Under "Oligopolistic Monopoly," HDD Prices and Quantity Soar! Bank of America Raises Target Prices for Major Manufacturers Western Digital and Seagate Technology

Zhihu Finance APP notes that Western Digital (WDC.US) and Seagate Technology (STX.US) have both maintained a clear trajectory of profit growth, which has prompted Bank of America to raise the stock price targets for both companies.

In an investor report on Monday, Bank of America analysts led by Wamsi Mohan stated: "As manufacturers have not increased unit production capacity, the supply of hard disk drives (HDD) remains tight, and we see this as a structural change. Therefore, we continue to see demand outstripping supply, and believe original equipment manufacturers (OEMs) still have room for further price increases."

Bank of America raised the price target for Seagate from $605 to $700, and raised the price target for Western Digital from $415 to $495. In a bull-case scenario, Bank of America finds that the total earnings per share (EPS) for both companies could increase significantly by 2028.

Seagate Valuation Analysis

When assessing Seagate, analysts noted: "We estimate that the current stock price of about $587 reflects 2028 calendar year EPS of $29 (based on a 4% CAGR in nearline storage price per TB and a 47% EBIT margin in the 2028 calendar year), and assumes a price-to-earnings ratio of 20x (which we believe is in line with Seagate's growth and margin profile). However, in a bull-case scenario, we think its EPS potential could reach $45 (when 2028 calendar year price per TB reaches $20, three-year CAGR of 16%, and EBIT margin reaches 55%)."

Western Digital Valuation Analysis

For Western Digital, Bank of America stated: "We estimate that the current stock price of about $400 reflects 2028 calendar year EPS of about $20 (based on a 0% CAGR in nearline storage price per TB, i.e., no growth, and a 45% EBIT margin in the 2028 calendar year), and assumes a price-to-earnings ratio of 20x (which we believe matches Western Digital's growth and margin profile). But in a bull-case scenario, we think its EPS potential could reach $33 (when 2028 calendar year price per TB reaches $20, three-year CAGR of 12%, and EBIT margin reaches 55%)."

As the two companies lock in long-term contracts with customers, business visibility continues to improve.

Wamsi added: "This market remains an oligopoly (with only three OEMs providing hard disk drives), and we believe the threat of new entrants is very low."

So far this year, the stock prices of Seagate and Western Digital have both more than doubled.

The Comeback of HDD "Veterans"

In an age where solid-state drives (SSD) are surging ahead, many once predicted that mechanical hard drives (HDD) would fade into insignificance. However, Bank of America's recent significant price target increases for Seagate and Western Digital serve as a wake-up call to investors who underestimated the industry. Today, the mechanical hard drive market is undergoing an unprecedented "structural transformation": it is no longer synonymous with cheapness but has become the most solid profit fortress for data centers and the AI wave.

"Oligopoly"

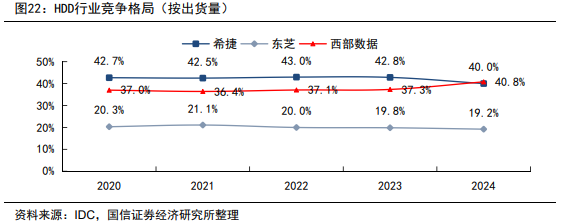

Currently, the mechanical hard drive market is in an "oligopoly" state. After decades of fierce price wars and mergers, the global HDD market is now dominated by only three major players: Seagate, Western Digital, and Toshiba. In terms of market share, Western Digital and Seagate have formed a duopoly, each holding approximately 40-41%, with Toshiba at around 19%.

This highly concentrated structure forms a natural and substantial "moat." For potential challengers, the capital expenditure and technological accumulation required to develop high-capacity mechanical hard drives are astronomical, and in today's stock-focused market, few new forces are willing (or able) to enter. This stable tripartite structure allows existing manufacturers to completely abandon the irrational competition of "selling at a loss for market share," and instead pursue higher-quality profit levels.

The shrinkage of the consumer market and the explosive growth of the data center market are reshaping manufacturers' product strategies. In the revenue structures of Western Digital and Seagate, the proportion of consumer HDDs has dropped sharply from over 20% to less than 10%. Limited production capacity is prioritized for more profitable enterprise customers, and consumer products have been effectively "marginalized." This structural change has shifted the market from "comprehensive coverage" to "precise focus."

"Supply remains tight" is not accidental but a strategic choice by manufacturers. In the past, hard drive makers increased production capacity to seize market share, resulting in price collapses; now, analysts point out, manufacturers are stopping the increase in unit capacity.

The Uptrend in Prices Against the Odds

This marks a shift in the HDD industry from "scale-driven" to "profit-driven." With production capacity locked in, while demand for massive storage by data centers and cloud computing platforms continues to surge amid the AI wave, the market balance quickly tilts toward the seller.

The price trend of mechanical hard drives saw a remarkable "counter-cyclical" rise in 2024-2025. In 2024, HDD shipments grew for the first time in a decade, with total sales soaring 50% compared to 2023, and the average selling price returning to the peak level of 1998. Entering the second half of 2025, Western Digital and Seagate both announced comprehensive price increases, with mainstream HDD prices rising an average of about 50% in four months, with some models seeing increases of up to 66%.

Although Seagate's production capacity for 2026-2027 has been fully sold out, Western Digital's CEO made it clear: "We don't want to build capacity with unknown purpose." This proactive supply limitation, combined with the shift of consumer capacity to the enterprise level, has created a tight supply-demand balance in the market, further driving up prices.

The Restructuring of Valuation Logic

The mechanical hard drive market is undergoing a profound "revaluation." Under an absolute oligopoly, the demand for AI cold data storage has shattered the belief that HDDs are a "sunset industry," pushing it from "volume growth, price drop" to "volume stability, price rise." The three giants' production control strategies and strategic abandonment of the consumer market mark the industry's entry into a new stage of "high gross margin and high precision" operations.

When Seagate's price target is set as high as $700 and Western Digital is favored at $495, the market is essentially paying for "high certainty." In the 2028 calendar year blueprint, the two giants' EPS are expected to reach $45 and $33, respectively.

So far this year, the stock prices of these two companies have more than doubled, and this is not a bubble but a repricing of HDD value by the market. In an era where data has become the "new oil," HDD giants, as the barrels carrying this oil, are enjoying their oligopoly dividends.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Fed: Flat curve, late-2026 cuts possible – BNY

BTW (Bitway) fluctuates by 56.4% in 24 hours: trading volume surge triggers intense price volatility

S&P 500: New highs despite global caution – Deutsche Bank