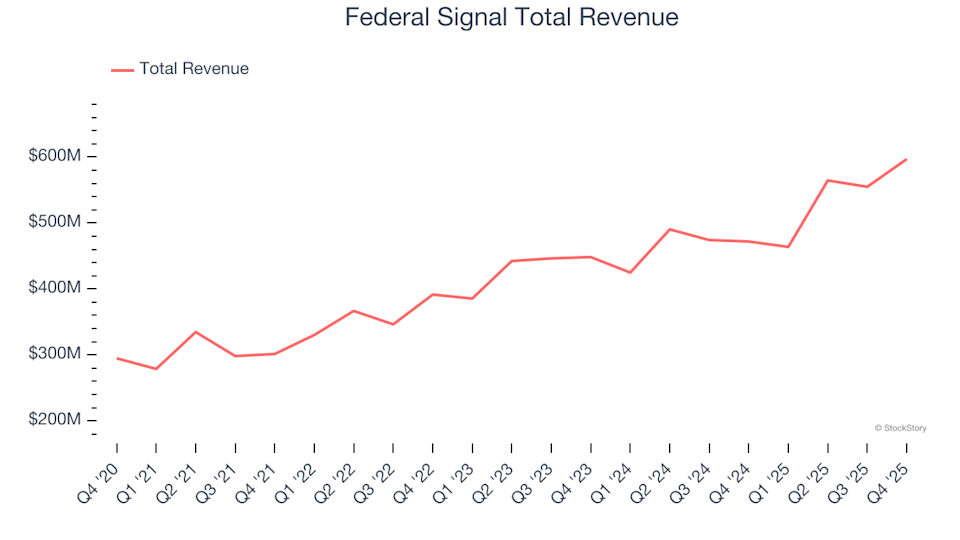

Heavy Transportation Equipment Stocks Q4 Analysis: Comparing Federal Signal (NYSE:FSS) With Its Competitors