Observing the "second-round transmission" of European inflation from the perspective of consumption

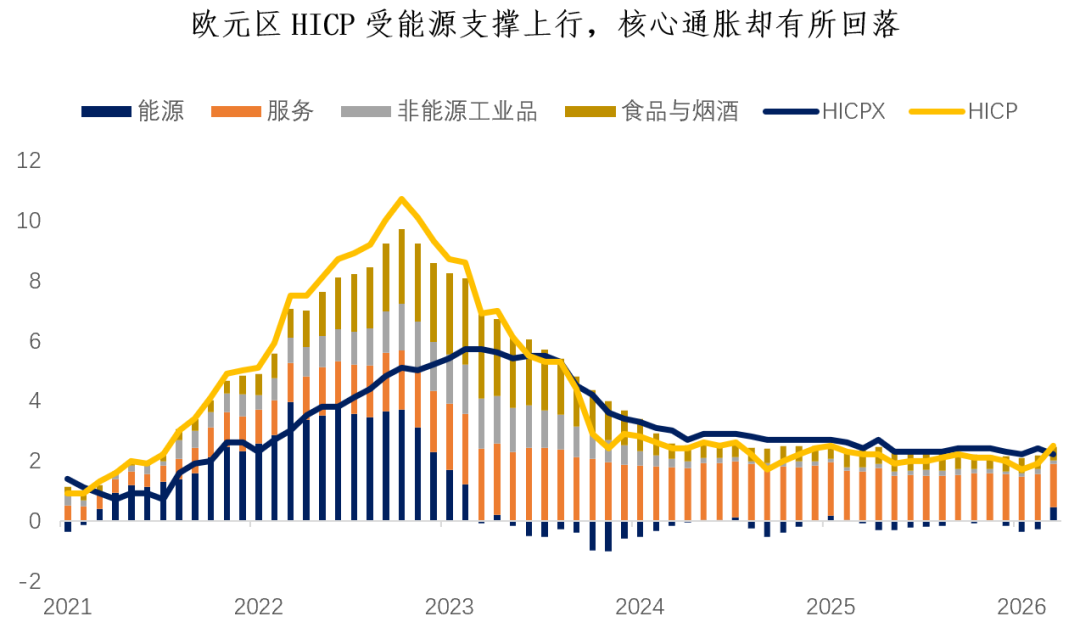

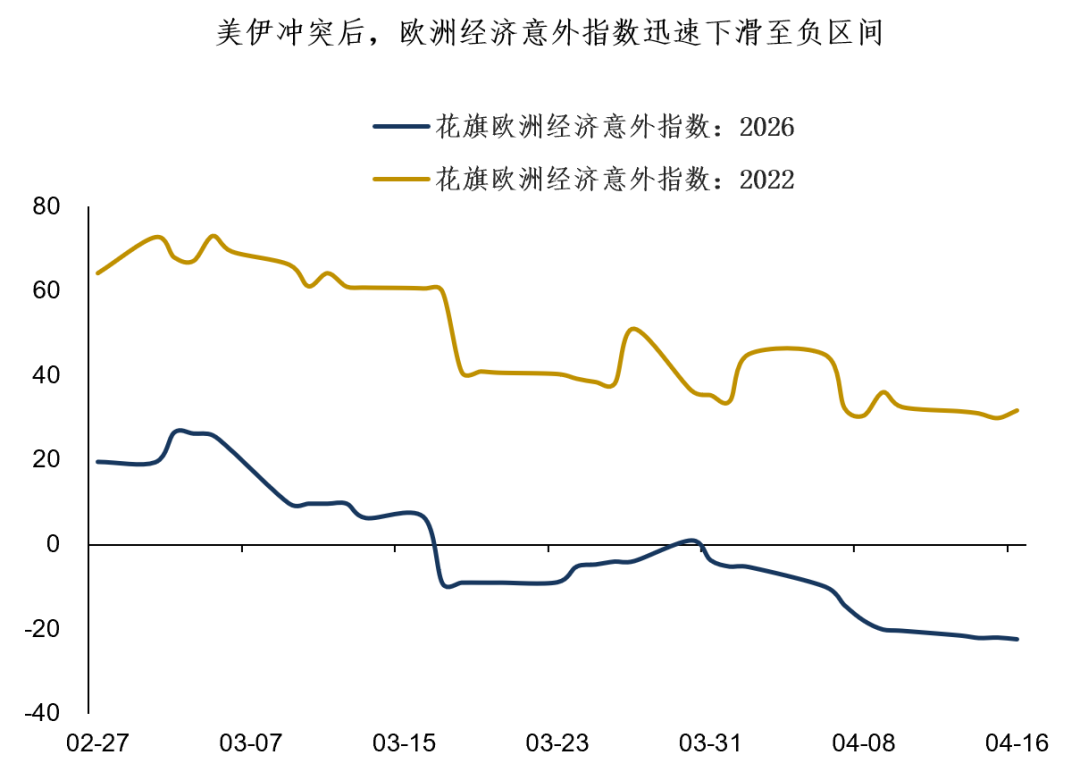

Amid the shockwaves of the US-Iran geopolitical conflict, energy prices have surged, causing Europe's HICP to soar to 2.5% year-on-year in March. However, unlike in 2022, the rise in oil prices has not been quickly transmitted to core inflation. With inflation in both the service sector and non-energy industrial goods declining, core inflation has edged down slightly to 2.3%.

