How can a war change the US economy? Six charts reveal the full chain impact of oil prices, inflation, and interest rates

The Iran war is beginning to affect the U.S. economy in multiple ways, through both direct shocks and more subtle transmission channels. Rising energy prices have become the most obvious impact, while the potential blow to overall economic growth is still gradually unfolding.

Although concerns over a recession have increased since the conflict broke out, most economists believe the war's impact on U.S. GDP is relatively limited, expected to only drag growth by a small fraction of a percentage point.

However, a key variable is the duration of the war. If the current ceasefire agreement holds, inflationary pressure may gradually ease; but if the conflict escalates again, the outlook will deteriorate significantly, and could even threaten the already fragile economic growth seen over the past two quarters.

Mike Skordeles, Chief U.S. Economist at Truist Advisory Services, stated: "This conflict will erode a portion of growth, but the overall economy can withstand it. The bigger issue is uncertainty."

In fact, this uncertainty has shrouded the U.S. economy for the past year. Since the Trump administration launched the "Liberation Day Tariff" in April 2025 to the current tougher foreign policy, the market has remained in an environment of uncertainty, which the war has further intensified.

The core questions facing the market include: Is inflation during war a temporary phenomenon or a lasting trend? Will consumer spending be impacted? And how much will countries reliant on energy imports suffer?

On top of these issues, the policy response from the Federal Reserve and other central banks is a key variable.

Skordeles noted: "Iran is important, and oil prices are important, but other factors like income still support the economy. Another uncertainty is the Fed—this is delaying rate cuts, not canceling them. This means consumers will face higher borrowing costs."

Energy Shock: Dual Pressure from Oil Prices and Consumption

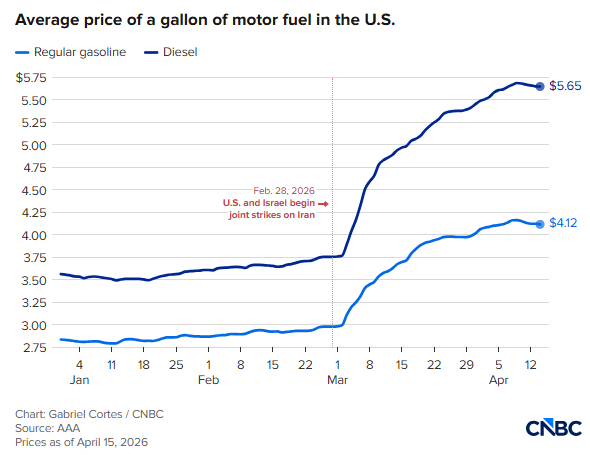

The rise in energy prices is directly affecting consumers. According to AAA data, the average U.S. gasoline price has risen to $4.10 per gallon. Meanwhile, rising mortgage rates are dragging down the real estate market, with existing home sales in March falling to a nine-month low.

Nevertheless, consumer spending still shows some resilience. Bank of America data indicates that debit and credit card spending in March rose 4.3% year-on-year, the largest gain in more than three years, with gasoline station spending soaring 16.5%. Even excluding energy, consumption still achieved a "healthy growth" of 3.6%.

Additionally, increased tax refunds have supported spending. The average refund this year is $3,521, up 11.1% from last year.

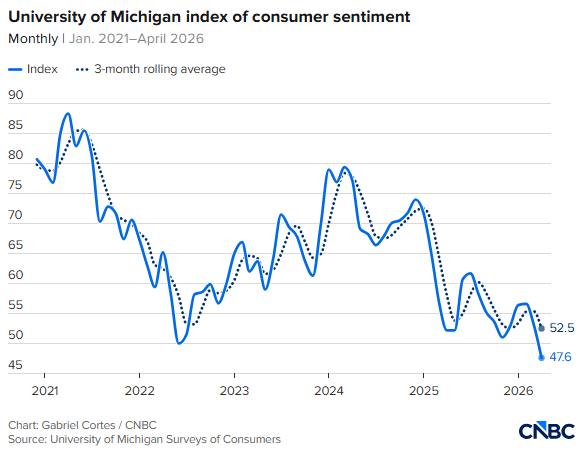

However, this actual consumption behavior diverges noticeably from consumer confidence. The University of Michigan survey finds U.S. consumer confidence has fallen to its lowest level since the 1950s—lower than during previous wars, stagflation periods, and financial crises.

Yet, analysts point out that the disconnect between consumer "words and actions" is not uncommon. David Kelly, Chief Strategist at JPMorgan Asset Management, said that although confidence is low, actual consumption is expected to continue growing, albeit at a slower pace.

