U.S.-Iran's Two-Week Truce Sends Oil Lower, but the Bigger Macro Story Still Runs Through War, Inflation, and the Fed

By:101 finance

Bitget offers one-stop trading for cryptocurrencies, stocks, and gold. Trade now!

A welcome pack worth 6200 USDT for new users! Sign up now!

The latest turn in the U.S.-Iran conflict looks, on the surface, like a geopolitical de-escalation. In market terms, though, it feels more like a sudden interruption to a macro panic. After President Donald Trump said he had agreed to suspend bombing of Iran for two weeks, with the arrangement tied to the reopening of the Strait of Hormuz, crude collapsed and risk sentiment improved almost immediately. Reuters reported that WTI fell about 16% to $94.85 a barrel and briefly touched $91.05, showing that the market was quick to strip out some of the most extreme supply-disruption pricing.

But what matters more is not the size of the oil drop itself. It is whether this reversal is large enough to change the macro story that had been building before the truce. At the height of the crisis, the market was not simply reacting to a war headline. It was reacting to the possibility that a prolonged disruption in the Strait of Hormuz could keep energy prices elevated, squeeze households, raise transportation and production costs, and force investors to rethink both inflation and policy expectations. The truce has pushed that tail risk back. It has not removed it. Reuters also noted that the broader market response was immediate, with S&P 500 futures rising more than 2% as oil plunged, underscoring how tightly this conflict had become linked to risk appetite and rate-sensitive assets.

That distinction matters because the transmission channel from this conflict into the U.S. economy runs straight through inflation. New York Fed President John Williams said this week that the Middle East war is likely to lift inflation this year through higher energy prices, with headline inflation seen around 2.75% in 2026 and potentially above 3% in the near term. He also said current policy, with rates at 3.5% to 3.75%, remains appropriate. That is a crucial signal. It suggests the Fed is not looking at this episode as a reason to rush into easier policy, even if growth starts to feel some strain.

This is where the ceasefire matters for more than just oil. If the worst-case Hormuz scenario had continued to escalate, the U.S. would have faced a nastier version of the same problem investors have been trying to avoid for months: slower growth paired with more stubborn inflation. Chicago Fed President Austan Goolsbee described the Iran war as a stagflationary shock that puts the Fed in a bind. In other words, the conflict does not just threaten higher gasoline and shipping costs. It raises the possibility that the central bank could be forced to keep policy tighter than markets would prefer even as economic momentum softens.

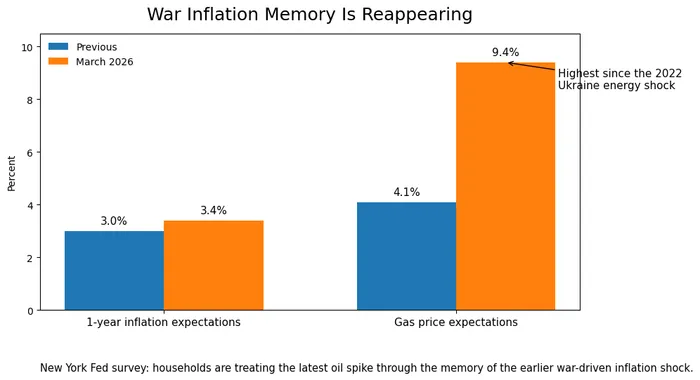

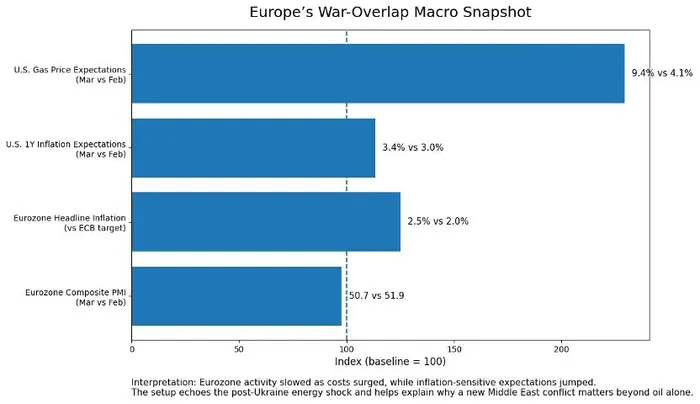

The reason this story now feels so powerful is that it is landing on top of an older geopolitical inflation scar rather than in a vacuum. The Russia-Ukraine war already taught markets how quickly an energy and commodity shock can spread far beyond the battlefield. Reuters reported this week that the New York Fed's March Survey of Consumer Expectations showed one-year inflation expectations rising to 3.4%, while expectations for gasoline prices jumped sharply to 9.4%, the highest level since the energy shock that followed Russia's 2022 invasion of Ukraine. That comparison matters because it shows households are not treating this oil spike as an isolated event. They are reacting through the memory of an earlier war-driven inflation surge that took much longer to fade than policymakers initially hoped.

