Morgan Stanley Comments on Nvidia "Halving Storage" Rumor: This Is a Real Shortage, Supply Constraints Have Become the Biggest Obstacle to AI

Rumors of Nvidia cutting the Vera Rubin rack memory configuration sent shockwaves through the market, but Morgan Stanley believes this actually confirms the severity of the memory shortage, rather than signaling a cooling of AI demand.

Last week, research institution SemiAnalysis released a report stating that Nvidia plans to reduce the LPDDR5 memory capacity of Vera Rubin racks from 55 TB to 28 TB, and the SOCAMM memory module specification from 192 GB to 96 GB. The market interpreted this as weakening AI demand, causing Micron Technology (MU) stock to plunge 13% on the same day it received Nvidia's HBM4 certification, marking the largest intraday decline since April 2025. Morgan Stanley semiconductor analyst Joseph Moore promptly issued a research note to refute this interpretation.

According to the Chasing Wind Trading Desk, Morgan Stanley stated clearly in its latest report that it has verified some racks will ship with lower configurations, but emphasized that this adjustment is entirely due to supply-side constraints, not weak demand. At the same time, the firm raised its 2026 global semiconductor industry revenue forecast from $807 billion to $880 billion and maintained its Overweight rating on MU and SNDK, with target prices of $1,050 and $1,750, respectively.

Rumor Confirmed, But Market Misinterprets the Logic

Morgan Stanley's report confirms that Nvidia is indeed reducing Vera Rubin rack memory configurations, but stresses that the market has completely misread the implications.

The report noted that Nvidia and cloud computing customers are willing to purchase every available GB of SOCAMM memory, and as soon as supply catches up, higher configurations will be immediately restored. Morgan Stanley believes the sole purpose of this adjustment is to minimize the impact of the DRAM shortage on GPU rack sales, and this is concrete evidence of a real shortage rather than the result of repeated order window effects.

In terms of scale, assuming 53,000 to 70,000 racks are built next year, a 55 TB configuration would make rack SOCAMM demand close to 5% of global DRAM demand. If configurations are halved across the board, the most extreme scenario would see a reduction of about 1.4 million TB in demand, equivalent to more than 2% of a 6.2 million TB market size, and this would impact the higher-value market segment. Morgan Stanley expects that higher configurations will resume soon after shipments begin.

April SIA Data: No Quick Fix for Memory Shortage

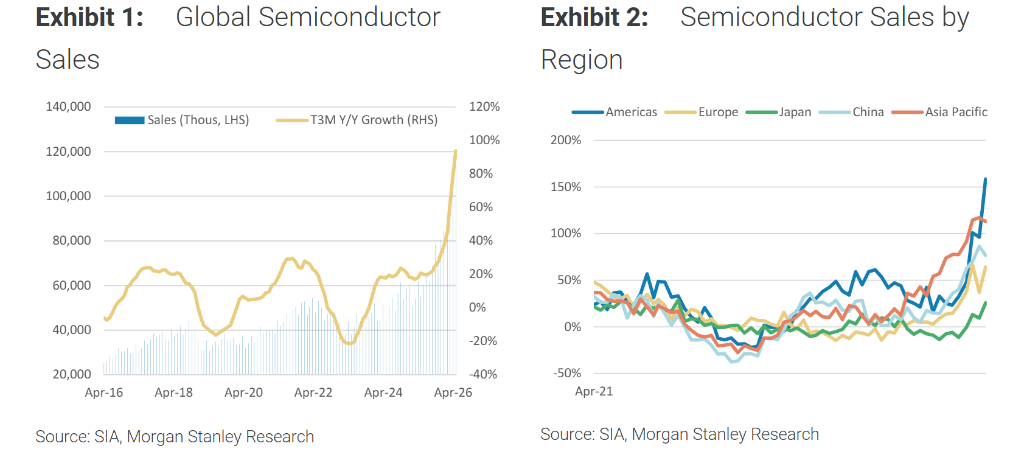

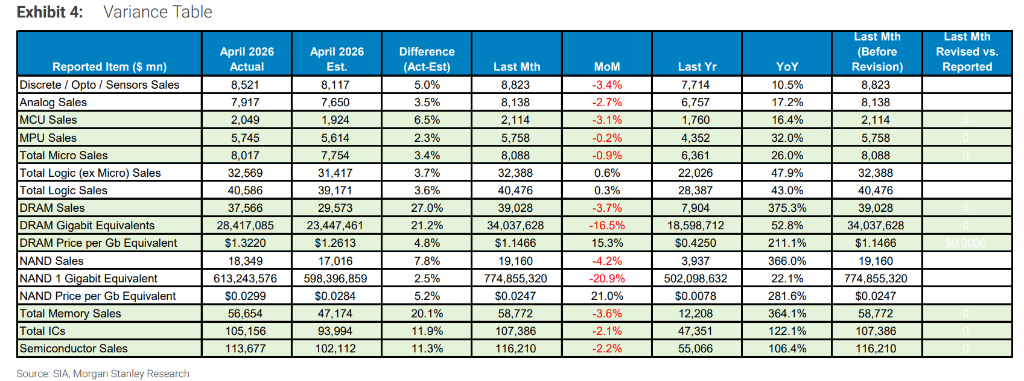

Morgan Stanley also commented on the Semiconductor Industry Association (SIA) April billing data released on June 5, stating this further strengthens the assessment that memory supply will remain tight.

