Middle East risk subsides, US stocks rebound; Goldman Sachs says rally needs Fed to resume rate cuts

The Middle East situation has further eased, with Iran announcing that the Strait of Hormuz is now “fully open” to commercial shipping. Prior to this, U.S. stocks had already rebounded sharply. As geopolitical risks recede, Goldman Sachs believes that in order for U.S. stocks to maintain their current rally, the Federal Reserve will need to pivot back toward a rate-cutting stance.

Christian Mueller-Glissmann, head of asset allocation research at Goldman Sachs, described the recent strong rebound in U.S. stocks as a “fast and fierce recovery phase,” and noted that part of the rebound was driven by technical factors—including hedge funds that had previously sold stocks to reduce risk are now being forced to rebuild positions.

Although the S&P 500 appears to be on track for a third consecutive week of gains exceeding 3%, Mueller-Glissmann still questioned whether this rally can be sustained without monetary policy support. He pointed out that the Fed needs to return to a rate-cutting stance to maintain the current upward momentum in U.S. stocks.

In an interview, Mueller-Glissmann said: “To sustain this recovery, to keep this rally going, I think we need the Fed to some extent to revert to its previous policy stance. We need to see some relief from rate pressures.”

He also noted that despite the sharp rise in the stock market, oil prices remain high and the credit market’s performance lags behind the stock market. He attributed part of the stock market’s strong performance to higher exposure to tech stocks, which continue to “deliver good results.”

The Fed is stuck in a policy dilemma

Although investors have recently chosen to treat Middle East war headlines as trading noise, and have returned to U.S. stocks—especially tech stocks—on the back of resilient corporate earnings in the latest earnings season, the negative impact of this conflict on U.S. economic growth and inflation cannot be ignored.

The Fed’s “number three,” New York Fed President Williams, said Thursday that the Middle East conflict has begun to have a tangible impact on the U.S. economy, manifested in higher price pressures and slowing economic growth momentum. Speaking to regional banking executives, he said the conflict has further exacerbated the uncertainty surrounding the U.S. economic outlook. While he still expects the economy to continue growing this year and inflation to gradually decline, he also admitted the Fed is facing the dual risks of rising inflation and economic slowdown.

Williams said that if disruptions in energy supply can ease quickly, energy prices should fall and the related shocks could partially reverse later this year. But he also warned that if the conflict evolves into a larger supply shock, it could further push up inflation and depress economic activity by raising input costs and commodity prices. This trend is “already starting to show.”

St. Louis Fed President Musalem also stated, “Supply shocks are threatening the Fed’s dual mandate on inflation and employment,” and pointed out, “The current rate range may remain appropriate for some time.” He added, “The oil price shock may be feeding into core inflation, which means core inflation could stay close to 3% through the end of the year.”

Even Fed Governor Milan, who has always supported bigger and more frequent rate cuts, has recently moderated his stance. On Thursday, Milan said he has pulled back from his position on rate cuts because inflation is proving more stubborn, and he now sees less justification for a looser monetary policy than before. He previously expected four rate cuts this year but now leans toward three.

Milan said that since December of last year, inflation has worsened, but it’s not entirely caused by the Middle East war. In fact, he observed this trend months before the conflict broke out. Milan pointed out that the underlying drivers of inflation have become more complicated: “Some other sectors have started contributing more, so the situation is more complex than it was at the start of the year.”

Milan currently believes that the Fed should move toward a neutral interest rate, which could be as low as 2.5%. He expects the inflation rate to hit the Fed’s 2% target in about a year. Regarding the job market, Milan sees no reason why the labor market cooling shouldn’t continue. Given labor market weakness, he is in favor of cutting rates now.

