Guinea's Bauxite Restrictions Incoming? Aluminum Prices May Enter a Supercycle

The global aluminum market may be facing a new round of supply shocks. On May 25, Guinea’s Minister of Mines stated clearly that an official bauxite export control plan will be announced in June. This is the fourth time in three months that Guinea has sent signals of export restrictions. Previous announcements have repeatedly disrupted the market but failed to fuel any sustained price rally due to a lack of implementation details. This time, however, a concrete timeline has been set, along with quantifiable reduction targets: annual export volume will be slashed from the record 183 million tons in 2025 down to around 150 million tons. The policy is likely to move from verbal expectation to actual implementation.

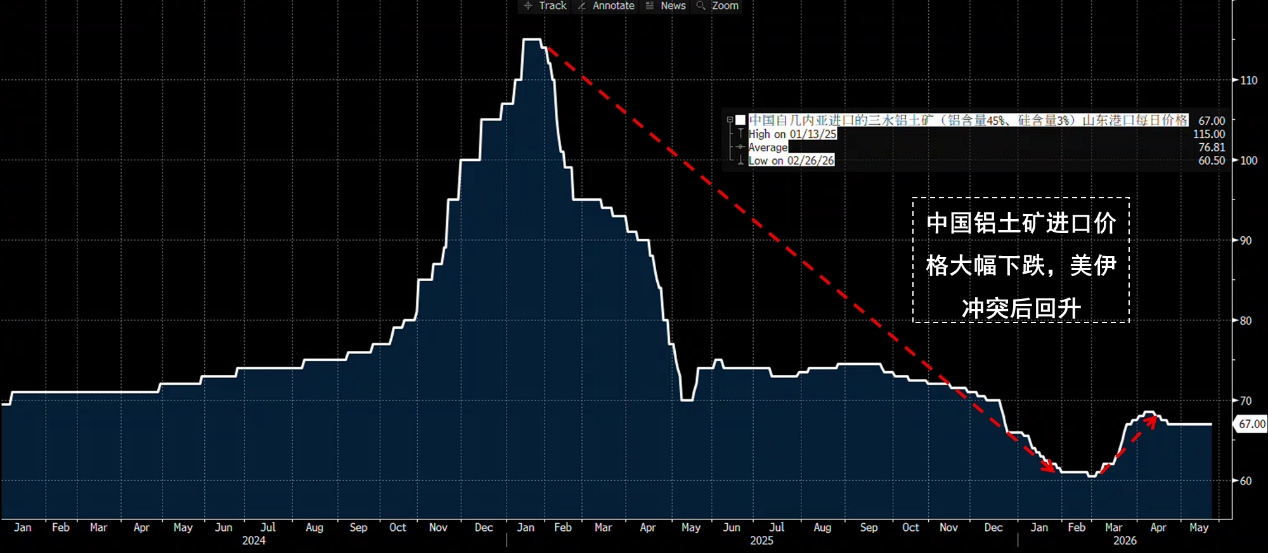

As the world’s largest bauxite exporter, Guinea accounts for more than one-third of global bauxite supply, with over 70% of its exports going to China. In 2025, Guinea’s bauxite exports soared 25% year-on-year to 183 million tons, a historical high. However, this rapid ramp-up in supply pushed bauxite prices down sharply, plummeting from $70/ton just over a year ago to $32-38/ton, bringing smaller miners to the brink of bankruptcy and slashing government revenues.

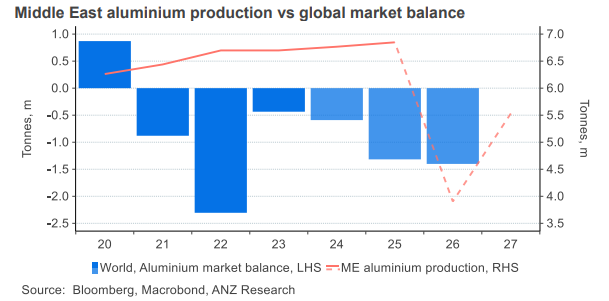

Since the onset of the Middle East conflict, the blockade of the Strait of Hormuz, along with attacks on core smelters such as Emirates Global Aluminium (EGA) and Aluminium Bahrain (ALBA), have resulted in the loss of over 3 million tons of annualized smelting capacity. The Middle East accounts for 23% of the world’s primary aluminum production (excluding China), and recovery is expected to take at least 12 months.

Adding to this, China’s aluminum production capacity has reached the regulatory ceiling of 45 million tons, with actual annualized output now at 47.6 million tons. Under domestic anti-overcapacity policies, there is unlikely to be a clear relaxation of capacity constraints over the next two years. It is expected that the global aluminum supply will enter a period of distinct structural shortage. At present, LME aluminum prices continue to trend higher, approaching a four-year high of $3,717/ton.

Resource Nationalism Spreads, Structural Repricing in the Aluminum Market

As noted above, the surge in Guinea’s bauxite shipments previously cut prices in half, forcing small- and medium-sized miners close to their cost lines and causing a sharp drop in government fiscal revenues. Limiting exports, regaining pricing power, and boosting revenue have become Guinea’s key policy objectives. If implemented, aluminum prices are expected to keep rising under constraints of resource supply, geopolitical tensions, and demand for energy transition.

On the supply side, in recent years, resource nationalism has been visibly heating up around the world.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Is Bitcoin price Going Down? (May 27)

Among the 14 Trillion-Dollar Companies, AI Accounts for 90%

Copper–gold “2020 signal” is really about global liquidity, not just Bitcoin

AustralianSuper says possible Glencore listing on ASX would be positive