The largest strike in Samsung's history is looming! JPMorgan estimates: At worst, it could eat up 12% of profits, adding new uncertainty to HBM competition

Samsung Electronics is facing one of the largest labor-management crises in its history.

According to a research report released by JP Morgan on May 6, the National Samsung Electronics Union (NSEU) has announced plans to stage an 18-day mass strike from May 21 to June 7. Their core demands include: abolishing the 50% cap on performance bonuses, securing a 7% base salary increase, and allocating 15% of annual operating profit into the employee bonus pool.

Negotiations are still ongoing, and the company’s management has clearly expressed a desire for an amicable solution. However, JP Morgan notes that the ultimate impact on profits will depend on the duration of the strike and the negotiation results. If all union demands are met, Samsung’s operating profit in 2026 may face a downside risk of 7% to 12%, and approximately 1% to 2% of the semiconductor division’s revenue could be adversely affected due to production halts.

This labor crisis is exacerbating the divergence in stock prices between Samsung and its competitor SK Hynix. SK Hynix successfully averted strike risks by reaching an agreement with its union on a 10% profit-sharing plan as early as September last year, while Samsung is now facing internal uncertainty on top of its ongoing disadvantages in the HBM competition. Since April, the performance gap between the two companies’ share prices has exceeded 25 percentage points.

Radical Strike Demands, Negotiations at a Stalemate

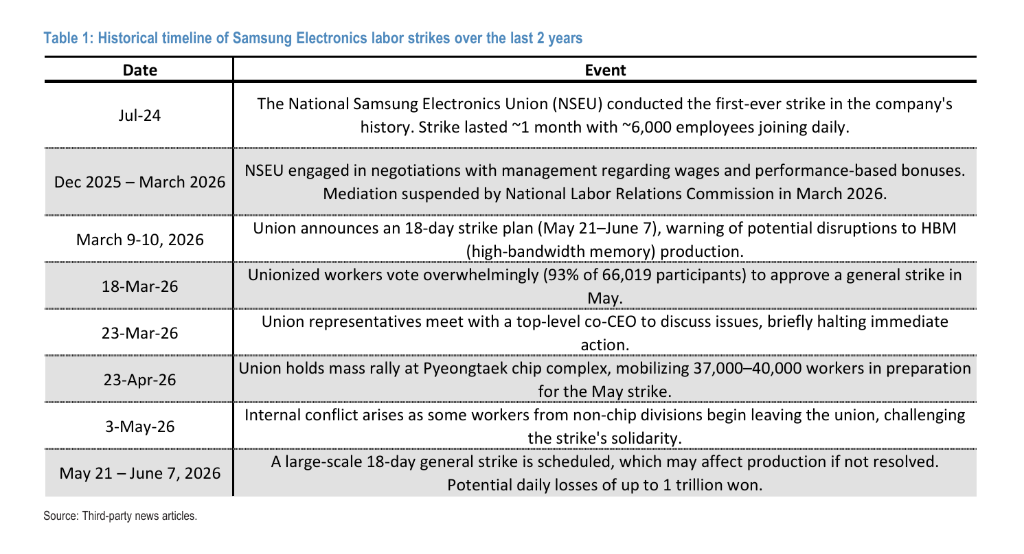

This strike is not a sudden occurrence but rather the result of intensifying labor-management tensions over the past two years.

In July 2024, Samsung experienced the first strike in its history, with about 6,000 employees participating daily for roughly a month. Afterward, the NSEU held multiple rounds of negotiations with management from December 2025 to March 2026, but irreconcilable differences remained, leading the National Labor Relations Commission to end mediation in March this year.

In March, the union announced the 18-day strike plan, warning that it could affect high-bandwidth memory (HBM) production lines. On March 18, 93% of 66,019 union members voted in favor of the strike. On April 23, after a meeting between union representatives and the co-CEO, the strike threat briefly eased; however, by the end of April, between 37,800 to 40,000 workers staged a large rally at the Pyeongtaek chip plant in preparation for the May strike. Meanwhile, some non-chip employees began leaving the union, signaling fractures in internal cohesion.

Samsung CFO Park Sooncheol stated in the recent earnings call that the company is handling the labor issue in accordance with the law and will prioritize dialogue to seek proper resolution. He added that even if a strike occurs, special teams and contingency mechanisms are in place to minimize production disruptions.

Profit Impact Estimates: Additional Labor Costs Could Reach KRW 39 Trillion

JP Morgan conducted a scenario analysis of the strike’s financial impact based on bottom-up estimates. If Samsung accepts the union’s terms, allocating 10-15% of operating profit to the performance bonus pool and raising base salaries by 5%, this would add 21 trillion to 39 trillion KRW in extra labor costs compared to current estimates, causing a 7% to 12% downside risk for 2026 operating profit.