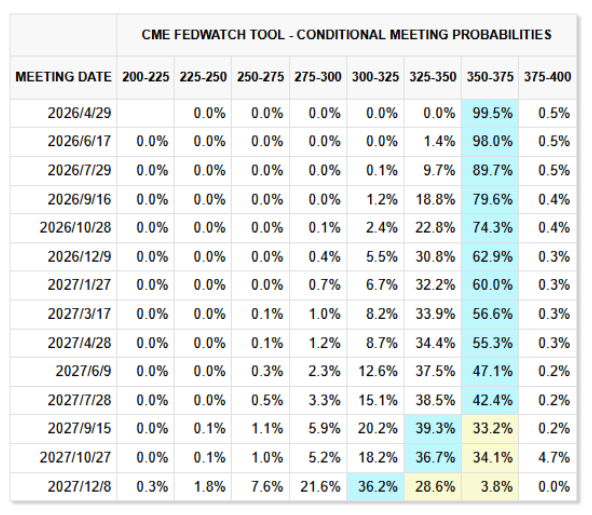

Overall, the dual risks of rising inflation and slowing economic growth stemming from the Middle East conflict are putting the Fed in a decision-making bind. As of press time, CME “FedWatch” tool shows the market estimates a 62.9% probability that the Fed will keep the benchmark interest rate unchanged through the end of 2026.

At the March 17–18 monetary policy meeting, the Fed announced it would keep the federal funds rate target range at 3.5% to 3.75%, the second straight meeting with no change. Although most officials still expect at least one rate cut this year in forecasts released after the meeting, the March meeting minutes show growing concerns.

Many policymakers emphasized that upside risks to inflation could ultimately require a rate hike. The likelihood of inflation remaining above the 2% target for longer has risen considerably. The March minutes indicate that the vast majority of participants judge that the progress toward the 2% inflation target has been slower than previously expected, and the risk of inflation staying well above target has increased.

Meanwhile, most officials worry that if the conflict drags on, it could affect the labor market, requiring rate cuts. Many warned that with new net job creation at low levels, the job market is vulnerable to negative shocks. A protracted Middle East conflict could dampen business sentiment and lead to further hiring pullbacks.

In fact, even before the current Middle East conflict erupted, the Fed's room to cut rates had narrowed—the labor market had stabilized, easing recession fears, whereas progress on inflation falling to the Fed's 2% target had stalled.

Taken together, information released in the Fed’s meeting minutes and the current market conditions suggest that the probability of the Fed leaving rates unchanged in the short term is highest, and the likelihood of an immediate rate hike or cut is low. On the threshold for hiking rates, while a few officials remain open to the idea, most judge that it's “too early” to assess the economic impact of the Middle East situation and prefer a cautious wait-and-see approach.

On the conditions for a rate cut, the minutes clarified the scenarios that would trigger further cuts—namely, if the Middle East conflict continues and labor market conditions deteriorate further, the pace of cuts could accelerate. The stronger-than-expected March U.S. nonfarm payrolls data, however, do not fit this scenario and temporarily ease the urgency for a near-term Fed rate cut.

Some analysts say the direction of Fed monetary policy will largely depend on external variables beyond its control, namely the duration and intensity of conflict in the Middle East. In this situation, Fed policy is likely to show “wait-and-see—wait for data—act accordingly” characteristics.

The Fed will announce its rate decision on April 29. This decision will be a key test for the outlook of Fed monetary policy. The market currently generally expects the Fed to keep rates unchanged at that time. Therefore, any change in wording in the decision statement or comments from Fed Chair Powell at the press conference will be critical in shaping market expectations around the path of monetary policy.

If the Fed Chair succession doesn’t go smoothly, Trump’s hopes for rate cuts could be dashed

Meanwhile, the process of the Fed Chair “handover” is currently not going smoothly, which may become a variable influencing Fed policy direction.

The U.S. Senate Banking Committee is expected to hold a confirmation hearing next week for Walsh, Trump’s nominee for Fed Chair. The hearing will serve as a platform for Senators from both parties to scrutinize Walsh's views on economic and monetary policy. Walsh has served as a Fed governor and as an economic policy advisor to Trump. Investors are especially focused on how Walsh will strike a balance between two competing forces—on the one hand, pressure from Trump to sharply lower borrowing costs, and on the other, economic conditions that are, at least in the short term, not yet favorable for rate cuts.

