DANA Shares Rise 34% Year-to-Date: Is It Time to Buy, Hold, or Sell?

Overview of Dana Incorporated

Dana Incorporated (DAN) stands as a prominent global supplier of power transmission and energy management technologies for on-highway vehicles. Its diverse product lineup is designed to boost the efficiency, performance, and environmental sustainability of both passenger and commercial vehicles.

The company operates through two main divisions: Light Vehicle Drive Systems and Commercial Vehicle Drive and Motion Systems.

Stock Performance in 2024

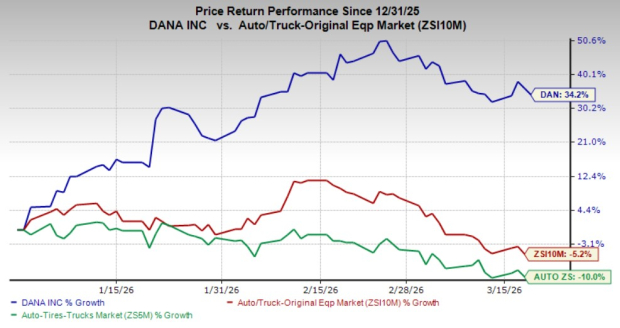

So far this year, Dana shares have significantly outpaced the broader market and sector averages. The stock has surged by 34.2% year-to-date, in stark contrast to a 5.2% drop in the industry and a 10% decline in the overall auto sector during the same period.

Year-to-Date Stock Analysis

Source: Zacks Investment Research

What Makes Dana an Attractive Investment?

- Margin Growth Through Cost Optimization: Dana has achieved $248 million in cost reductions and anticipates reaching a $325 million annualized savings rate by 2026, including the removal of $40 million in costs following its off-highway business sale. These efforts are expected to drive profitability improvements, with adjusted EBITDA projected to reach approximately $800 million in 2026—translating to a margin of 10-11% and a 250 basis point increase over 2025.

- Stable Revenue Backlog: Despite volatility in the electric vehicle sector, Dana has secured a multi-year backlog worth $750 million. Around $200 million of this is factored into its 2026 outlook, providing solid revenue visibility.

- Robust Financial Position and Shareholder Returns: Proceeds from the off-highway divestiture were used to reduce debt, resulting in a $1.9 billion decrease and liquidity of about $1.8 billion. This stronger balance sheet gives Dana the flexibility to pursue growth initiatives. The company has returned over $700 million to shareholders in 2025 and raised its quarterly dividend by 20% to $0.12 per share in February 2026. Dana has also expanded its share repurchase program to $2 billion through 2030, reflecting management’s confidence in its long-term strategy.

Potential Risks for Dana Investors

- Lower Volumes May Impact Revenue: Dana expects a $95 million revenue reduction in 2026 due to softer demand in traditional commercial vehicle markets. Ongoing weakness in electric and light vehicle platforms is also affecting its battery and electronics cooling segment.

- Increased Capital Expenditures: As Dana invests in new business launches and operational improvements, capital spending is set to rise to about $325 million in 2026—an increase of $70 million from the previous year. While these investments support future growth, they may temporarily constrain cash flow.

Outlook and Conclusion

Dana is well-positioned for continued advancement, thanks to disciplined execution, operational improvements, and effective cost management. Its strong backlog and enhanced financial flexibility support ongoing investments in growth and shareholder returns. These strengths are expected to drive steady operational gains and improved profitability over time.

Looking forward, upward revisions to EBITDA guidance and consistent shareholder payouts reinforce Dana’s positive investment case. With momentum in operations and a focus on reducing leverage, the company’s prospects remain favorable.

Currently holding a Zacks Rank #2 (Buy), Dana offers an appealing option for investors seeking exposure to a strengthening automotive supplier.

Other Noteworthy Automotive Stocks

- RENAULT (RNLSY): Zacks Rank #1 (Strong Buy). Consensus estimates for 2026 project sales growth of 14.4% and earnings growth of 176.3% year-over-year. EPS estimates for 2026 and 2027 have risen by $0.34 and $0.18, respectively, over the past month.

- Modine Manufacturing (MOD): Zacks Rank #1 (Strong Buy). Fiscal 2026 sales and earnings are expected to grow by 21.3% and 19%, respectively. EPS estimates for fiscal 2026 and 2027 have increased by $0.01 and $0.04 in the last 30 days.

- Blue Bird (BLBD): Zacks Rank #1 (Strong Buy). Fiscal 2026 earnings are projected to rise by 4.1% year-over-year, with EPS estimates up $0.16 in the past month and $0.26 in the past two months for fiscal 2027.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

MLSS Surges 13% After Hours — But No News Explains It

Strive's Bitcoin Accumulation Faces Liquidity Test as GAAP Losses Hit $393.6M