$19 to $80: In 9 months, Intel goes from "AI abandoner" to "all-time high"

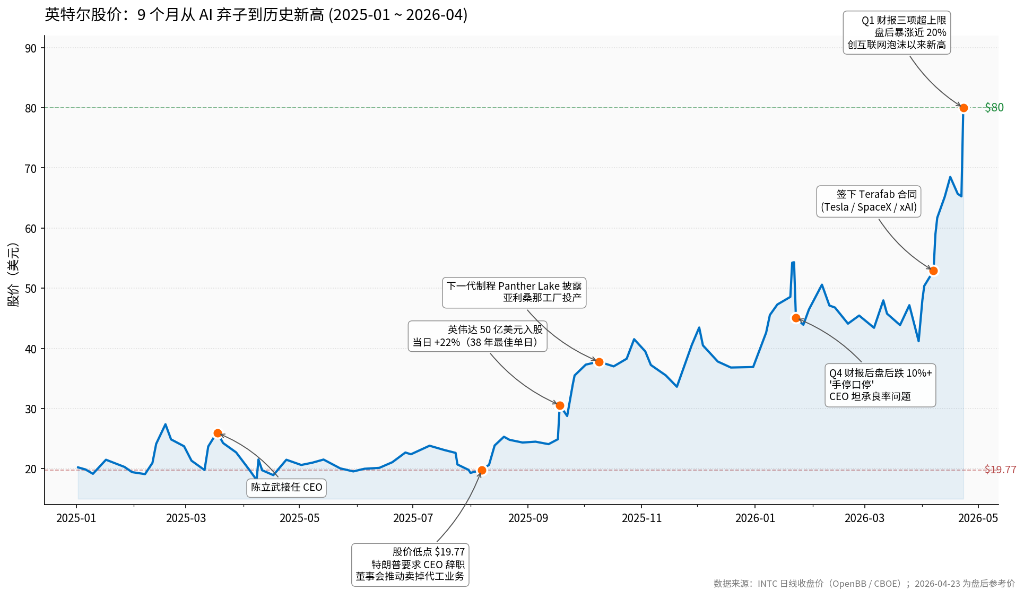

On the morning of August 7, 2025, Intel's stock price fell to $19.77.

This was the fifth month of Chen Liwu's tenure as CEO, and it was also his worst day. A few hours earlier, Trump had posted on social media demanding that he resign immediately, accusing him of a "serious conflict of interest." Inside Intel, Chairman of the Board Frank Yeary was pushing an even harsher plan—selling Intel’s foundational wafer foundry business directly to TSMC. On paper, it made sense: with years of losses, the foundry segment had long been a drag on the stock price, but if this really happened, Intel would be reduced to a pure chip design company—half of it effectively carved out.

On that day, Intel's market cap was $89 billion, just one-fiftieth of Nvidia's. The few words Wall Street used when mentioning the company—bankruptcy, breakup, sell-off—hinted at one thing: the AI era’s narrative had nothing to do with Intel anymore.

Nine months later, after the close on Thursday, April 23, 2026, within half an hour of opening, Intel's stock price surged nearly 20%, approaching $80. This was a height unseen since the dot-com crash, with the company’s market value growing by $49 billion in one day—more than a quarter of AMD’s entire market cap that day.

And of the 34 Wall Street analysts tracking the company, as of Wednesday’s close, 24 still rated it as "hold"—with an average target price of $55.33. By then, Intel’s stock price was already at $66. The options market priced in a 9.3% swing pre-earnings, but the actual move was over twice that. Even hedge funds were caught off guard.

It took only nine months for this company to go from an AI outcast to an AI darling. This wasn’t something a single earnings report could explain. Two independent storylines converged—advancements in AI technology returned CPUs from the role of obsolete hero back to a data center essential, and Chen Liwu leveraged a set of "anti-Intel traditions" to seize this unexpected windfall.

What Really Changed Was the CPU's Role in AI

Over the past two years, Intel’s position in capital markets was clear: every segment of the AI story left it out. Nvidia dominated the training side, with GPU prices soaring and customers lining up in batches. The CPU, once the protagonist of the last era, was sidelined by default. By 2023, Intel’s data center business was all but written off by Wall Street—the prevailing notion was it was the "aftermath of Nvidia's crush."

Then, something began to shift quietly.

As enterprise AI shifted from "training models" to "putting those models to work," especially as large-scale deployment of various AI agents became reality, the nature of computing changed. Training is a one-off large matrix calculation on massive datasets—a GPU specialty. But when an AI agent actually runs, it does much more than "think": parsing instructions, calling external tools, reading files, managing memory, orchestrating execution order, interfacing results with another agent—all these essential, intricate tasks occur on the CPU. The GPU handles one to two seconds of "thinking," while the CPU provides the bulk of sustained operations.