Europe offers an even clearer reminder of how these two wars can overlap in macro terms. The euro zone had already spent years adjusting to the economic aftershocks of Russia's invasion of Ukraine, especially through energy markets and manufacturing costs. Now, with the Middle East conflict adding a fresh oil shock, Reuters reports that euro zone growth slowed to a nine-month low in March as surging costs linked to the war hit demand and activity. ECB policymaker Dimitar Radev has warned that inflation expectations may now rise faster than in the past precisely because consumers and businesses still carry the inflation scars left by the post-Ukraine energy shock. That is important for U.S. investors too, because it suggests the global economy is entering this latest conflict with far less psychological and pricing flexibility than it had before 2022.

That helps explain why the equity bounce should be read carefully. Stocks can rally on the idea that the most dangerous version of the energy shock has been delayed, and that reaction makes sense. But the move does not automatically restore the low-rate, low-inflation backdrop that high-valuation growth stocks tend to need. As oil rose during the conflict, investors began to reprice the path of rate cuts. Reuters reported that UBS pushed its forecast for Fed cuts back to September and December from June and September while also lowering its 2026 S&P 500 targets because of conflict-related energy risks. The truce may ease that pressure at the margin, but it does not yet restore the environment that existed before the war.

There is another layer here that markets may be underestimating. Russia is not simply a background character in this macro story. Reuters reported that Moscow sees new trade opportunities from the disruptions caused by the Middle East war, especially in oil, wheat, fertilizers, and other export-oriented sectors. That matters because the Russia-Ukraine war never stopped being a structural influence on food, fertilizer, and commodity trade. What the Iran conflict adds is another source of supply anxiety on top of that existing fragility. This is not just about one oil route or one ceasefire. It is about a global pricing system that has become more vulnerable to repeated wartime distortions.

Investors should also be careful not to mistake a tactical pause for a strategic resolution. Reuters separately reported that Iran set preconditions for lasting peace talks, including a halt to U.S. strikes, guarantees against future attacks, and compensation for damages. That is not the language of a finalized peace framework. It is the language of a negotiation that remains fragile. Oil can fall quickly when traders feel the immediate disaster has been delayed. It can also reprice quickly again if the ceasefire proves temporary or if passage through Hormuz does not normalize as expected.

There is also a reason the market cannot fully price this as an all-clear moment. The conflict is no longer only about bombs, ships, and missiles. Reuters has also reported a sharp escalation in Iran-linked cyber activity targeting U.S. critical infrastructure, including water and energy systems. That matters because cyber disruption is harder to quantify, harder to hedge, and more capable of reigniting inflation fears or risk aversion after a period of apparent calm.

So the real signal from this week's U.S.-Iran developments is not that danger has passed. It is that the most acute tail risk has stepped back just enough to let markets breathe. That should lower the odds of an immediate oil-driven policy scare, and it may buy equities some room for a short-term recovery. Yet the deeper macro tension remains intact, because the market is now trying to absorb a new Middle East energy shock while still living with the inflation memory and commodity fragility shaped by the Russia-Ukraine war. What investors need now is not another headline about de-escalation, but convincing evidence that oil will keep moving lower, that inflation expectations will stop drifting higher, and that central banks will no longer sound as though war itself has become one of the biggest obstacles to a cleaner path toward easing.

1

0

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

Understand the market, then trade.

Bitget offers one-stop trading for cryptocurrencies, stocks, and gold.

Trade now!

You may also like

PUFFER fluctuated by 53.0% in 24 hours: Exchange contract delisting triggers short squeeze and liquidity panic

Bitget Pulse•2026/04/08 08:21

Micron’s Exceptional Earnings Spark Huge Expectations as Analysts Aim for $600—Will the AI Surge Meet the Hype?

101 finance•2026/04/08 08:18

ORGO Surges Near 20-Day MA—But Is This a Rebound or a False Dawn?

101 finance•2026/04/08 08:18

Crypto's $100B Rebound: A Risk Appetite Trade, Not a New Trend

101 finance•2026/04/08 08:12

Trending news

MoreCrypto prices

MoreBitcoin

BTC

$71,702.62

+4.33%

Ethereum

ETH

$2,253.98

+6.92%

Tether USDt

USDT

$0.9999

+0.00%

XRP

XRP

$1.38

+5.16%

BNB

BNB

$612.74

+2.07%

USDC

USDC

$0.9999

+0.00%

Solana

SOL

$84.49

+5.50%

TRON

TRX

$0.3161

-0.02%

Dogecoin

DOGE

$0.09462

+4.23%

Hyperliquid

HYPE

$39.36

+8.42%

How to buy BTC

Bitget lists BTC – Buy or sell BTC quickly on Bitget!

Trade now

Become a trader now?A welcome pack worth 6200 USDT for new users!

Sign up now