Oil Prices as a Key Variable

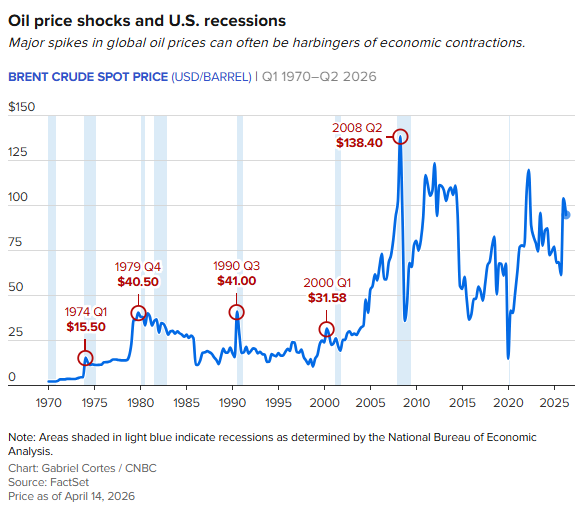

Economists generally agree that oil prices will be the core factor in determining the war's economic impact.

Joseph Brusuelas, Chief Economist at RSM, noted that only when WTI crude oil prices rise to $125 per barrel will there be a true economic shock, as demand destruction will be notably intensified.

Currently, WTI is around $91 a barrel, lower than the recent peak of $115, and still some distance away from the "danger zone".

He said: "We have not yet seen structural damage, and cannot yet judge the extent to which production and refining capacity in the Middle East has been affected."

Growth Slowdown and Changing Rate Cut Expectations

Economists generally expect that this war will slow growth, but not trigger a systemic collapse.

Goldman Sachs has lowered its GDP growth forecast for this year to 2%—down 0.5 percentage points from previous estimates. The Atlanta Fed expects Q1 growth of about 1.3%.

Meanwhile, Goldman Sachs expects the unemployment rate to rise to 4.6% and believes the economic slowdown will ultimately prompt the Fed to cut rates multiple times later this year.

Goldman Sachs economists said: "Rising oil prices, increased uncertainty about the outlook, and robust employment data are currently prompting the Fed to maintain a wait-and-see stance. We expect the combination of rising unemployment and only limited improvement in inflation will support rate cuts in September and December."

This forecast is more aggressive than current market pricing. The market currently expects rate cuts only as early as mid-2027, while the Fed previously only hinted at possibly one rate cut.

Inflation Remains the Biggest Obstacle

Inflation remains the key constraint on policy shifts.

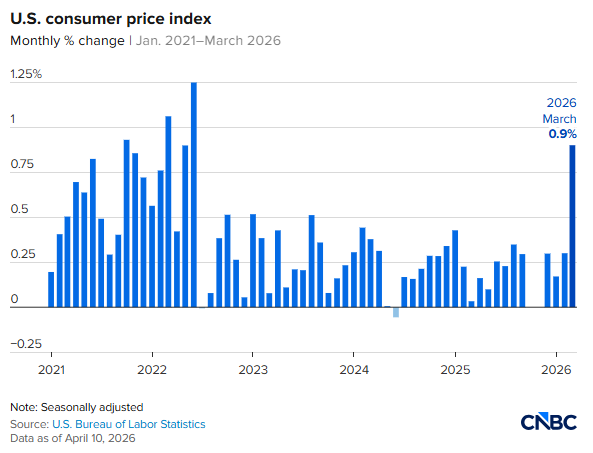

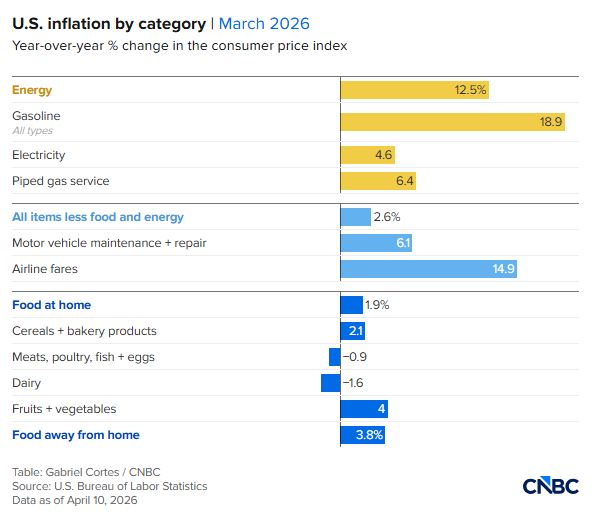

Data show March CPI rose 0.9% month-on-month and 3.3% year-on-year; but core inflation (excluding food and energy) only rose 0.2% month-on-month and 2.6% year-on-year, still above the Fed's 2% goal but showing a downward trend.

The Producer Price Index (PPI) shows similar divergence: overall up 0.5%, core up only 0.1%.

Additionally, the New York Fed survey shows one-year inflation expectations at 3.4%, lower than the University of Michigan's 4.8%, indicating the market remains divided on the inflation outlook.

Global Spillover Effects and Supply Chain Pressure

The war's impact is not limited to the United States. Since Europe and Asia have greater dependence on Middle Eastern energy, their shocks may be bigger.

Skordeles said: "Right now it’s more of a price shock rather than a supply shock. The impact is greater on Asia because of higher energy dependence."

The war has already disrupted global supply chains. The New York Fed’s global supply chain pressure index reached its highest level since January 2023 in March.

However, overall, the market still views the shock as manageable.

"While energy costs are up, they're still not extreme by historical standards," Skordeles said, "The economy will be affected, but it won't be a catastrophic result."

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.