In March 2026, Gartner provided a hard number: In 2026, enterprise AI inference spending will overtake training for the first time. Cloud computing spending related to inference will climb from $9.2 billion in 2025 to $20.6 billion, and continue to double over the next four years. TrendForce’s calculations were even more direct—in the era of widespread AI agents, the CPU-to-GPU ratio in servers is expected to shift from the current 1:4 or 1:8 toward 1:1 or 1:2, meaning absolute CPU demand will multiply several times. Over the next four years, annual CPU demand growth will outpace GPUs and other AI accelerators.

The CPU market is expanding—not being eroded. Intel's Xeon server CPU product line still holds roughly 70% of the entire server CPU market share. While AMD is catching up, the overall pie is growing, so Intel’s absolute revenue is rising. In Q1 2026, Intel’s Data Center & AI revenue was $5.1 billion, up 22% year-over-year. This division, which was the most difficult to talk about under Nvidia’s shadow in 2023, has now become Intel’s fastest growth engine. AI-related business already accounts for 60% of Intel’s total revenue, up 40% year-over-year.

Intel’s CFO said on the earnings call, "CPU is experiencing a renaissance"—nine months ago, this sounded like management's pep talk. But put in the context of Gartner’s inflection point, the weight of that statement is quite different.

Chen Liwu Seized the Opportunity—But With an “Anti-Intel” Playbook

What connects Chen Liwu in March 2025 with Intel in April 2026 is what he did in these nine months.

This 65-year-old chip veteran from Malaysia acted boldly in his second month in charge—a 15% layoff, cutting 24,000 positions and reducing staff from 96,400 to around 75,000. He’s not a gentle reformer. Back in 2008, when he took over troubled Cadence, he used the same approach: restructuring, focusing on core business, cutting all non-essential spending. Twelve years later, Cadence’s stock price had risen 3200% by his departure.

He brought the same methods to Intel, with some escalation. Planned multibillion-dollar factory expansions in Europe were axed, Ohio projects slowed, and upper management was halved. His memo to all employees became widely quoted: "No more blank checks—every investment must make economic sense." His venture capital background shone through: instead of treating Intel as a tech giant, he managed it as a company needing to survive tough times.

The moment that made Wall Street raise its eyebrows happened on September 18, 2025. That day, Nvidia announced it would subscribe to $5 billion worth of Intel common shares at $23.28 each; the two companies would co-develop chips—Nvidia GPU units would be integrated into Intel’s PC processors, and Intel server CPUs would provide compute power for Nvidia’s AI clusters. News of this collaboration sent Intel’s stock up 22% in one day—the company’s best single-day performance in 38 years.

A company whose identity was once defined by its closed x86 ecosystem opened its doors to a former rival. Before Chen Liwu, this was unimaginable. His predecessor Pat Gelsinger took a different route—trying to catch up with internal technology and massively building out their own fabs, hoping to single-handedly put Intel back on track. He failed. Chen Liwu changed course: asset-light operation, inviting outside capital, treating external clients as lifelines. From September to November, three significant external investments landed in quick succession—$8.9 billion from the U.S. government for about 10% of Intel, Nvidia’s $5 billion, and $2 billion from SoftBank Japan. In total, $12.7 billion, representing a 16% stake. For the first time in history, Intel welcomed the government, strategic investors, and its old rival onto its shareholder register simultaneously.

The most intense game of these nine months took place in the boardroom. Throughout the summer of 2025, Chairman Frank Yeary repeatedly sought to spin off or sell the foundry business directly to TSMC. On paper, it made sense: the foundry segment lost money every year, draining cash flow and valuation. Chen Liwu stood almost alone against the opposition. His bet was straightforward—the age of AI inference is coming, and the foundry must be retained. This internal struggle delayed a multi-billion dollar financing plan, and an AI startup acquisition intended to catch competitors was lost to a slower board review.

At CES in January 2026, Chen Liwu took the stage to personally launch Intel’s first batch of next-generation process chips, and the Arizona factory went into full production. It was his first real “delivery” since taking office. But before the market could fully absorb the optimism, Q4 earnings hit—with Q1 2026 guidance at only $12.2 billion. On the analyst call, the CFO described the supply-demand status as “hand-to-mouth,” meaning factory output and customer deliveries left no buffer inventory. Chen Liwu admitted the factory yield rate was “still below what I want.” Intel’s stock fell over 10% after hours that day.

Three months later, everything turned around.

Two Deals Filled Half the Foundry Business’s Evidence Gap

The real trigger for analysts abandoning a “hold” stance after hours on April 23 was not the $13.6 billion revenue, nor the adjusted $0.29 EPS—which beat estimates by 29 times. What moved them were two contracts.

The first was Terafab. At the start of April, Elon Musk announced a $25 billion chip manufacturing joint venture. Tesla, SpaceX, and xAI—the “Musk ecosystem”—would provide both demand and capital, building a chip plant in Austin, Texas, to serve all of Musk’s commercial ventures, aiming to produce the equivalent of 1 terawatt of AI computing each year. Intel is the project’s chief foundry partner; this means their next-generation leading-edge process secured its first major external client—just months prior, external customer commitments for this process were zero. On April 22, Musk personally confirmed the partnership on Tesla’s earnings call.

