Middle East conflict tears apart global pricing system, causing chaos across stocks, bonds, forex, and commodities

After the outbreak of the Middle East war, the traditional global asset correlations collapsed completely and have yet to recover. Investors have to rely on malfunctioning market indicators to piece together new trading strategies, struggling to navigate the evolving situation.

The S&P 500 Index reached new record highs, yet this masks multiple concerns including rising geopolitical tensions, prolonged disruptions in energy supplies, and profound economic scars.

Mark McCormick, Chief FX Strategist at Bank of Montreal, believes that in the next three to six months, markets will no longer be able to return to the pre-conflict normal.

In his research report, he points out: "The momentum of economic growth is recovering but remains weaker than end-2025 levels; policy interest rates remain high, asset correlations keep shifting, and the risk of asset drawdown is continuously increasing. A brand-new market landscape is taking shape."

The following analysis dissects the complete disorder in the classic interrelations among stocks, bonds, forex, and commodities—relationships that were once core references for economic outlook.

Fixed Income Market Faces Harsh Stress Test

Typically, equities and bond yields move together: when investors worry about economic downturns that could hurt equities, they buy bonds for safety, pushing down yields, and vice versa.

Since the pandemic, this correlation has continuously faltered. High inflation and high government debt have persistently undermined bonds’ traditional role as a hedge against stock market risks.

The International Monetary Fund warned in a pre-war blog post back in February: traditional hedging tools have fully failed, and investors and policymakers must restructure risk management systems for a new cycle.

The two-year short-term bonds, which are highly sensitive to inflation and interest rate expectations, are at the center of the current market volatility.

Over the past five years, the average one-month rolling correlation between the two-year U.S. Treasury yield and the S&P 500 Index was 0.23, but it has now plunged to -0.8; since the war broke out, this figure has stabilized at -0.63. The two-year German government bond yield versus the Euro Stoxx 600 Index is also showing the exact same abnormal pattern.

Michael Metcalfe, Head of Global Macro Strategy at State Street Global Markets, said: "In March this year, the market did not see the expected safe-haven buying of sovereign bonds, and there was simply no flight to safety in short-term bonds."

"This is a brutal test for the fixed income market; this shock combines both rising inflation and pressured growth, magnifying long-term fiscal risks," he added.

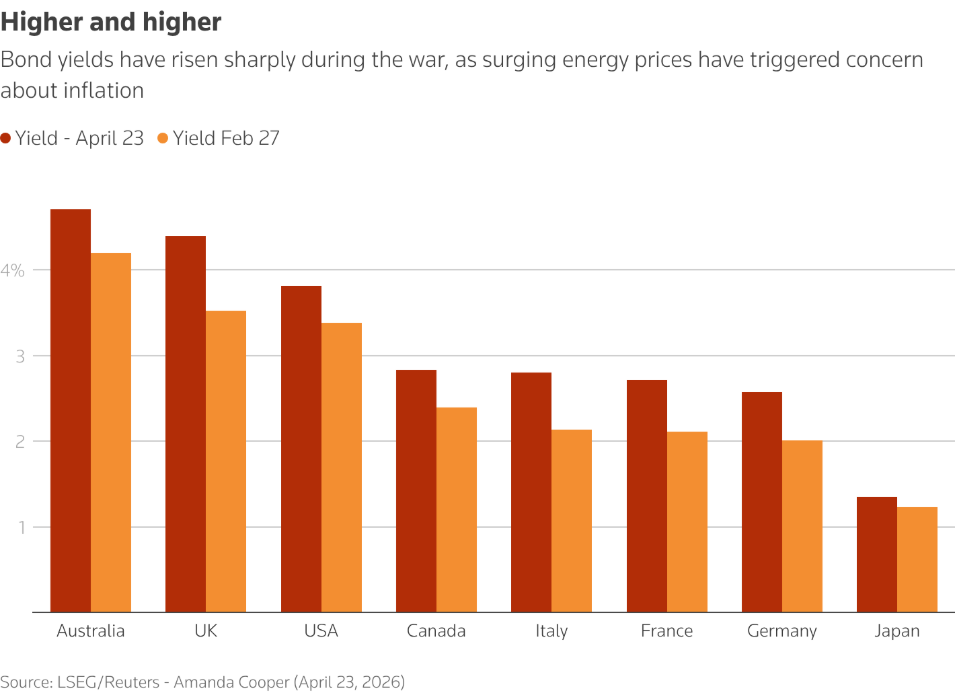

Sovereign bond yields surged during wartime, as rising energy prices triggered inflation concerns

Sovereign bond yields surged during wartime, as rising energy prices triggered inflation concerns Gold’s Price Action Becomes Completely Abnormal

Since the outbreak of this conflict, gold has completely lost its safe haven status and its performance has become abnormally tied to stocks and highly volatile cryptocurrencies. Gold is currently down 10% from its pre-war levels.

