Strategy or Hut 8: Which Bitcoin Stock Offers Greater Growth Potential at Present?

Comparing MSTR and Hut 8: Two Distinct Paths to Bitcoin Exposure

Strategy (MSTR) and Hut 8 Corp. (HUT) stand out as leading stocks for investors seeking Bitcoin-related opportunities, though they approach the market in very different ways. MSTR focuses on acquiring large amounts of Bitcoin using capital raised from financial markets, while Hut 8 operates as a miner and digital infrastructure provider. Both companies’ fortunes are closely linked to Bitcoin’s price, with long-term strategies centered on accumulating and holding BTC.

As Bitcoin’s volatility rises and institutional interest grows, evaluating these two stocks becomes even more relevant. Which one presents the most promising potential? Let’s take a closer look.

Why Consider MSTR?

MSTR has evolved into a company with a primary focus on Bitcoin, leveraging traditional financial tools to amass a significant BTC treasury. The company’s main objective is to boost its Bitcoin Per Share by tapping into various capital sources.

As of March 30, 2026, MSTR is the largest corporate holder of Bitcoin, with approximately 762,099 BTC. This underscores its commitment to Bitcoin as a core asset. The company continues to grow its holdings, recently acquiring an additional 1,031 BTC, solidifying its leadership. MSTR’s approach is built on long-term accumulation, supported by fair value accounting and recognition from institutions, such as a solid credit rating and inclusion in the MSCI index.

Over time, MSTR has diversified its funding methods, raising about $25.3 billion in 2025 alone through equity, preferred stock, and innovative “digital credit” products. New offerings like STRC provide investors with yield-based exposure to Bitcoin, broadening participation and supporting further BTC purchases. The company’s recent $42 billion at-the-market program, split between common and preferred shares, offers flexibility for future capital needs.

MSTR’s balance sheet is heavily weighted toward digital assets, valued at $58.9 billion by the end of 2025. Despite carrying $8.2 billion in debt, the company maintains a healthy cash reserve of $2.25 billion, ensuring it can cover interest and dividends for several years. MSTR’s valuation is highly sensitive to Bitcoin’s price, making it a leveraged play on BTC.

What Sets Hut 8 Apart?

Hut 8 is transitioning from a pure Bitcoin mining company to a diversified digital infrastructure provider, integrating BTC holdings, AI computing, and energy assets. As of March 30, 2026, Hut 8 holds 13,696 BTC, ranking it ninth among corporate Bitcoin holders.

The company’s “power-first” approach leverages its energy resources to efficiently support both mining and AI-driven computing. Hut 8 has developed an 8.5 GW project pipeline as of December 31, 2025, and secured long-term contracts, including a 15-year, $7 billion AI data center lease with Fluidstack (backed by Google), ensuring stable cash flows. The compute segment is now the main growth engine, with revenues more than doubling in 2025.

Hut 8’s shift toward AI infrastructure is evident in its River Bend campus and Vega data center, which utilize advanced liquid cooling technology. Partnerships with companies like Anthropic and Fluidstack help the company transition from volatile mining income to steady, long-term infrastructure revenue. The spin-off of American Bitcoin allows Hut 8 to focus on scaling its core operations and invest further in AI expansion.

However, Hut 8 still faces earnings instability due to Bitcoin price swings and significant unrealized losses in 2025. The company also contends with execution risks related to large-scale AI projects, regulatory challenges, and high capital requirements.

MSTR vs. HUT: Analyst Estimates

According to Zacks, MSTR’s 2026 earnings are projected at $107.99 per share, a figure that has remained steady over the past month but has more than doubled in the last two months. This marks a dramatic improvement from the previous year’s loss of $15.23 per share.

MSTR Earnings Estimate Trend

Source: Zacks Investment Research

By contrast, Hut 8 is expected to remain unprofitable in 2026, with an estimated loss of $1.23 per share. This forecast has worsened by $0.20 over the past month and continues a downward trend. However, the company is projected to reduce its losses compared to the previous year’s $2.14 per share deficit.

HUT Earnings Estimate Trend

Source: Zacks Investment Research

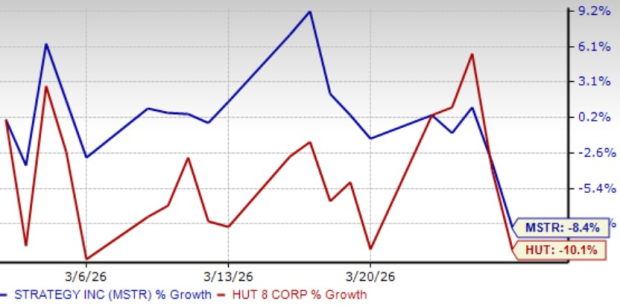

Stock Performance and Valuation: Head-to-Head

Over the past month, MSTR has outperformed HUT, with its shares dropping 8.4% compared to Hut 8’s 10.1% decline.

Hut 8’s weaker performance is largely attributed to its dependence on power infrastructure and regulatory uncertainties, with significant AI investments weighing on short-term results until they begin to generate returns.

MSTR’s relative strength comes from consistent Bitcoin accumulation, improved access to capital, and the introduction of new digital credit products for future fundraising. While both stocks have been affected by Bitcoin’s price drop, MSTR’s ongoing BTC purchases help sustain investor confidence.

MSTR vs. HUT: Stock Performance Comparison

Source: Zacks Investment Research

MSTR trades at a price-to-book ratio of 0.89x, much lower than Hut 8’s 3.09x, suggesting less valuation risk. Both stocks have a Value Score of F, but the difference reflects varying investor expectations. Hut 8’s higher valuation is driven by optimism about its AI infrastructure strategy, while MSTR’s valuation is more closely tied to its Bitcoin holdings, offering more direct exposure to BTC’s price movements.

MSTR vs. HUT: Valuation Comparison

Source: Zacks Investment Research

Final Thoughts: MSTR Takes the Lead

MSTR currently presents a more attractive opportunity, thanks to its aggressive Bitcoin acquisition strategy, improving earnings outlook, and disciplined approach to capital at a lower valuation. Hut 8, on the other hand, faces near-term challenges from its capital-intensive AI expansion and ongoing earnings volatility. For those seeking leveraged exposure to Bitcoin, MSTR stands out as the stronger choice at this time.

At present, MSTR holds a Zacks Rank #1 (Strong Buy), while HUT is rated Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Conduit Re's Chief Executive Offloads Stock Despite Robust Financial Position, Prompting Doubts About Confidence

Legal & General’s Bold Repurchase Plan Faces Unclear Business Prospects—Future Actions Depend on Buyback Speed