The second was Google. That same day, Intel announced a multi-year server CPU deal with Google Cloud. Despite Google’s substantial investment in Arm-based server CPUs in recent years, this contract sent a clear signal—that for AI inference, Google’s answer wasn’t to wholesale replace Xeon with Arm.

The importance of these two deals is not the revenue size—Terafab’s financial terms aren’t even fully disclosed—but in their timing. Intel deliberately arranged for these announcements so the market would see the orders at the same time as the numbers. Q2 revenue guidance of $13.8 to $14.8 billion, with a midpoint $1.2 billion above consensus, is underpinned by these already locked-in orders. On the call, Chen Liwu stated, “Multiple customers are actively evaluating the next-gen process,” and “several are entering early technical engagement stages.” This wording is much firmer than "interested."

A year ago, the biggest concern among holdouts was uniform—Chen Liwu’s story sounded good, but the company had claimed “this time will be better” too many times before. What they got on April 23 was black-and-white contract evidence.

What Will the Market Focus on Next?

The move from $66 to $80 marked the first involuntary softening of the Wall Street “hold” consensus. For the next three months, the real re-rating path depends on two things.

First, actual Q2 delivery. Intel’s guidance range is $13.8 to $14.8 billion. If actual results hit the upper end (above $14.5 billion) and Data Center & AI continues growing 20%+ YoY, the last line of defense for holdouts will collapse. Second, when will the next-generation process land a second major external client that publicly signs? The clients Chen Liwu referenced as being in "early engagement" are rumored to include one or two of Google, Apple, AMD, or Nvidia—if any publicly confirms in the second half-year, Intel’s intrinsic valuation path to $90–100 opens. Both achieved, and that becomes the new anchor. If either is missed, returning to the $55 to $65 analyst average is baseline.

The first ripple effect will be in semiconductor equipment stocks. Intel ramping up next-generation production directly boosts the big three equipment suppliers—Applied Materials, Lam Research, and KLA. On April 23, the Philadelphia Semiconductor Index had risen for 17 consecutive trading days, a record, with Texas Instruments up 19% on the same day. The rally effect was already underway. The advanced packaging chain will benefit next—TSMC’s AI packaging capacity as well as U.S. and South Korean packaging/testing companies will profit.

The one under pressure is AMD. Over the last two years, AMD used its EPYC server CPUs to steadily erode Xeon’s territory, reaching a 39.4% share—now, the “Intel also benefits from AI inference” narrative partly offsets this. In the next quarter or two, watch for signs that AMD’s data center revenue growth begins to slow sequentially. There’s also Nvidia itself as a hidden beneficiary: last year, it acquired its $5 billion Intel stake at $23.28; at nearly $80, the gain is already over 3x. The mark-to-market profit on this strategic holding alone influences market sentiment and pricing.

It’s crucial to separate sentiment-driven rallies from fundamentals. AI PC stocks have risen in sympathy recently, but there’s no real support—Intel’s PC business grew only 1% YoY in Q1 and, though accounting for over half of revenue, showed nearly zero growth. The “AI PC” story has been told for two years, but a true replacement cycle hasn’t yet arrived. This type of sympathy rally lacks depth. NAND stocks like Micron and businesses indirectly tied to Intel foundry’s fortunes aren’t at the core of this move either.

The Second Half Signal Is the Q2 Earnings Report

In July 2026, Intel’s Q2 earnings will be the next pricing checkpoint. Focus on three things—whether Q2 revenue really hits $14.5 billion, whether Data Center & AI maintains 20%+ YoY growth, and management’s tone on second-half gross margins. Chen Liwu already warned on the Q1 call that cost pressure from memory and circuit board materials will be a significant headwind in coming quarters. This is the toughest negative factor for the next two quarters.

Watch in parallel for next-generation process clients going public. If another large external client signs in the second half year, that becomes the next lever for the stock price to climb toward $90.

Looking further ahead—November 2026 is U.S. midterms, and 10% of Intel is held by the U.S. government. If the election changes the attitude of this stake-holder, the “stabilizer” political undertone will be repriced by the market.

What Chen Liwu did in these nine months was not simply rescue Intel from the abyss. He returned a company nearly delisted from Wall Street back to the main battlefield of AI compute. The other half of this drama is—AI technology’s evolution happened to reach an inflection point in 2026, placing a comeback opportunity right in front of him. He caught it his way.

When does the second half begin? It all depends on Q2.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

TRADOOR fluctuates 40.1% in 24 hours: Trading volume surge and rapid price pump trigger major volatility

US Dollar Index (DXY) holds gains near 99.00 as geopolitical tensions grow

DXY: Fed repricing supports US currency – Deutsche Bank