Compared with Bloomberg market consensus, JP Morgan believes that under the 10% profit-sharing scenario, operating profit has about 3% downside potential. Based on its published forecast, the company’s operating profit for 2026 is around KRW 35 trillion; in the most pessimistic scenario, actual profit could be further compressed.

On the production impact side, JP Morgan cites wafer production loss data from the NSEU’s mock action in April, estimating that the 18-day strike could result in revenue opportunity losses exceeding KRW 4 trillion—about 1% of the semiconductor division’s annual sales. If production lines are forced to halt, the losses would be even more severe—annual DRAM output could fall 0.9%, NAND by 0.5%, and the system LSI and foundry divisions by 2.4%. Considering both increased labor costs and production losses, the full-year operating profit impact could total KRW 26 trillion to 43 trillion.

Citibank analyst Peter Lee’s team also cut Samsung’s target price (from KRW 320,000 to KRW 300,000) on April 30, noting that provisions for bonuses due to escalating labor disputes could erode profits, and lowered the company’s operating profit forecasts by 10% and 11% for this year and next, respectively.

The Key Conflict: Salary Structure Gap with SK Hynix

From a compensation structure perspective, the union’s demands have a practical background. According to JP Morgan, in the past two years, Samsung spent 11% of sales revenue on employee compensation (including base salary and incentives), while SK Hynix’s proportion reached 12.5%. On a per-capita basis, SK Hynix’s average total remuneration for 2025 is more than twice that of Samsung.

However, JP Morgan points out that this gap mainly arises from differences in workforce structure: Samsung has about 260,000 employees globally, with only 60% of its South Korean staff in the semiconductor division; SK Hynix has about 42,000 employees, all 100% engaged in semiconductor operations. The absolute pay gap per person between the two companies is largely structural rather than a simple reflection of compensation policies’ advantages or disadvantages.

In September last year, SK Hynix reached an agreement with its union on a 10% annual operating profit sharing scheme, setting an industry precedent. Bank of America Securities analyst Simon Woo wrote in a research note that a potential strike at Samsung could even further improve SK Hynix’s chip pricing environment, benefiting the latter.

Fundamentals Remain Strong, but Valuation Discount Persists

Samsung’s fundamentals themselves remain robust. Its semiconductor division achieved record profits in Q1 this year, with operating profit soaring 48-fold year-over-year thanks to AI data center orders, beating market expectations. JP Morgan also notes that the industry’s memory cycle continues upward, with memory shortages expected to intensify by 2027, leaving long-term fundamentals intact.

However, strong performance has not fully offset the valuation discount caused by labor-management risks. Stanley Tang, a senior fund manager at Sumitomo Mitsui DS Asset Management, stated, “The market remains optimistic about AI-driven high-bandwidth memory demand, but is concerned about a potential Samsung strike.” He pointed out that both MediaTek and ASE Technology Holding’s stock prices have risen nearly 10%, “but only Samsung is underperforming the broader market.”

Since May, Samsung’s share price has risen about 20%, higher than the 12% gain of the composite share price index over the same period, mainly benefiting from stronger-than-expected demand for CPU-related memory (driven by AMD’s Q1 results) and expectations around Apple’s foundry order collaborations. However, JP Morgan warns that negotiations are not yet complete, and production uncertainty and per-share earnings risks will continue to create short-term volatility for the stock price.

JP Morgan: Maintain Overweight, Watch for Short-Term Volatility Opportunities

Despite the above risks, JP Morgan maintains an Overweight rating on Samsung Electronics, with a target price of KRW 350,000 (December 2026), representing about 31% upside from the current price of KRW 268,000.

Analyst Jay Kwon commented that the core investment thesis of a “higher and longer” memory upcycle remains unchanged; every time the stock price has pulled back due to strike issues, it has been a buying opportunity, and this view is unchanged. JP Morgan believes that reaching an agreement between management and the union is highly likely, which will serve as a “catalyst” for the stock price to clear its overhang.

In the longer term, JP Morgan’s bullish stance is based on two pillars: first, the sustained expansion of hardware capex by cloud service providers through 2027 and the industry trend of AI memory demand expanding from GPUs to CPUs; second, Samsung’s continued improvement in technical execution in the HBM field. The firm believes that for Samsung’s valuation to become more compelling, further evidence of technological leadership is needed to rebuild investor confidence. The May 21 strike deadline will be a critical short-term observation point.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

AIAV (AIAvatar) fluctuated 40.3% in 24 hours: Low liquidity amplifies price volatility

USD: Softer tone as Fed seen delaying cuts – MUFG

Euro area: Energy shock rekindles price pressures – Societe Generale

Core Scientific shares slip after bitcoin miner swings to Q1 net loss despite higher revenue