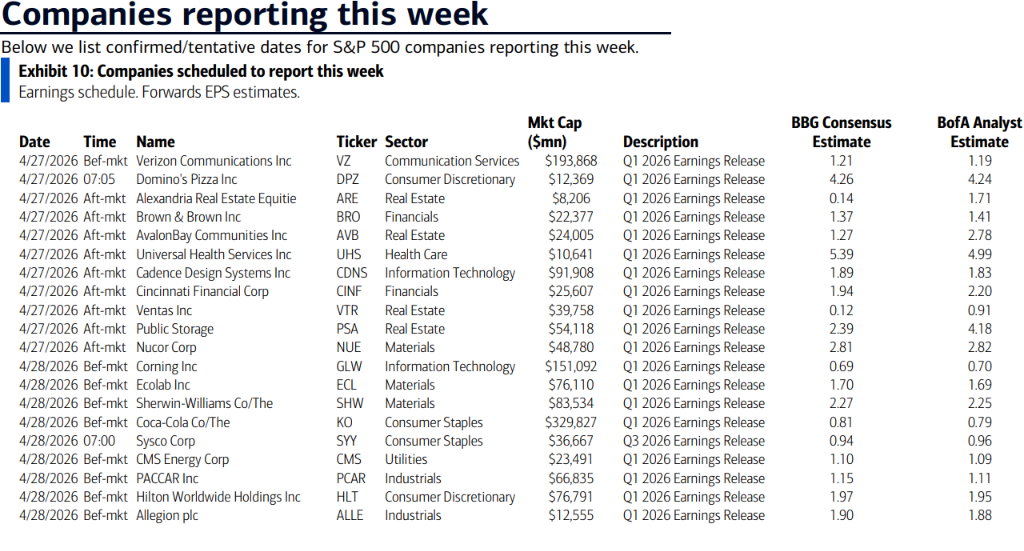

Amazon (AMZN) Q1 2026 Earnings Preview: AWS and Advertising as Dual Growth Engines

Bitget2026/04/28 04:22

Bitget2026/04/28 04:22Investment Highlights at a Glance

Amazon(AMAZ) is scheduled to report its Q1 2026 results after the U.S. market close on April 29, 2026 (early morning Beijing time on April 30). Wall Street consensus calls for revenue of $177.2 billion (+13% YoY) and adjusted EPS of $1.63.

The key investment themes center on whether the AWS cloud segment can sustain its accelerated momentum and whether the high-margin advertising business will continue delivering outsized profit contributions. At the same time, investors will scrutinize the company’s record $200 billion (+60% YoY) capital expenditure plan for 2026, focused on AI infrastructure. Strong Q4 2025 results have boosted sentiment, but near-term margin pressure from heavy CapEx remains the primary driver of potential stock volatility.

Bitget has now listed AMAZUSDT 100x Leveraged Contracts – Go Long or Short and Maximize Your Returns!

Three Major Focus Areas

Focus 1: AWS Growth Momentum and AI Monetization

AWS remains Amazon’s most important high-margin growth driver. In Q4 2025, AWS revenue accelerated to +24% YoY, fueled by surging demand for generative AI training and inference workloads. Enterprise adoption of large language models continues to ramp, positioning AWS for further acceleration.

Consensus expects Q1 AWS revenue around $36.8 billion with operating margin in the area of 35.7%. Progress on Amazon’s own chips (Trainium3 and Inferentia), deeper partnerships (including with Anthropic), and commercialization of AI services will be closely watched as proof points of AI monetization. If actual growth comfortably exceeds the mid-to-high 20% range, it should reinforce long-term confidence and support a positive stock reaction.

Focus 2: Advertising as the Second High-Margin Growth Curve

Advertising carries significantly higher margins than retail and is rapidly becoming a major profit pillar for Amazon. In Q4 2025, ad revenue rose +23% YoY to $21.3 billion, cementing Amazon’s position as the third-largest digital advertising platform in the U.S. The full rollout of ad tiers on Prime Video and increased seller activity have further enhanced this high-margin business.

Q1 advertising revenue is expected to maintain double-digit growth. Core products (Sponsored Products, Sponsored Brands, and Sponsored Display) leverage Amazon’s rich purchase-intent data for precise targeting. Continued gains in advertising’s revenue share and contribution to overall gross margin should help offset retail pressures and stand out as one of the brightest spots in the report.

Focus 3: Steady Retail Performance vs. CapEx Return Concerns

North America and international retail segments are projected to deliver stable expansion, supported by improved operational efficiency and strong third-party seller activity. However, the massive $200 billion 2026 CapEx budget—primarily directed at AI data centers, custom silicon, and high-performance networking—has raised investor concerns about short-term profit dilution. CEO Andy Jassy has highlighted plans to roughly double data-center capacity by the end of 2027, but the market is focused on the payback period.

If retail margins continue improving and CapEx execution remains transparent with clear ROI signals, worries should ease. Conversely, any guidance suggesting AI spending will weigh on Q2 profitability could trigger a pullback.

Risks and Opportunities

Upside Catalysts:

- AWS growth beating expectations (mid-to-high 20%+ range) combined with faster-than-expected self-developed chip commercialization.

- Further margin expansion from advertising, driving an EPS beat.

- Smooth execution of major AI partnerships (e.g., expanded Anthropic commitments), strengthening the long-term growth narrative.

Downside Risks:

- Overly large CapEx scale leading to cautious Q2 guidance and fears of extended payback periods.

- Heightened regulatory scrutiny on large tech investments and partnerships.

- Retail margin misses or weaker consumer spending due to macro headwinds.

Trading Strategy Suggestions

Bull Case: Strong beats in AWS and advertising, paired with credible ROI visibility on CapEx, could drive the stock toward fresh highs (implied move around ±7%, with upside targeting the $273 area).

Bear Case: Margin pressure or conservative guidance highlighting short-term AI investment drag may push shares back toward the $237 support zone.

Key Metrics to Watch:

- AWS revenue and growth rate

- Advertising revenue contribution

- Overall operating margins

- Q2 revenue and profit guidance

Actionable Ideas:

- Consider light positioning ahead of the print; add on clear beats or reduce on weak guidance.

- Monitor post-earnings volatility closely—ideal for event-driven short-term trades with tight risk management.

Disclaimer: This analysis is for reference only and does not constitute investment advice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

NZD/USD slips to 0.5900 as US-Iran tensions support USD; focus remains on FOMC meeting

Gold struggles below $4,700 as US-Iran tensions support USD ahead of FOMC meeting

BTW (Bitway) fluctuates 42.3% in 24 hours: Trading volume surge triggers sharp price volatility