Why hasn’t this round of sharp oil price increases promptly triggered a second wave of transmission to core inflation?

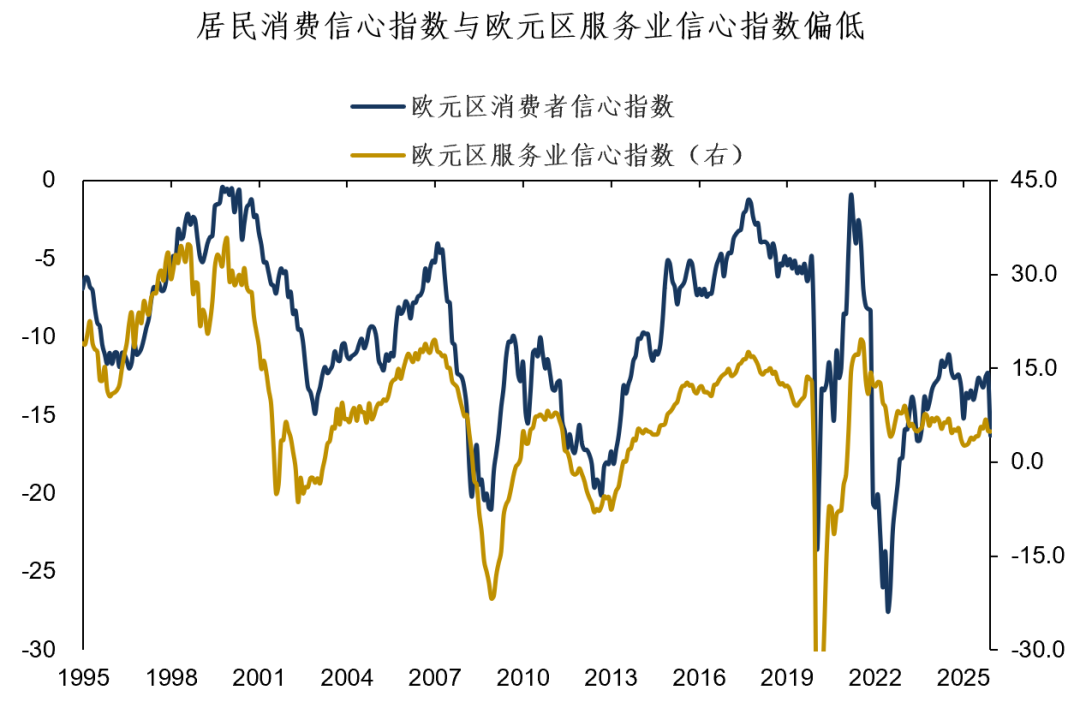

First, unlike the macro environment during the 2022 energy crisis, before the latest Middle East tensions erupted, the eurozone economy had already shown insufficient endogenous resilience, with significant GDP divergence and both consumer confidence and business investment at historically low positions. Downstream businesses have found it difficult to fully pass on the increased upstream energy costs to end consumers.

