Behind Sandisk's rally: Is AI reshaping the storage DNA, or is it another epic cyclical illusion?

According to Zhitong Finance, based on the logic that "NAND has achieved 'de-cyclicality' through a $42 billion long-term contract with a major hyperscale cloud provider," SanDisk (SNDK.US) has delivered a return of over 356% since the beginning of the year. Analyst Louis Gerard notes that it remains to be seen whether this surge is a permanent leap in its business model or the most extreme cyclical peak in the history of the flash memory industry.

SanDisk will be spun off from Western Digital (WDC.US) in February 2025, a move that eliminates the "conglomerate discount" that previously masked the potential of the flash business behind the HDD business, making both of them pure plays in the AI supercycle.

The latest financial report shows that SanDisk's revenue for Q3 fiscal year 2026 reached $5.95 billion, up 252.1% year-on-year, with non-GAAP EPS at $23.41, far exceeding expectations. However, this was mainly driven by pricing power and product mix optimization, while bit shipments remained flat year-on-year and declined sequentially. The company has proactively exited the low-value consumer market, shifting toward the high-end data center business.

The most astonishing metric is the non-GAAP gross margin of 78.4%, far exceeding the industry average of 30%-40%, marking the steepest upswing in semiconductor history. However, this is entirely dependent on a 645% year-on-year surge in the data center business.

Limitations of the "New Business Model"

The "New Business Model" (NBM) implemented by SanDisk aims to eliminate cyclicality through financially backed long-term agreements. However, these agreements have a fundamental flaw: the long-term portion adopts floating pricing. This means that although the $11 billion financial guarantee prevents customer defaults, it cannot shield against price declines.

As new production capacity from Samsung and SK Hynix (such as 321-layer technology) comes online between 2026 and 2027, floating prices will reset in accordance with the spot market. The market currently views the $42 billion RPO as fixed income, which might be a misjudgment.

Significant Overvaluation

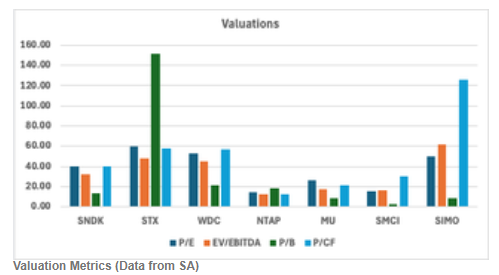

SanDisk's non-GAAP PE ratio has reached 40.36, much higher than Micron's 26.30. The discounted cash flow (DCF) model, factoring in price normalization post-2027, suggests an implied target price of only $372.42—about 70% downside from current prices. Probability-weighted scenario analysis likewise indicates the potential for negative returns. Compared to Micron, SanDisk's current valuation premium lacks fundamental support.

Risks and Conclusion

SanDisk's risk lies in the possibility that supply-demand imbalance may continue since suppliers are shifting to "profit-first" strategies and capacity is tilting toward HBM, restricting NAND supply; the $1.1 billion financial backing also enhances the enforceability of contracts.

Analyst Louis Gerard believes that SanDisk's share price soaring from $33 to $1,406 within a year is already absurd based on the AI narrative and supply tightness. Given that a 78% gross margin is unsustainable in a commoditized business and considering that this cycle set a record for margin expansion, future pullbacks could be similarly severe. He rates the company as "Sell."

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

AIAV (AIAvatar) fluctuated 40.3% in 24 hours: Low liquidity amplifies price volatility

USD: Softer tone as Fed seen delaying cuts – MUFG

Euro area: Energy shock rekindles price pressures – Societe Generale

Core Scientific shares slip after bitcoin miner swings to Q1 net loss despite higher revenue