Bitget UEX Daily | US-Iran Ceasefire Talks Advance; S&P 500 First Breaks 7000; TSMC and Netflix Earnings Today (April 16, 2026)

Bitget2026/04/16 01:32

Bitget2026/04/16 01:32

I. Hot News

Federal Reserve Developments

Fed Officials Signal Rates May Stay Elevated for Longer

- St. Louis Fed President Musalem noted that supply shocks are threatening both inflation and employment goals simultaneously, suggesting current interest rate levels may remain appropriate “for a considerable period”; he also lowered the 2026 GDP growth forecast to 1.5%-2% and expects inflation to approach 3% by year-end.

- In an interview, Trump threatened to remove Chair Powell from the Board if he remains after his successor is confirmed; Powell’s term ends May 15, with the hearing for his replacement nominee scheduled for April 21.

- CME data shows a 98.4% probability that the Fed will hold rates steady in April.

Ongoing Middle East tensions continue to weigh on corporate decision-making; combined with hawkish signals, this may support the dollar and cap further equity upside in the near term.

International Commodities

US-Iran Ceasefire Talks Progress, Oil Prices Under Pressure

- Trump stated that a US-Iran deal is “very likely” before King Charles III’s visit to the US in late April, with current odds “extremely high”; both sides are considering extending the ceasefire by two weeks to facilitate peace negotiations.

- Iran’s Foreign Ministry, via Pakistan mediation, continues dialogue but has not yet agreed to extend the truce, proposing free passage on the Omani side of the Strait of Hormuz while insisting it will not accept the US proposal in full.

- The White House described the talks as “constructive” and remains optimistic.

Ceasefire expectations are easing Strait of Hormuz tensions and temporarily reducing supply risks—positive for risk assets but capping any near-term oil price rebound.

Macroeconomic Policy

Fed Beige Book: Middle East Conflict Tops US Economic Uncertainty

- The economy remains in modest expansion but at a slower pace; consumption growth is slight, K-shaped divergence has intensified, low-income groups face rising pressure, and the labor market is in a “freeze.”

- AI is emerging as a structural factor influencing hiring, with most companies adopting a wait-and-see stance.

- The Senate once again rejected a Democratic resolution limiting Trump’s military options against Iran (47-52).

Middle East developments have become the primary variable for corporate planning; paired with hawkish Fed rhetoric, markets remain cautiously optimistic about economic resilience.

II. Market Review

Commodities & FX Performance

- Spot Gold: Mildly range-bound, currently around $4,830/oz, pulling back modestly for two consecutive sessions as ceasefire hopes dampen safe-haven demand.

- Spot Silver: Moving in tandem with gold, currently around $80/oz, supported by steady industrial demand.

- WTI Crude: Down approximately 0.43%, currently near $87.70/barrel, as ceasefire progress eases supply concerns.

- Brent Crude: Down approximately 0.19%, at $94.57/barrel, with geopolitical risk premium fading quickly.

- US Dollar Index: Eased slightly to around 98, as improved risk sentiment weighs on the greenback.

Cryptocurrency Performance

- BTC: Up 0.44% over 24H, currently around $74,793, holding above the $74,000 level after recent consolidation; ceasefire news supports risk appetite, though Fed hawkishness provides some counter-pressure.

- ETH: Up 1.16% over 24H, currently around $2,360, showing relative strength and clear signs of capital rotation.

- Total Crypto Market Cap: Up 0.2% over 24H, standing at approximately $2.61 trillion.

