Warning! Overheated US CPI Data May Pull Stock Market from 'Risk-On' Euphoria to Short-Term Sell-Off Track

According to The Knowledge, based on the latest forecasts from Wall Street strategists, an overheated U.S. CPI report could trigger a significant market shift—if CPI is much higher than expected, markets may transition from "the Federal Reserve will pause rate cuts this year" to "the Federal Reserve may have to reconsider rate hikes." This would break the dovish, optimistic, and bullish assumptions that support the market’s Risk-On (broad embrace of risk assets) stance, possibly sending global equities, bonds, and forex markets into a more intense repricing phase. In particular, for the AI computing power-driven global stock bull run, this might mean a major short-term downward correction.

Recently, the U.S. and global stock markets have repeatedly hit record highs thanks to robust U.S. nonfarm employment and an unprecedented boom in AI computing power investments. However, increasingly extreme momentum trading, oil price shocks, inflation concerns, and rising long-term U.S. Treasury yields have started to weigh on valuations; especially as the 10-year U.S. Treasury yield is forming a technical pattern that suggests additional upside. If yields continue to break higher, it could threaten equity market gains.

Moreover, the latest geopolitical developments—namely Trump’s rejection of an Iranian peace proposal—have undoubtedly prolonged the de facto U.S.-Iran dual blockade of the vital Strait of Hormuz for the global energy system. This could push up international oil prices further. With momentum indicators at historically extreme levels that have often preceded sharp short-term sell-offs, these may jointly send the AI-investment-fueled global stock rally into correction.

U.S. inflation is heating up again, mainly due to international oil prices surging more than 60% since the end of February. Major central banks, including the Federal Reserve, are approaching a point where action may be needed. At least for now, the interest rate futures market sees the Fed staying put, and not signaling any rate cuts at least until the end of this year. Meanwhile, the ECB, Bank of Japan, and Bank of England are likely to resume tightening policies in the near future.

This is not just about central bank policy. The AI computing power boom driving global stocks, U.S. Treasury yields—the so-called "anchor of global asset pricing,"—and the dollar index all face major implications, and this week’s April U.S. CPI report will play an extremely important role in determining their next moves.

CPI Storm Approaches! High Oil Prices Could Ignite an Inflation Monster

April CPI is expected to remain hot, with economists projecting a month-on-month spike of 0.6%, compared to March’s 0.9% increase. This is set to push the annual CPI from last month’s 3.3% sharply up to 3.7%. Meanwhile, core CPI is also forecast to jump, with a possible month-on-month increase from 0.2% to 0.4%, and year-on-year core CPI rising from 2.6% to 2.7%.

Prediction markets like Kalshi agree with analysts’ forecasts, expecting headline CPI year-on-year to jump 3.7% and month-on-month 0.6%, with core CPI up 2.7% year-on-year and 0.4% month-on-month. The issue is, May’s inflation is also likely to rise further on April’s strong base; at present, the CPI swap market is pricing headline CPI as high as 4%.

It’s noteworthy that March’s U.S. inflation already looked hot, with the monthly CPI surging 0.9%, the biggest single-month rise since June 2022, and the annual rate rising to 3.3%, the highest since 2024 began. Gasoline prices recorded the strongest single-month jump since 1967.

This (constantly rising CPI data) will undoubtedly pose major challenges to the Federal Reserve and global central banks, and, after 2021 and 2022’s inflation misjudgments, increase pressures for rate hikes and monetary tightening actions. Markets have already reacted—Fed funds futures now indicate no rate cuts by the Fed through 2026, and none foreseeable soon.

These challenges aren’t limited to the Fed—they also confront other major central banks like the ECB and Bank of England, as high inflation threatens to force quick adaptation in both the interest rate futures and bond markets to the oil supply shock.

Since the Iran war began in late February, the Strait of Hormuz has largely been blockaded, cutting off one of the main shipping routes for crude, natural gas, and refined fuel to world markets, sharply driving up energy prices and stoking global investor fears about inflation. The International Energy Agency says that the Hormuz supply disruption caused by this geopolitical conflict is creating the largest supply shock in human history.

Wall Street giant Citi released a report stating that if long-term U.S.-Iran peace talks remain elusive, keeping the Strait of Hormuz under extended lock and control, international oil benchmark Brent crude could surge further from its recent retreat near $100, potentially setting new highs for this cycle.

Markets are already pricing the possibility of European rate hikes: the ECB and Bank of England could hike as many as three times this year. Meanwhile, so far, markets have not priced in Fed rate hikes—only an end to the easing cycle.

Even as CPI accelerates, the bond market is digesting this relatively calmly, pricing risk through higher expected inflation rather than higher real yields—suggesting the market still expects the Fed to remain dovish, as some economists hold that the Fed will regard oil shocks as “transitory.”

Since the international oil price surge of over 60% at the end of February, the real yield curve for the 10-year U.S. TIPS has actually decreased in the past few months, while 5-year inflation swaps have soared.

This makes the April CPI report especially important— a lower-than-expected print could bring rate cuts back into market expectations, while a reading well above consensus may force markets to price in hikes, challenging the dovish, bullish Fed stance.

