Australian Bonds: Rate Hikes Suppression and Geopolitical Games

As global macro narratives shift, the overseas bond market has become a core window for observing asset allocation among major categories. Previously, our analysis focused mainly on the US Treasuries market; today, let's take a different approach and look at how Australian Government Bonds (ACGB) are being priced amid endogenous inflation pressures and Middle Eastern geopolitical variables.

1. Monetary Policy: Short-term Rates “Easy to Rise, Hard to Fall” under Rate Hike Expectations

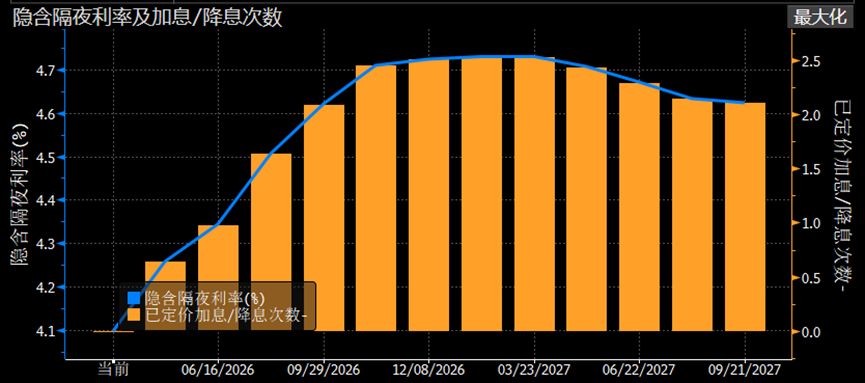

At the March policy meeting, the Reserve Bank of Australia decided to stop waiting and raised the target rate by 25 basis points to 4.10%. This move made it clear to the market: the core conflict of the current policy lies in overheated endogenous demand.

Inflation Driven by Endogenous Demand: Although global supply chain pressures have eased, the inflation rebound in Australia in the second half of 2025 mainly stems from strong domestic private demand and a tight labor market. RBA believes this internally-driven inflation is stickier than external imported inflation and must be effectively restrained by maintaining a high interest rate environment. This logic ensures very strong policy rigidity for short-term rates.

Internal Divergence Among Decision Makers: This rate hike passed with a narrow 5-to-4 margin. The divided vote suggests that future policy decisions will depend on short-term economic data. However, this has not weakened market expectations of another 25bps rate hike in May. As long as the rate hike path continues, short-term yields will remain high.

Implied Australian Overnight Rate and Priced-in Rate Hike Counts

2. Long-Term Rates: A Game Between Geopolitical Volatility and the “Shock Absorber” Mechanism

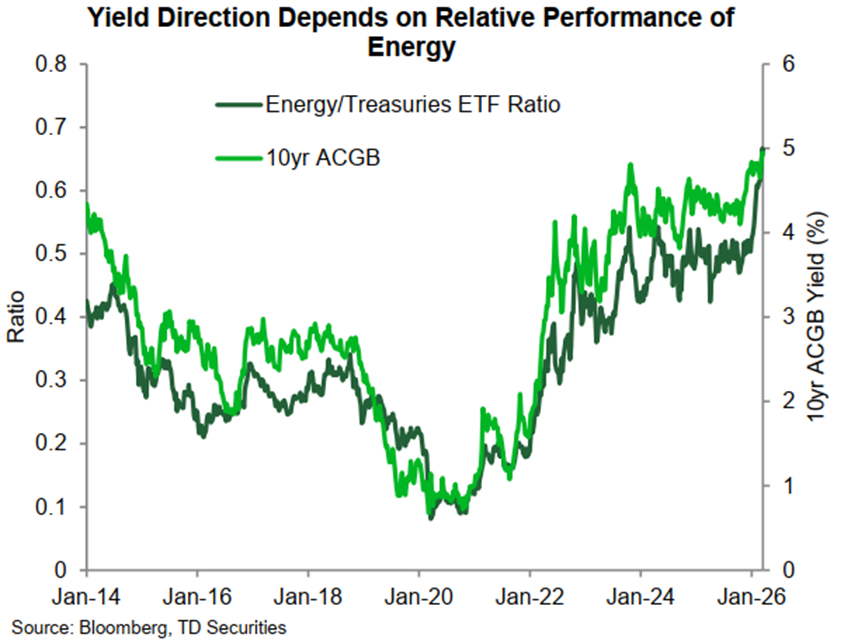

Recently, as the Middle East situation fluctuates, we observe that ACGB long-term yields are wavering at elevated levels amid geopolitical changes. The 10-year government bond yield swings widely around 5%, up and down 10bps, but has not made a further move upward. This is highly correlated with energy prices—under the “negotiation and confrontation” scenario, oil prices have not reached new highs.

Performance Synchronization of 10-year ACGB Yields and Energy/Bond ETF Ratios

From a long-term narrative perspective, as one of the world’s top three LNG exporters, Australia’s ample energy capacity gives it strong immunity to “imported inflation.” This means that inflation expectations embedded in long-term pricing are unlikely to include excessive external premiums, instead focusing more on the effectiveness of RBA policy. As RBA continues to maintain high rates to combat endogenous inflation, the market expects this tightening will ultimately produce a suppression effect on future fundamentals.

On the other hand, large-scale hedging operations by Australian pension funds (buying AUD) have supported a stronger exchange rate, creating a strong local currency environment that effectively offsets imported inflationary pressure. To some degree, this softens the most sensitive inflation premium risk in the long end of the bond market, leading to greater resilience for long-term yields to revert toward the mean.

3. Market Operation Strategies: Curve Flattening Trades Still Mainstream

Despite short-term geopolitics intensifying market volatility, we believe the central logic of yield curve "flattening trades" remains solid.

Our logic is that, once extreme expectations around the Middle East ease, the geopolitical risk premium in long-term yields will quickly fade, driving rates lower. At the same time, supported by RBA’s hawkish stance and rate hike expectations in May, short-term rates will continue to fluctuate at high levels. This combination—long-term rates falling as the geopolitical situation cools, short-term rates sustained by policy rigidity—will keep the curve spread moving flatter.

Although some institutions took profit in curve flattening trades amid mid-March volatility, against the backdrop that “insurance rate hikes” have not ended, repositioning for curve flattening is still the mainstream consensus in the market.

ACGB 2s10s Yield Spread Trend

4. Conclusion

In summary, Australian Government Bonds are currently in a cross-pricing period between endogenous inflation risks and external geopolitical uncertainties.

We expect that, in the short run, ACGB long-term performance will still fluctuate with Middle Eastern developments. But over a longer cycle, as RBA suppresses endogenous demand with high rates, the dampening impact of high interest rates on future inflation and economic growth will once again become the main theme for long-term pricing. Therefore, curve flattening continues to be the most certain direction.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.