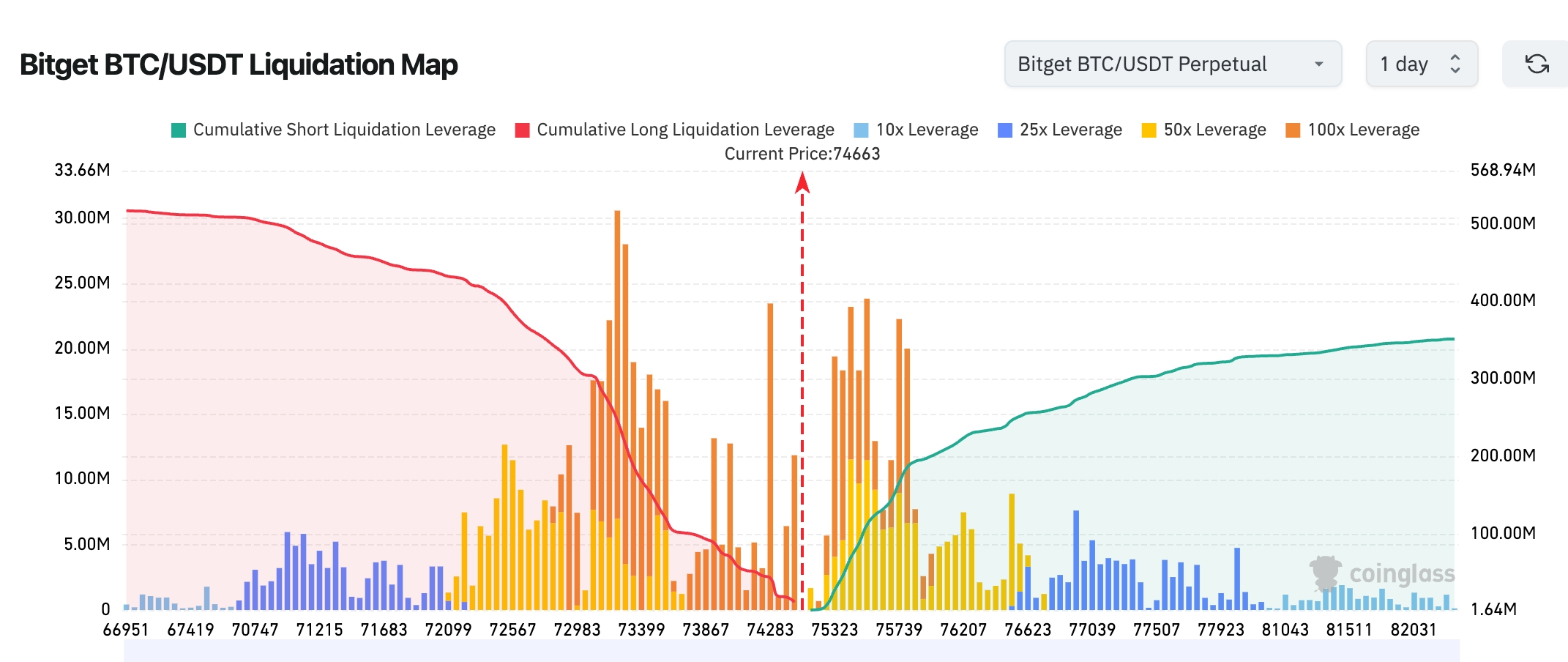

- Market Liquidations: $2.19 billion total liquidated in 24H, with short positions accounting for $1.41 billion.

- Bitget BTC/USDT Liquidation Heatmap: Price currently hovering near $74,663 at the multi-short/long liquidation boundary; lower red long-liquidation zones have largely cleared, while upper green short-liquidation clusters are building rapidly. The $75k–$78k zone is densely packed with shorts, creating potential for a short-squeeze rally, but downside support appears thin without fresh long-side fuel.

- Spot ETF Flows: BTC spot ETFs saw net outflows of approximately $106 million yesterday; ETH spot ETFs recorded net inflows of $26.6 million.

- BTC Spot Flows: Inflows of $2.008 billion vs. outflows of $1.965 billion yesterday, resulting in net inflows of approximately $43 million.

US Equity Index Performance

- Dow Jones: Down 0.15%, at 48,463.72 points, with relatively stable recent trading.

- S&P 500: Up 0.8%, at 7,022.95 points—its first-ever close above the 7,000 psychological level.

- Nasdaq: Up 1.59%, at 24,016.02 points, extending its winning streak to 11 consecutive sessions and setting fresh record highs, driven primarily by technology stocks.

Tech Giants Performance

- NVDA: $196.33 (+1.2%) — sustained AI compute demand

- AAPL: $266.43 (+2.94%) — Cook’s Nike share purchase boosts sentiment

- MSFT: $411.95 (+4.61%) — accelerated AI application rollout

- GOOGL: $337.12 (+1.26%) — SpaceX equity revaluation

- AMZN: $248.50 (-0.21%) — short-term profit-taking

- META: $671.58 (+1.37%) — steady advertising business

- TSLA: $391.95 (+7.62%) — A15 chip tape-out news

Core driver: Dual tailwinds from ceasefire optimism and improving earnings outlook, together with continued AI and new-energy themes, propelled the tech heavyweights and lifted major indices to new highs.