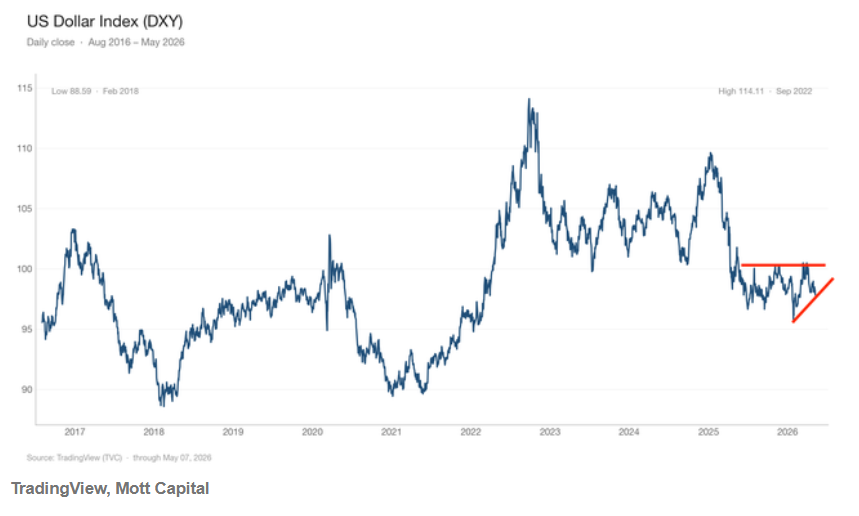

Additionally, CPI may have a significant and lasting impact on the U.S. dollar trend and U.S. Treasury yields. The 10-year Treasury yield is close to breaking a multi-year descending trendline, a critical technical level repeatedly tested in the past. If the 10-year breaks and holds above 4.4%, we could see the yield surge for months, possibly returning to the historic high levels seen in October 2023.

The same goes for the dollar index, the principal gauge of U.S. dollar strength. The dollar index has struggled to break above 101—a key resistance—but it’s trended higher in recent weeks; if it breaks 101, the dollar could reach its highest level since January 2025, near 109.

The bond market is still pricing oil shocks as “higher inflation expectations, lower real yields,” meaning it believes the Fed sees the oil shock as transitory; but if CPI keeps beating forecasts, this dovish assumption will be challenged. If the 10-year Treasury yield breaks through 4.4%, multi-month yield increases may follow; if the dollar index breaks 101, it could surge towards the 109 area seen in January 2025.

Currently, both rates and the dollar stand at critical technical junctures. If both the dollar and the 10-year yield surge after the CPI report, this could be a major "red flag" sell signal that neither the Fed nor investors can ignore.

If the 10-year yield and dollar continue to range trade, markets will likely stay neutral for some time, at least until the next CPI report in June. In the meantime, a flood of AI-linked positive catalysts could drive another round of historic bullish euphoria for U.S. and global stocks.

CPI as the “General Switch” for Three Key Markets! A Red-Hot CPI Could Drag Markets Back from “Risk-On” to the Era of “High Yields, High Dollar, High Volatility”

An excessively hot U.S. CPI inflation report may force markets to reassess the Fed’s reaction function. If CPI is significantly higher than expected, markets could shift from “no rate cuts for now” towards “repricing rate hike risk,” driving the 10-year Treasury yield and dollar above key technical levels and triggering a sharp, short-term selloff in stocks and other global risk assets, reversing Risk-On sentiment.

For the bond market, a hot CPI means: rising long-term nominal yields, higher inflation compensation, and a sustained upward break in the 10-year Treasury curve. If markets believe the Fed will “look through” oil shocks, real yields may not rise sharply; but if CPI heat spreads to core inflation, wages, and services, the bond market will be forced to refocus from “one-off oil shock” to “more persistent inflation shock.” At that point, real yields will also rise, and the 10-year may retest higher ranges.

Recently, Wall Street giant Barclays has pushed out its expectation for Fed rate cuts from 2026 to 2027. Interest rate futures traders have assigned about a 78.7% chance of steady rates through the end of 2026, meaning the bond market has largely abandoned the “rate cut dream.”

If 10-year or longer U.S. Treasury yields rise persistently, that means “significantly higher funding costs + weaker liquidity expectations + a larger macro denominator” all at once for core risk assets like stocks, cryptocurrencies, and high-yield corporate bonds.

Theoretically, the 10-year U.S. Treasury yield is the “risk-free rate” (r) in the denominator of the key DCF valuation model for stocks. If other variables (especially cash flow expectations in the numerator) don’t change much—like during an earnings season void of strong catalysts—then a higher or persistently high denominator level puts immense pressure on the valuations of high-flying, AI-linked tech stocks, high-yield bonds, and cryptocurrencies, all of which may face valuation collapse at historical highs.

For the forex market, a hot CPI is extremely bullish for the dollar, especially as U.S. yields rise again and growth elsewhere remains fragile. The logic: if U.S. inflation heats up but the economy remains resilient, the Fed keeps rates high or turns more hawkish, widening the dollar's relative yield advantage; at the same time, geopolitical strife and oil shocks boost dollar safe-haven demand. A dollar index break above 101 could open technical space towards 109—consistent with recent pressure on energy-importing economies (like Japan and South Korea), where rising oil hurts and central banks face greater currency risks.

For stocks, a hot CPI isn’t just universally bearish—it will change market internals. If CPI runs hot, overall U.S. market valuations will get squeezed by higher discount rates, particularly long-duration, unprofitable growth stocks, popular AI momentum trades, and the most crowded corners of semiconductors; but energy, oil services, inflation hedges, and value stocks with strong cash flows and pricing power will relatively outperform. If CPI is driven by energy but core inflation stays moderate and underwhelming, the market may keep betting that the “AI infrastructure frenzy + economic resilience” narrative offsets any pressure, so the AI-driven global bull trend stays intact for now. But if core CPI clearly heats up too, stocks may shift from a “profit-driven bull” into a more complex pricing regime of “high yield curves hurting valuations + inflation squeezing profit margins.”

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Defaults Surge, Deep Losses! Apollo Plans to Sell $3 Billion Private Credit Fund

US Dollar Index advances after Trump and Iran dismissed latest peace initiatives