Can workers push up inflation by negotiating higher wages? A research report from Goldman Sachs indicates: The probability that this round will lead to a "wages + prices" inflationary spiral is limited for two reasons:

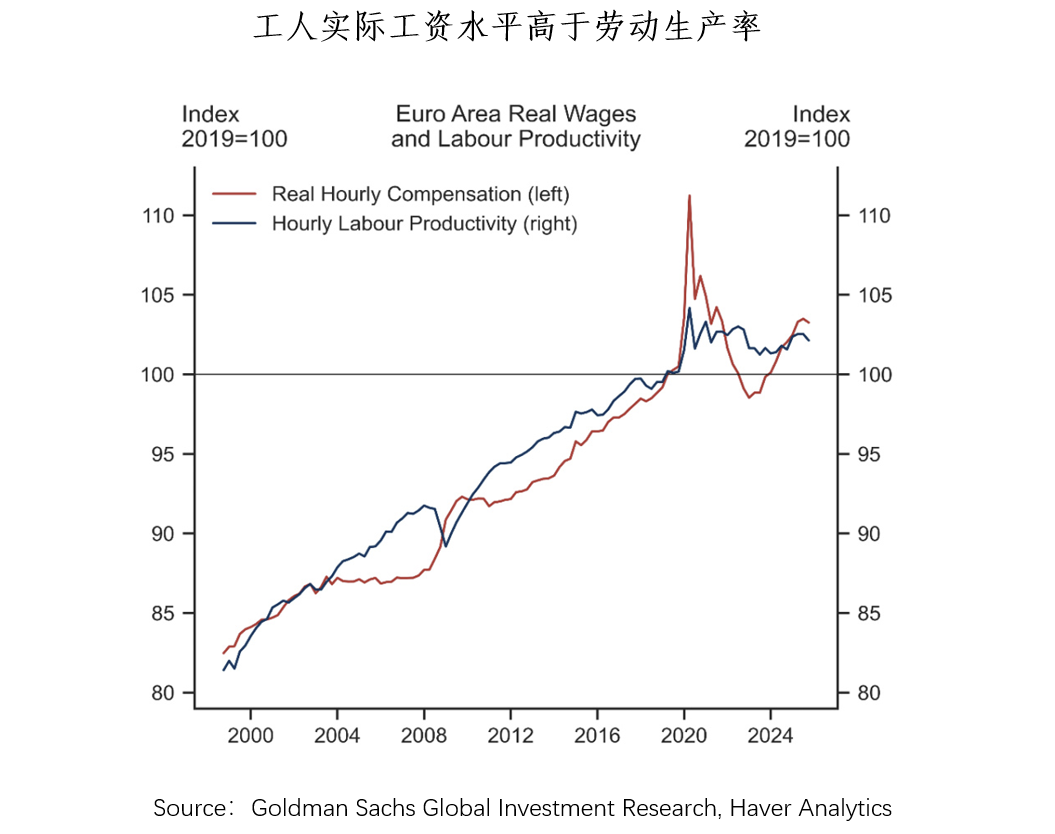

First, before the conflict, workers already had a purchasing power “buffer”. Before the conflict, real wages for European workers were slightly higher than labor productivity, and this gap should narrow gradually as the market adjusts. This means that even if rising energy prices erode purchasing power, companies still have room to resist nominal pay increases.

Second, the current labor market is somewhat looser than in 2022, with the job vacancy rate and employment rate estimates having returned to pre-pandemic levels. Workers’ bargaining power for higher wages has weakened. The recent energy price increases are expected to negatively impact the labor market, further constraining the recovery and improvement in real purchasing power.