Sector Rotation Highlights

Nuclear Power / Quantum Computing Sector +8%+

- Representative stocks: Oklo +8%, D-Wave Quantum +22.63%, IonQ +20.95%

- Driving factors: Dual tailwinds from energy transition and surging AI compute demand; market optimism on long-term prospects for clean energy and quantum technology remains strong.

AI Application Software Sector +4-6%

- Representative stocks: Cloudflare +6.43%, Palantir +4.75%

- Driving factors: Accelerated enterprise AI deployment and faster real-world software rollout.

Semiconductor Sector mixed

- Representative stocks: ASML -4% (Q2 guidance missed expectations), Intel +1.77%

- Driving factors: Robust AI chip demand offset by weaker guidance from lithography leader; clear intra-sector rotation underway.

III. In-Depth Company Analysis

1. Tesla – A15 Chip Successful Tape-Out

Event Summary: Tesla announced successful tape-out of its next-generation A15 AI chip. CEO Elon Musk highlighted on social media that the chip “will become one of the highest-volume AI chips in the world.” Targeted at FSD autonomous-driving compute, Dojo supercomputer clusters, and Optimus humanoid robots, the milestone marks a critical step toward full AI hardware self-reliance, promising sharply lower reliance on external suppliers, improved efficiency, and strong support for Robotaxi initiatives—further reinforcing the “AI + Automotive” dual-engine narrative. Market Interpretation: Analysts widely view the development as validation of Tesla’s end-to-end AI hardware strategy, with potential to materially lift gross margins and unlock long-term growth; multiple brokerages note that A15 volume potential will further strengthen Tesla’s technological moat and drive valuation re-rating. Investment Insight: Progress from tape-out to mass production will be the key 2026 catalyst for Tesla shares—investors should closely monitor subsequent test data and deployment timelines to capture the long-term valuation upside from AI hardware autonomy.

2. Microsoft – Accelerated AI Application Rollout

Event Summary: Microsoft shares rose 4.61%, driven by deepening OpenAI collaboration and rapid global adoption of enterprise AI tools such as Copilot across Azure and Office suites, marking a clear shift from proof-of-concept to tangible commercial deployment that significantly boosts enterprise productivity. Market Interpretation: Wall Street analysts unanimously agree that Microsoft’s AI monetization has entered an acceleration phase, with Azure cloud growth picking up and subscription revenue contributing more; the cloud + AI engine synergy is becoming a clear differentiator. Investment Insight: Faster AI adoption further cements Microsoft’s leadership among tech giants; its cloud + AI dual-engine model positions it as one of the most reliable growth anchors for the full year.

3. Apple – Executive Increases Stake in Nike

Event Summary: Apple CEO Tim Cook recently added to his Nike position, filing shows he purchased 25,000 shares last Friday at approximately $42.43 each for a total of about $1.06 million, bringing his holding to 130,480 shares. As a Nike board member since 2005, the move is interpreted as management’s positive stance on cross-industry collaboration between consumer electronics and lifestyle brands, while also signaling confidence in the current consumption environment and Apple’s own ecosystem resilience. Market Interpretation: Institutions see Cook’s contrarian buying as an optimistic signal on consumption recovery, helping lift expectations for iPhone sales stabilization and sustained services growth—particularly notable given some Wall Street funds trimming Nike positions. Investment Insight: Rising services contribution and hardware-ecosystem synergy should provide long-term valuation support for Apple; continue to watch new hardware cycles and services revenue trends.

4. TSMC – Q1 Earnings Release Today

Event Summary: TSMC will release its full Q1 2026 results this morning; the market has already priced in the expected ~35% year-over-year revenue growth, yet the stock slipped 1.26% yesterday on some profit-taking. As the world’s leading foundry, its guidance carries benchmark significance for the entire semiconductor supply chain. Market Interpretation: Brokerages broadly expect strong demand for AI training and inference chips—especially advanced nodes and CoWoS packaging—to drive full-year results above consensus; focus remains on capex plans, 2nm process progress, and AI order visibility, with tight supply conditions likely to persist. Investment Insight: As the core semiconductor foundry play, TSMC’s earnings and guidance will serve as the key gauge of industry health—AI capex momentum deserves close attention.