Historically, gold has maintained a strong negative correlation with the U.S. dollar. Whenever markets experience sharp volatility and investors dump stocks and risky assets, the dollar usually serves as the core haven—this has been true again during this war.

Since late February, the gold-dollar correlation coefficient has weakened dramatically from its five-year average of -0.4 to -0.19; the gold-equities correlation has climbed to 0.55, well above the five-year average of 0.22.

The key underlying factor is the extreme coupling between the dollar and stock market: this week, the inverse correlation between the dollar and the S&P 500 hit a record -0.94, nearly a perfect negative, well below the five-year average of -0.28.

At the same time, the correlation between bitcoin and the U.S. stock market has surged to a historic high of 0.96, far above the pre-war average of 0.4, completely destroying the value of diversified asset allocation.

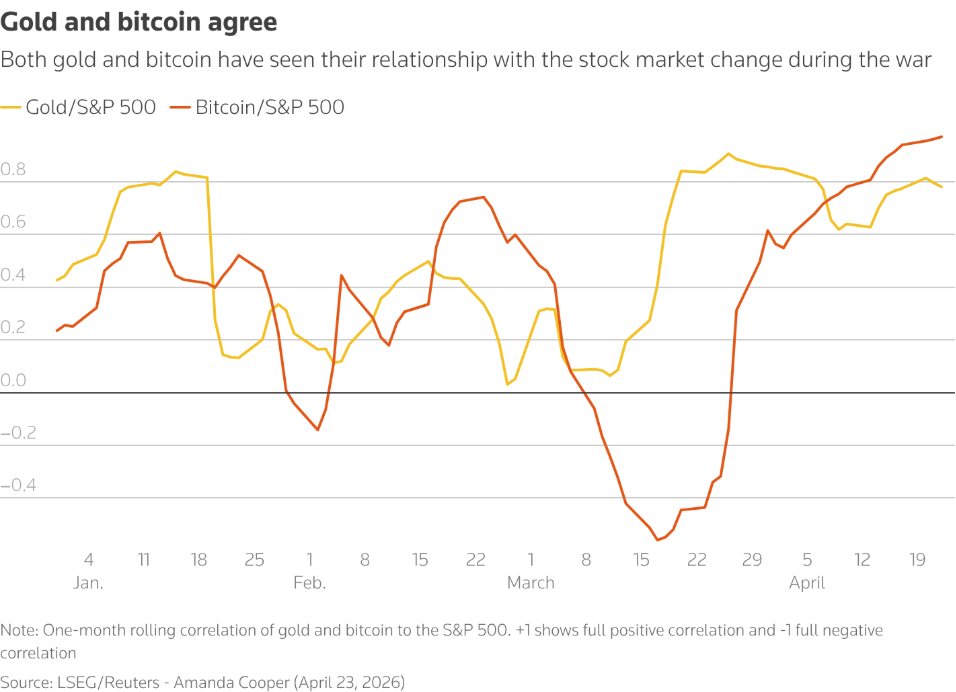

The traditional correlations between gold, bitcoin, and the U.S. dollar have both broken down

The traditional correlations between gold, bitcoin, and the U.S. dollar have both broken down Extreme Events Breed Abnormal Market Effects

As expectations for an inflation shock rise, traders are now betting on European rate hikes and a delay to Federal Reserve rate cuts.

Ordinarily, regional rate differentials directly drive shifts in currency strength, but this ironclad rule has now also broken down.

The market expects the European Central Bank to hike rates twice this year, while the Fed leans toward cuts. However, the euro against the dollar is only holding near 1.17 and has barely retraced any of its wartime losses.

UniCredit noted: "Major unexpected events can completely rewrite financial market patterns and disrupt the traditional logic of various indicators moving together." The bank added that the breakdown in the relationship between the euro-dollar rate and the transatlantic rate spread is a typical case.

Measured by the two-year U.S.-Europe swap rate spread, the current correlation with the euro rate is 0.5—close to zero at the start of the year, with a two-year average of -0.3.

UniCredit further states: "As long as the risk premium from the war persists, rate spreads will struggle to regain dominance in driving the euro exchange rate."