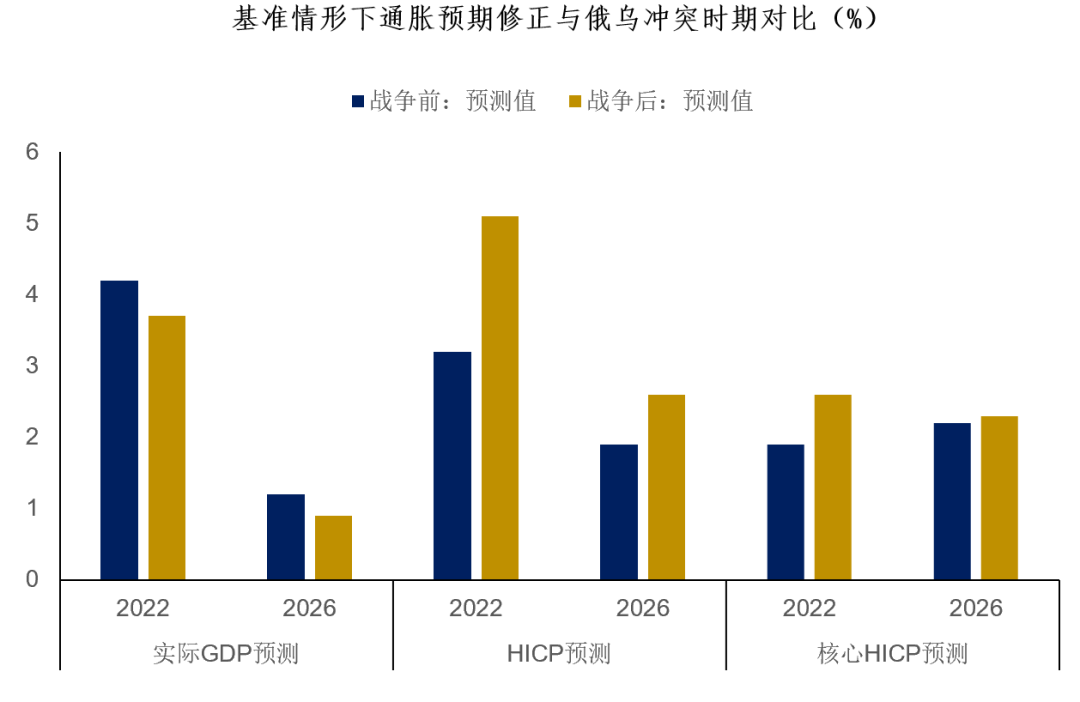

Based on the ECB’s inflation forecasts, if oil prices stay at the USD 90 baseline in the second quarter, 2026 inflation expectations have only been revised up from 1.9% to 2.6%, far below the 2022 revision from 3.2% to 5.1%. The ECB’s core inflation forecast is even more cautious: even under the adverse scenario where oil prices remain at USD 120 in Q2, core inflation in 2026 is only revised up from 2.2% to 2.4%.

In summary, from a consumption perspective, the “second round transmission” of inflation is relatively limited and controllable this time around. Considering the inherent fragility of the eurozone economy, it is unlikely to withstand the negative impact of an aggressive rate hike cycle. Thus, according to current data, “wait and see” is the ECB’s more prudent policy choice. However, if the US-Iran war continues to escalate, oil prices remain high, and imported inflation pressures build, rate hikes could be put on the agenda sooner.

To sum up today’s analysis:

1. Due to the eurozone’s lack of endogenous economic resilience before the outbreak of the current conflict, and unlike 2022, oil price increases have not quickly spilled over to core inflation, which has edged down to 2.3%.

2. With real wages above productivity and the labor market relatively loose, there is limited room for European residents to negotiate higher wages to compensate for lost purchasing power. The probability of a “wages + prices” inflation spiral is thus reduced.

3. Based on the current data, the ECB’s prudent policy option is “wait and see”, but if the US-Iran conflict continues to escalate and high oil prices drive up imported inflation, rate hikes could come onto the agenda sooner.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin: The New King of Safe-Haven Assets, A New Choice for Robust Portfolio Allocation

BLESS 24-hour volatility hits 40.8%: price surges sharply amid surging trading volume