Berkshire Supports OXY's Net-Zero Oil Strategy While J.P. Morgan Predicts $60 per Barrel

Occidental Petroleum: Navigating a Bearish Oil Market

Assessing the prospects for Occidental Petroleum (OXY) requires understanding the current commodity cycle, which is unfavorable for oil prices. The industry faces persistent oversupply, weakening demand, and macroeconomic trends that support lower real interest rates and a softer dollar. These factors combine to limit price growth, making OXY’s focus on steady cash generation and leveraging transition-related premiums a crucial measure of its operational effectiveness.

Oil Price Outlook and Market Dynamics

Short-term projections indicate a notable downturn. According to J.P. Morgan Global Research, Brent crude is expected to average $60 per barrel in 2026, reflecting subdued supply and demand fundamentals. The bank highlights ongoing oil surpluses, which may necessitate production cuts to avoid excessive stockpiling. This bearish stance contrasts with the recent surge to $94 per barrel driven by geopolitical tensions in the Middle East—a spike analysts anticipate will revert to normal. The current volatility is seen as temporary, not indicative of a lasting trend. Forecasts suggest Brent will dip below $80 per barrel in Q3 2026 and average $64 per barrel in 2027, reinforcing the view that recent price jumps are short-lived disruptions within a broader downward trajectory.

Structural Shifts and OXY’s Value Proposition

The prevailing market conditions reflect deep-seated imbalances rather than a typical cycle. Global oil supply is projected to outpace demand growth, even as consumption rises. Meanwhile, the energy transition and shifting trade patterns—such as Russian oil moving away from India—are altering the market’s long-term balance. For Occidental Petroleum, success depends on navigating a cycle where average prices are significantly lower than previous highs. The company’s ability to generate robust cash flow, especially from its carbon capture and enhanced oil recovery (EOR) operations, is vital in this environment. Investors are adjusting to a new normal, and OXY’s strategy is under scrutiny.

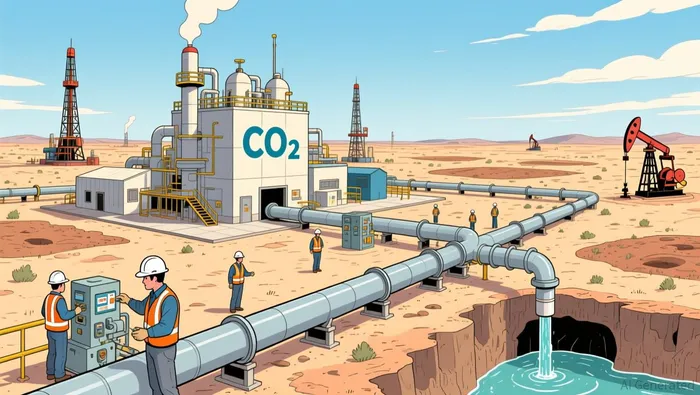

Building a Competitive Edge: EOR, Carbon Capture, and Net-Zero Oil

Occidental Petroleum is forging a distinctive advantage by combining decades of operational know-how with an ambitious carbon capture agenda. This approach aims to create a strong position in the evolving energy landscape, enabling its assets to produce cash flow and command a premium for lower-carbon output. At the heart of this strategy is OXY’s leadership in CO₂ Enhanced Oil Recovery (EOR) in the Permian Basin.

Legacy Infrastructure and Carbon Capture Initiatives

OXY’s EOR operations represent a vast, integrated network developed over half a century, utilizing 13 processing and recycling facilities and capable of storing up to 20 million metric tons of CO₂ annually. This isn’t a peripheral activity—it’s a core business that allows OXY to permanently sequester carbon while increasing oil recovery rates by 10–25% in targeted fields. This dual capability—boosting reserves and managing emissions—creates a synergy that sets OXY apart from most competitors.

This established infrastructure is now pivotal for the $1.3 billion Stratos Direct Air Capture (DAC) project. With 1,200 workers involved in construction, the facility is scheduled to begin operations this summer. Once operational, it will be the world’s largest DAC plant, capturing 500,000 metric tons of CO₂ from the atmosphere each year. The innovative pairing of this new technology with OXY’s existing EOR network allows the captured CO₂ to be transported directly to oil fields for injection and permanent storage.

Net-Zero Oil: Monetizing Carbon Solutions

OXY’s vision is to commercialize this integrated system as “net-zero oil.” By combining atmospheric carbon capture with reductions in operational emissions, the company aims to offset the CO₂ produced during the lifecycle of its products. This strategy, as OXY describes it, offers a vital bridge for the transition to a low-carbon economy, providing a solution for sectors where liquid fuels remain essential—even as global oil demand is forecasted to decline by up to 50% by 2050.

