I. Discussion on Analytical Frameworks and Methods

My approach to macroeconomic analysis is: based on an analytical framework, I directly form opinions and conclusions, then wait for economic indicators to verify those views. I do not obsess over short-term fluctuations in economic indicators (I don’t overcomplicate details); as long as the trend remains unchanged, I do not revisit the logic and framework. This approach saves a lot of energy and allows for continual testing and improvement of the analytical framework.

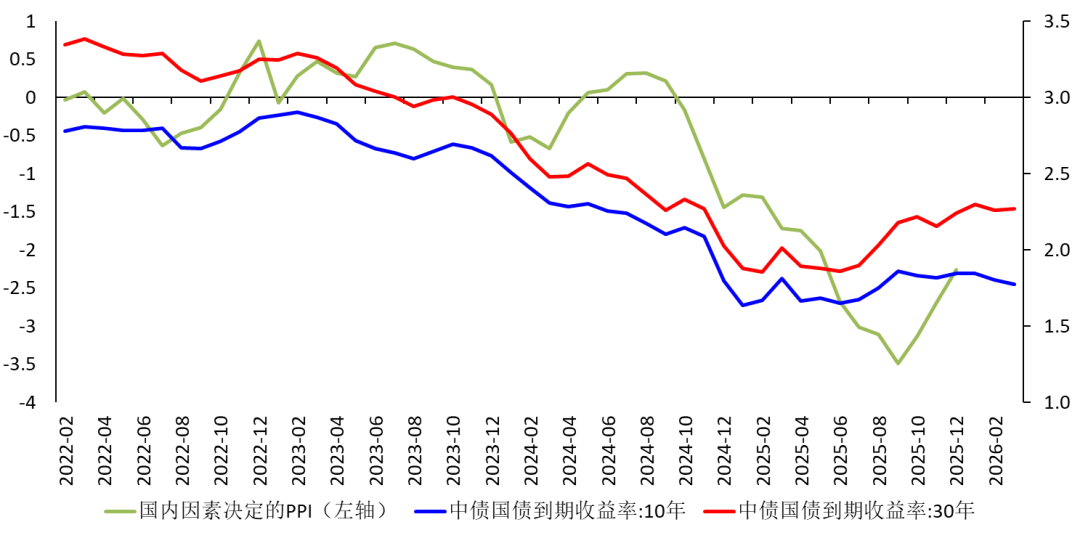

Since Q2 of 2023, I have believed that after 2022, the economy has fallen into a balance sheet recession, with aggregate demand trending downward in the long run. In January 2024, I broke down the PPI into international factors (CRB, shipping freight) and China-specific factors (aggregate demand), and found that the component of PPI determined by aggregate demand showed that since mid-2022, aggregate demand has been weak and the industrial sector has been in deflation. The PPI determined by aggregate demand is generally consistent with industrial capacity utilization, corporate bond yields, and stock index trends. And, as pointed out at the end of March 2024, "In the coming years, the PPI is likely to remain at a low level(unless some unexpected factors cause a global commodity price surge, as in 2020-2021)." The data from the past two years have already verified these perspectives, so I didn't update the analysis from January 2024. Now, here is an update. II. Data

The decomposition method for PPI can be found in the January 2024 analysis, which is not explained in detail here; the results are presented directly. The data used are as follows:

1. Dependent variable: Year-on-year PPI.

2. Explanatory variables:

[1] CRB Industrial Raw Materials Index YoY: CRBindu

[2] CRB Metals Index YoY: CRBmetal

[3] CRB Food Index YoY: CRBfood

[4] CRB Textiles Index YoY: CRBfz

[5] CRB Edible Oil Index YoY: CRBoil

[6] CRB Livestock Index YoY: CRBani

[7] Imported Shipping Freight Index: Container Ship YoY, CICFI

[8] Imported Shipping Freight Index: Dry Bulk Carrier YoY, CDFI

[9] Imported Shipping Freight Index: Oil Tanker YoY, CTFI [10] M1 YoY. [11] M2 YoY. [12] Total social financing YoY: sr [13] Credit balance YoY: credit [14] RMB Real Effective Exchange Rate Index YoY: Ex. [15] Industrial added value YoY: After seasonal adjustment to the industrial added value index to eliminate the Spring Festival effect, the seasonally adjusted YoY growth rate is used as the explanatory variable, denoted as IVA. Not all these explanatory variables appear in the equation; those with coefficients not significantly different from zero are eliminated. III. Fitting and Decomposition The sample period is from January 2019 to December 2025, a total of 84 months. The fitting shows that CRB Industrial Raw Materials Index YoY, CRB Metals Index YoY, CRB Edible Oil Index YoY, CRB Livestock Index YoY, CDFI YoY, M1, Social Financing, and Industrial Added Value YoY coefficients are significantly different from zero. The first five are considered international factors, and the last three are considered domestic factors, thus decomposing PPI into two parts, as shown in Figure 1:  Figure 1: Decomposition of PPI into Two Parts

Figure 1: Decomposition of PPI into Two Parts It can be seen that:

[1] The large fluctuations in China's year-on-year PPI are mainly determined by international factors. The root cause is overcapacity, with supply far exceeding domestic demand, so domestic demand has little impact on PPI.

[2] From 2020 to 2022, production halts of European and American enterprises, coupled with factors such as the Russia-Ukraine war, led to a global commodity price increase on one side, and an increase in demand for Chinese goods on the other, pushing up China's PPI. In Q4 2022, as production in Europe and the US recovered and demand for Chinese goods fell, international factors declined rapidly, turning PPI negative, and the industrial sector fell into deflation.

[3] Since mid-2023, domestic demand has remained weak, leading to a decline in PPI.

[4] Since 2025, although international factors have risen, domestic factors continue to drag down PPI. In the second half of 2025, although domestic factors have improved, the growth rate is still negative.

[5] The flattening and rebound of long-term treasury bond yields in 2025 are due both to central bank guidance and expectations of a price rebound.

Figure 2: PPI Component Determined by Domestic Factors

IV. Impact of the War After the U.S.-Israel-Iran war broke out on February 28, 2026, Iran closed the Strait of Hormuz, causing crude oil prices to soar. In the early morning of March 3, Trump indicated he might deploy ground forces; on March 3, Houthi forces attacked European and American merchant ships in the Red Sea, raising investor worries about the war's scale expanding and duration lengthening, keeping oil prices high and hurting the global economy. Thus, Asia-Pacific stock markets plunged on March 3.

I believe the U.S. will not deploy ground troops (click here). Whether from a military capability or fiscal standpoint, the U.S. is unable to wage a prolonged ground campaign in Iran. It was previously analyzed that rising crude oil prices will push up U.S. inflation and squeeze the Fed’s room to cut rates. For Japan, it will push up Japanese government bond yields, forcing the BOJ to hike rates earlier than expected and hitting the Japanese economy. For China, rising crude oil prices and shipping fees will obviously push up PPI. However, do not expect PPI increases to be smoothly transmitted to CPI and help the economy exit deflation. The reasons are:

[1] Weak downstream demand impedes transmission.

[2] During a balance sheet recession, if costs and prices for consumer goods (such as natural gas, gasoline) rise, households will cut consumption in other areas.

[3] If people remain pessimistic about the future, even if consumer prices rise across the board (which is unlikely) and force increased spending, as soon as the war ends, households will cut expenditures again, dragging down the growth rate of consumption even further.

Therefore, the component of PPI determined by domestic factors (aggregate demand) will remain very weak.

![Analyzing whether Decred’s [DCR] buyers will push price towards $36.7 liquidity](https://img.bgstatic.com/spider-data/97d640990b18dfb322bfae019209378c1772780625458.png)