In April, total semiconductor sales fell 2.2% month-on-month, much better than Morgan Stanley’s estimate of -12.1% and the 10-year seasonal average of -10.6%, with year-on-year growth accelerating to 106.4%. Memory performed especially well: DRAM sales fell only 3.7% month-on-month, far better than the estimated -24.2% and the 5-year average of -27.6%, with an annual increase of 375.3% and three-month rolling annual growth at 298.5%—a historical high since 2001. The average price has accelerated for nine consecutive quarters year-on-year; NAND sales fell 4.2% month-on-month, also much better than the -11.2% estimate, with an annual increase of 366.0%. The three-month rolling year-on-year revenue growth of 307.0% and average price growth of 213.4% are both record highs.

Morgan Stanley points out that the April data confirms there is no quick fix for the memory shortage. DRAM has become the main bottleneck in AI infrastructure construction; intensive HBM wafer capacity, cleanroom and EUV equipment constraints, and limited incremental NAND production capacity all support a “higher for longer” pricing environment. The firm believes long-term supply agreements (LTAs) are a symptom of supply tightness and the hyperscale cloud vendors’ competition for capacity, rather than the cause of this cycle.

Raised Forecasts, Bullish on Memory and AI Supply Chain

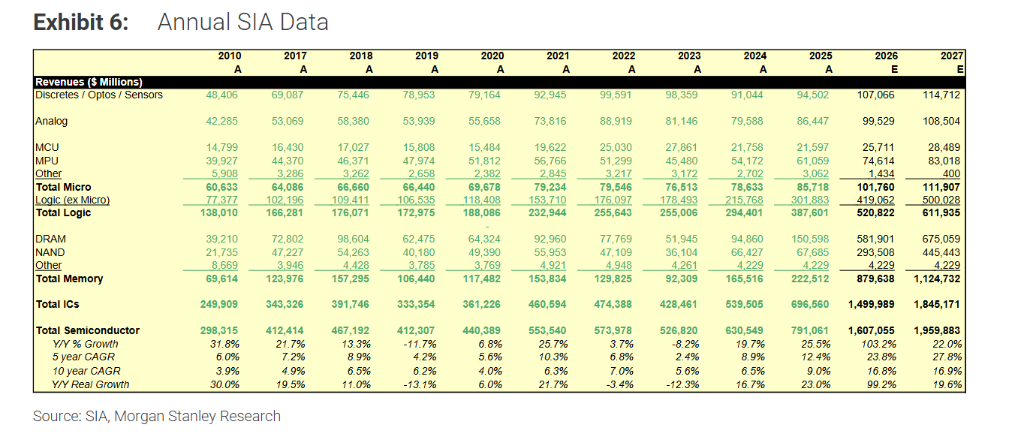

Based on these findings, Morgan Stanley has sharply raised its industry forecasts. The global semiconductor revenue estimate for 2026 has been raised from $910 billion to $1.607 trillion, with expected year-on-year growth from +91% to +103%, mostly driven by memory. DRAM estimates have jumped from $150.3 billion to $581.9 billion, and NAND from $67.7 billion to $293.5 billion. For 2027, the firm expects industry revenue to further grow 22% to $1.96 trillion, mainly driven by continued memory pricing power.

At the individual stock level, Morgan Stanley maintains an Overweight rating on MU with a base target price of $1,050 (current price $864, implying 22% upside); maintains Overweight on SNDK with a base target price of $1,750 (current price $1,559, implying 12% upside). In addition, the firm remains bullish on AI infrastructure beneficiaries NVDA (Overweight, target price $288), AVGO (Overweight, target price $502), and ALAB (Overweight, target price $240), as well as capital equipment/supply chain stocks LRCX, KLAC, and MKSI.

Broad Market Improves as Cycle Signals Widen

Morgan Stanley notes that April SIA data highlights more than just memory; broader market outperformance is also noteworthy, indicating that the current semiconductor upcycle is spreading from AI-driven strength to a broader range of sectors.

By category, discrete devices, analog chips, MCUs, and MPUs all exceeded Morgan Stanley’s estimates and the 10-year seasonal averages. The industrial segment is rebounding from the cycle trough and demand is expanding into non-AI areas, with continued progress in inventory drawdowns. The firm notes that while price increases are appearing in the supply chain, the main driver is cost pass-through rather than value re-capture, except in a few companies like ADI.

Morgan Stanley concludes that the April data further demonstrates that the current semiconductor upcycle is no longer simply an AI-focused rally, but is evolving into a broader supply-constrained upcycle. Against this backdrop, the firm also remains positive on analog/MCU suppliers ADI, NXP, and ALGM.

~~~~~~~~~~~~~~~~~~~~~~~~

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Charles Hoskinson Tests Zero-Knowledge Wallet Recovery for Cardano

Bitcoin Sell-Off Risk Grows as Key On-Chain Metric Turns Negative, Analyst Warns

Dark Defender Says “I Am Adding More XRP to My Bag”. Here’s why

Bitget Launches Third Anti-Scam Month With Multi-Asset Fraud Report