The company’s comprehensive CCUS (carbon capture, utilization, and storage) capabilities, combined with its Permian assets, form a unique business model. This enables OXY to secure long-term contracts with clients seeking lower-carbon feedstocks and fuels, and opens new revenue streams from carbon credits and premium pricing. In a challenging commodity market, this strategic moat is designed to safeguard cash flow and establish a new competitive advantage.

Financial Strength and Valuation Considerations

Occidental’s strategy has garnered strong investor support, as evidenced by a 58.85% year-to-date rally in its stock, which is trading near its 52-week high of $66. This performance reflects confidence in OXY’s ability to generate cash and deliver returns despite industry headwinds. The rally is backed by improved financials and a capital return policy that underscores management’s optimism about future cash flows.

Shareholder Commitment and Balance Sheet Health

A cornerstone of investor trust is OXY’s dedication to shareholders. The company maintains a dividend payout ratio of 56.7% TTM, supported by a 28-year streak of consecutive dividends. This sustainable approach, with recent increases, provides tangible returns while preserving capital for reinvestment in carbon capture and EOR projects. Strong cash flow has enabled OXY to meet its near-term debt reduction goals and shift focus toward rewarding shareholders.

Berkshire Hathaway’s ongoing accumulation further demonstrates confidence, with its stake approaching 29% of the company. This is a strategic, long-term investment, signaling belief in OXY’s operational strengths and its ability to sustain cash flow in a lower-price environment.

However, this optimism is reflected in the stock’s premium valuation, with a PE TTM of 39.3. The market is paying for OXY’s “net-zero oil” narrative and perceived financial resilience. In a structurally weak commodity cycle, this high valuation requires flawless execution—both operationally and strategically. Any missteps could quickly alter market expectations, as recent volatility has shown. For now, investors are willing to pay for the story, but continued performance is essential.

Upcoming Catalysts and Ongoing Risks

The investment outlook for Occidental Petroleum depends on several near-term catalysts and the management of persistent cyclical risks. The company’s distinctive value proposition—combining operational cash flow with an emerging carbon business—will be tested by specific developments in the coming quarters.

Stratos DAC Launch and Commercialization

The most immediate catalyst is the launch of the Stratos Direct Air Capture facility, which executives confirm is on track for summer 2025. Successfully bringing this plant online, with its capacity to capture 500,000 metric tons of CO₂ annually, will demonstrate OXY’s ability to execute major projects and prove the commercial viability of its carbon capture technology. Monetizing the captured carbon—through contracts with industrial emitters or carbon credit sales—will provide the first concrete financial validation of OXY’s “net-zero oil” strategy, transforming a promising narrative into a new revenue stream.

Oil Price Pressures and Cost Discipline

OXY must also contend with bearish oil price forecasts. J.P. Morgan Global Research expects Brent crude to average $60 per barrel in 2026, which would challenge cash flow from core operations. While OXY’s cost management and EOR efficiencies offer some protection, a rapid shift to lower prices could strain its ability to fund dividends and carbon investments. The current high valuation assumes success; any shortfall in operational cash flow would quickly test investor confidence.

Policy Environment and Incentives

The economics of OXY’s carbon capture business are closely linked to the pace of policy development around CCUS incentives. Company materials emphasize that effective CCUS implementation, supported by proactive policies, can deliver large-scale solutions. Incentives like the U.S. 45Q tax credit are vital for making DAC projects financially feasible. Any delays or reductions in policy support would raise costs and potentially erode the premium OXY aims to capture, while stronger policy backing could accelerate monetization of its carbon assets.

Execution in a Challenging Environment

Ultimately, the next year will be a test of OXY’s ability to deliver amid structural pressures. The Stratos plant must meet its operational goals, oil prices need to remain above bearish forecasts, and policy tailwinds must persist. Success across these areas is necessary to transform the “net-zero oil” model into a robust, diversified profit engine.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Blackstone stock climbs 3.27% amid positive technical indicators

Fannie Mae's Crypto-Backed Mortgages Indicate Regulatory Change Rather Than a Market Transformation

IMAX Experiences Earnings Surge Amid Leadership Gap Following CEO's Departure for Health Reasons

CAVA’s Market Value Hinges on Flawless Performance—Will It Meet Expectations Before the Premium Fades?