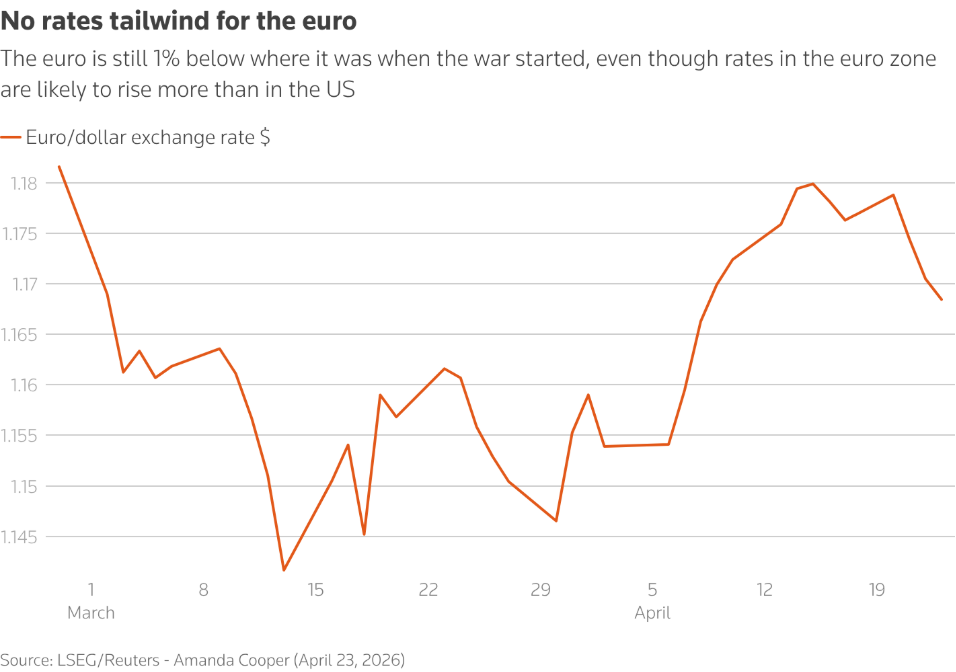

The euro has not benefited from rate spread advantages

The euro has not benefited from rate spread advantages Inflation Expectations Completely Decouple from Fundamentals

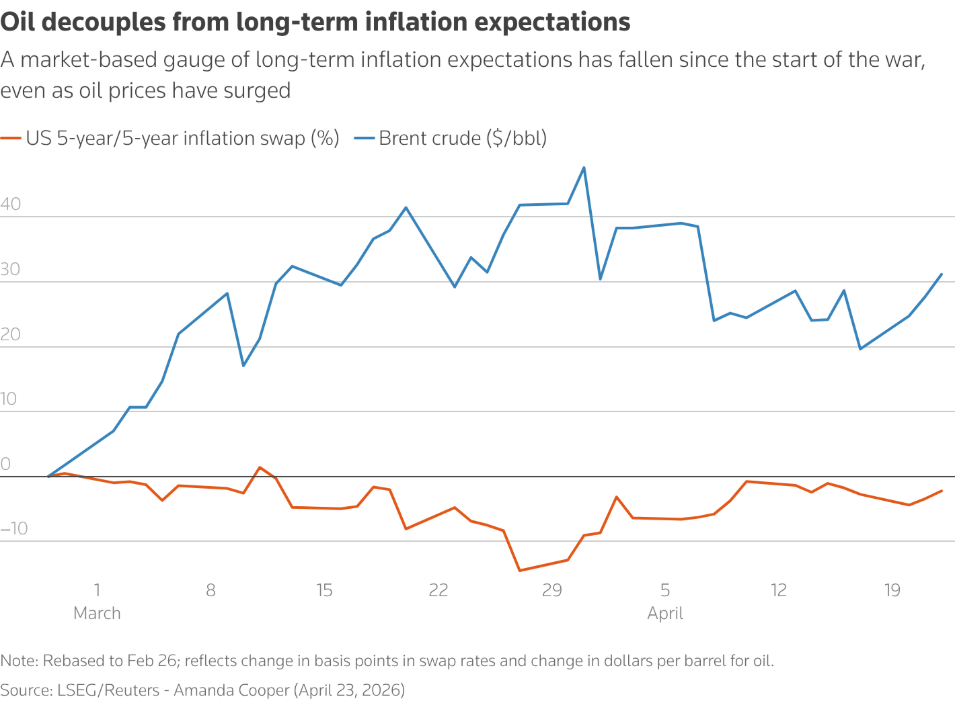

Historically speaking, a sharp rally in oil prices would boost inflation expectations, but in this conflict, the logic has completely flipped—inflation expectations are falling, not rising.

The five-year forward inflation swap rate, which measures long-term U.S. inflation expectations, has retreated from nearly 2.45% before the war to around 2.4%, while oil prices have still risen by about 40% over the same period.

The correlation between the two has dropped to -0.7, a complete reversal from the five-year positive average of 0.2; during the 2022 Russia-Ukraine energy crisis, the indicator once registered a strong positive correlation of 0.7.

Deutsche Bank believes expectations of increased U.S. fiscal deficits for the war are one of the reasons for this disconnect in logic.

"Another major factor is that forward inflation pricing has already seriously decoupled from economic fundamentals, substantially weakening its traditional reference value."

Oil prices are rising, but long-term inflation expectations are falling

Oil prices are rising, but long-term inflation expectations are falling Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

TRADOOR fluctuates 40.1% in 24 hours: Trading volume surge and rapid price pump trigger major volatility

US Dollar Index (DXY) holds gains near 99.00 as geopolitical tensions grow

DXY: Fed repricing supports US currency – Deutsche Bank