Given the Trump administration’s repeated attacks on the Fed, and inflation having exceeded the central bank’s target for over five years, any poorly handled response on interest rates could undermine the credibility of the Walsh-led Fed.

However, even if Walsh performs impeccably in the committee hearing, as long as the Department of Justice’s investigation into Powell continues, Walsh’s path to Senate confirmation remains uncertain. North Carolina Republican Tillis has said that, until the criminal investigation is resolved, he will not support any nominee, as he believes it threatens the Fed’s independence.

This week, Trump again stated that if Powell does not leave the Fed on time, he will take action to remove him. While Powell’s term as Fed Chair expires on May 15, his term as a Board member runs until January 2028. Traditionally, an outgoing Fed Chair leaves the institution entirely after their leadership term ends, but in March Powell said he would stay on until the Justice Department investigation is resolved “transparently and definitively.”

Trump said he does not plan to drop the Justice Department’s investigation into Powell and reiterated the need to investigate issues related to the Fed building project. This week, U.S. prosecutors raided the Fed’s headquarters construction site, which also indicates the Justice Department has not given up its probe of Powell, and earlier this month, U.S. District Judge Boasberg upheld a ruling to quash a subpoena against Powell.

If Walsh cannot be confirmed by May 15, Powell has said he intends to serve as interim Chair, and may also continue in his other key position—Chair of the Federal Open Market Committee (FOMC), which sets rates. This means the Trump administration’s continued investigation could not only delay Walsh’s confirmation, but also allow Powell to retain significant control over monetary policy.

Corporate earnings resilience is a critical pillar! Wall Street loudly bullish on U.S. stocks

Despite lingering Fed policy uncertainty, recent support from robust corporate earnings has prompted multiple Wall Street institutions to “strongly” endorse the outlook for U.S. stocks, and the market has begun to anticipate the start of a new bull run led by tech stocks.

Veteran equity market strategist and Fundstrat co-founder Tom Lee—dubbed “Wall Street’s super forecaster”—believes that both U.S. and global equity markets are currently stronger than they were when they last touched record highs earlier this year. Tom Lee agrees with a classic judgment from Wall Street giant JPMorgan: the technology sector—with a focus on AI compute infrastructure—will lead the next super bull market phase in equities.

Citi has upgraded its rating on U.S. stocks from “neutral” to “overweight,” and expects the S&P 500 to hit 7,700 points by the end of the year. The bank’s latest research report notes that technology, previously held back by geopolitics, valuation worries, and overly high expectations, is entering a window where risk appetite is shifting back to a revaluation of fundamentals. As Middle East tensions ease, the market has swiftly shifted from defensive to risk assets, with the S&P 500 and Nasdaq strengthening in tandem, indicating that capital is now betting on “future earnings growth driven by AI” rather than “current panic.” Under this framework, tech stocks, especially large tech platforms, are no longer just liquidity-driven crowded trades—they are reclaiming their status as the anchor for U.S. equity risk appetite and earnings expectations.

Asset management giant BlackRock’s equity strategists have also reverted to “overweight” U.S. stocks. BlackRock especially highlighted the new U.S. earnings season, loudly voicing confidence that the earnings engine can sustain the bull market. The strategists wrote, “Even during geopolitical conflict, corporate earnings expectations continue to rise, largely due to strong AI compute demand driven by AI investment themes.”

In summary, the new U.S. bull market narrative is underpinned by three main pillars: the corporate earnings resilience demonstrated in the latest earnings season, a new wave of risk appetite—led by tech/AI computing themes—and the market’s judgment that the Middle East shock will not turn into 2022-style long-term inflation. As long as these three pillars stand, and with Middle East tensions easing, U.S. stocks are expected to continue strengthening.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

XAU/USD slips below 4,550 after the Fed's most divided hold since 1992

NOMERC 24-hour volatility at 47.0%: Abnormal trading volume drives rebound amid low liquidity

Bitcoin, Ethereum Dip as Fed Holds Rates Steady for Third Straight Time