Strattec Shares Surge 78% in the Last Year: Does it Remain a Good Investment Today?

Strattec Security: Still a Strong Opportunity After a 78% Surge

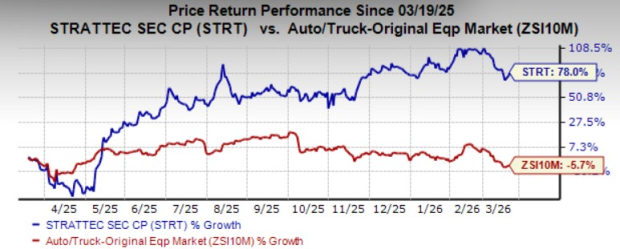

Strattec Security (STRT) has climbed nearly 78% over the past year, but its momentum appears far from over. The company’s robust fundamentals—including improving profit margins, enhanced cash flow, a more favorable product portfolio, and attractive valuation—continue to support a positive outlook. With a Zacks Rank #1 (Strong Buy), Strattec stands out as a top pick for investors seeking near-term growth. See the full list of Zacks #1 Rank stocks here.

Image Source: Zacks Investment Research

What’s Driving Strattec’s Continued Rally?

Strattec’s success is rooted in strong operational performance. In the second quarter of fiscal 2026, revenue increased 6% year-over-year to $137.5 million, adjusted earnings per share rose to $1.71 from $0.65, and gross margin improved by 330 basis points to 16.5%. Management now sees gross margins in the 15-16% range as a sustainable target, thanks to strategic pricing, product mix, and cost management.

The company’s earnings strength is further supported by restructuring efforts, supply chain improvements, and manufacturing enhancements. Annual savings from restructuring are projected at $3.4 million, while selling, administrative, and engineering expenses for the second half are expected to remain between 10% and 11% of sales.

Financial Flexibility Strengthens the Investment Case

Strattec’s financial position adds to its appeal. STRT generated $13.9 million in operating cash flow last quarter and $25.2 million in the first half of fiscal 2026. The company finished the quarter with $99 million in cash and just $2.5 million in debt. Management anticipates operating cash flow of approximately $40 million for the full year, with capital expenditures under $10 million.

This solid balance sheet enables Strattec to continue investing in automation, process upgrades, and new customer programs, even if automotive production remains inconsistent.

Quality of Growth Is Improving

Strattec is shifting its focus toward higher-value segments such as power access systems, door handles, and digital key solutions, while moving away from lower-margin businesses like switches. The company is also targeting new customer projects for model years 2029 and beyond, which could generate sustained revenue streams once contracts are secured.

This strategic shift in product mix positions Strattec for increased content per vehicle and stronger margins over time, even if industry production is sluggish.

Valuation Perspective

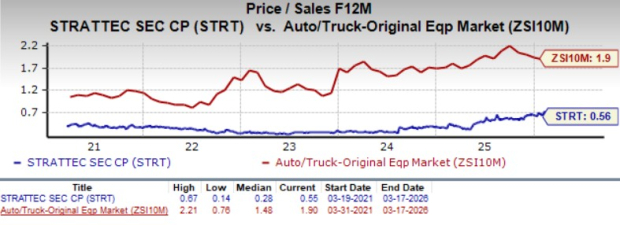

Strattec’s forward price-to-sales ratio stands at 0.56, which is below the industry average. By comparison, peers like Magna International (MGA) and BorgWarner (BWA) trade at forward P/S ratios of 0.37 and 0.75, respectively.

Image Source: Zacks Investment Research

Analyst Outlook

Despite some short-term challenges, Strattec’s long-term prospects remain favorable. Management expects sales in the second half of fiscal 2026 to decline 3-4% year-over-year, reflecting softer U.S. auto production, currency headwinds, and the impact of previous pricing actions. However, the company is better positioned than before to manage these obstacles, thanks to improved margins, tighter cost controls, and a strong cash balance.

The stock’s impressive rally does not diminish its upside potential. With rising profitability, robust cash flow, and a reasonable valuation, Strattec continues to offer an attractive investment opportunity.

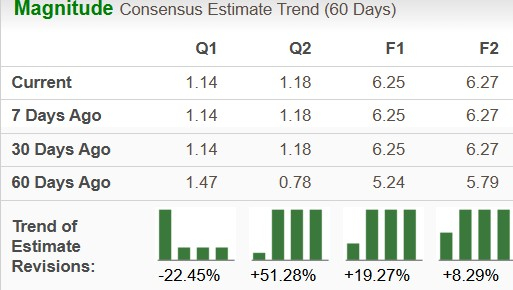

Consensus estimates from Zacks suggest that STRT’s fiscal 2026 earnings per share will grow by 16% year-over-year, with upward revisions over the past two months.

Image Source: Zacks Investment Research

Top Analyst Picks: One Stock Poised to Double

Among thousands of stocks, five Zacks experts have each selected their top candidate for a potential 100%+ gain in the coming months. From these, Director of Research Sheraz Mian has chosen one with the highest upside potential.

This company focuses on millennial and Gen Z consumers, generating nearly $1 billion in revenue last quarter. A recent dip in its share price presents a timely opportunity. While not every elite pick succeeds, this one could outperform previous Zacks selections like Nano-X Imaging, which soared 129.6% in just over nine months.

Discover Our Top Stock and Four Runners-Up for FreeFor the latest stock recommendations from Zacks Investment Research, you can download the 7 Best Stocks for the Next 30 Days. Get your free report here.

- BorgWarner Inc. (BWA): Free Stock Analysis Report

- Magna International Inc. (MGA): Free Stock Analysis Report

- Strattec Security Corporation (STRT): Free Stock Analysis Report

Originally published by Zacks Investment Research

Zacks Investment Research

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

How does increasing client assets and expanding advisory services benefit Schwab?

VNRX Surges 24% on ctDNA Breakthrough — But Broader Market Drags It Down

Are Options Traders Aware of Information About Cabot Stock That We Aren't?

ALDX Plummets 71% Following FDA's Third Complete Response Letter for Dry Eye Disease Drug Application