5. Allbirds – Strategic Pivot to AI Compute

Event Summary: Footwear brand Allbirds announced a major transformation, exiting its core sneaker business to focus on AI computing infrastructure. The company will rebrand as NewBird AI and has secured up to $50 million in convertible debt financing; the shift is expected to complete in Q2. Initial steps include acquiring high-performance GPUs and offering compute access via long-term leases, ultimately aiming to become a full-stack GPU-as-a-Service and AI-native cloud provider—underscoring the market’s intense enthusiasm for AI compute themes. Market Interpretation: Institutions note that traditional consumer companies pivoting to high-growth tech are attracting strong investor interest; successful execution could reshape valuation multiples, though early-stage execution risks, competition, and capital efficiency remain watchpoints. Investment Insight: In an environment of accelerating AI theme rotation, transformation stories from legacy firms offer high optionality—investors should balance opportunity with execution uncertainty.

IV. Cryptocurrency Project Updates

- SoSoValue data shows XRP spot ETF net inflows reached $17.1142 million on April 15 (US Eastern time).

- Matrixport has fully closed its final 25,000 ETH long position (20× leverage), realizing a $17.32 million profit after holding for approximately 65 days.

- Ethereum DEX aggregator Kyber leads with ~31% market share, followed by CowSwap at 22%, while 1inch’s share has declined from ~30% to 15%.

- Onchain Lens monitoring reveals BlackRock withdrew 3,446 BTC worth $255.2 million from Coinbase in the past 8 hours.

- CryptoQuant Head of Research Julio Moreno noted that Bitcoin’s recent rally faces growing profit-taking pressure; multiple on-chain metrics signal rising selling pressure. Bitcoin broke above $76,000 on Tuesday to a new high since early February but has since pulled back near $74,800, now testing the $76,800 realized-price level for traders—a historical bear-market resistance that has capped rebounds multiple times.

- USDT issuer Tether transferred 951 BTC (~$70.47 million) from Bitfinex to its Bitcoin reserve address. The address has accumulated BTC at 15% of quarterly profits since 2023 and typically receives transfers shortly after quarter-end. It currently holds 97,141 BTC (~$7.2 billion), ranking as the world’s fifth-largest Bitcoin wallet.

- Strive, the listed Bitcoin treasury company, announced via CEO Matt Cole on X that it is raising the annual dividend yield on its product SATA by 25 basis points to 13.00% and has additionally purchased 27 BTC, bringing total holdings to 13,768 BTC.

- Arkham monitoring shows Morgan Stanley’s spot Bitcoin ETF MSBT has purchased $83.6 million worth of BTC since its launch this week; the on-chain address currently holds $64.4 million.

V. Today’s Market Calendar

Economic Data Release Schedule

| 20:30 | US | Initial Jobless Claims | ⭐⭐⭐⭐ |

| 21:15 | US | Industrial Production MoM | ⭐⭐⭐ |

| 22:00 | US | Philadelphia Fed Manufacturing Index | ⭐⭐⭐ |

Key Event Preview

Thursday, April 16

- TSMC reports Q1 results pre-market; Netflix reports Q1 results after the close ★★★★★

- US weekly initial jobless claims (week ended April 11)

- Fed officials deliver multiple speeches; Fed releases Beige Book—any hawkish tone could weigh on risk appetite ★★★★★

Friday, April 17

- Earnings season continues with possible regional banks or smaller tech names; markets may enter weekend caution mode.

Overall Weekly Strategy Note: Earnings delivery and Fed hawkish signals will dominate sentiment. Continue monitoring Iran developments and US-Iran negotiation follow-through; focus on structural opportunities in banking, technology, energy, and semiconductors.

Institutional Views

Multiple investment banks note that advancing ceasefire talks combined with improving corporate earnings outlooks are jointly fueling the risk-asset rally; the S&P 500 and Nasdaq hitting record highs reflect the market’s immediate reaction to reduced geopolitical risk. Morgan Stanley and Goldman Sachs both argue that although the Fed’s “higher for longer” rhetoric temporarily caps rate-cut expectations, lower Middle East uncertainty should support a rebound in corporate capex, keeping technology and AI themes as the dominant narrative for the year. In crypto, institutional flows are visibly rotating from Bitcoin ETFs toward Ethereum, with Bitwise analysts expecting ETH’s relative strength to persist into Q2. Overall, near-term risk appetite is improving, but investors should remain alert to any renewed hawkish Fed commentary or oil-price volatility that could re-ignite inflation concerns. Favor high-conviction growth assets while keeping a close eye on further geopolitical negotiation developments.

Disclaimer: The above content is compiled by AI search and manually verified for publication only; it does not constitute any investment advice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.