Bitget UEX Daily | Warsh's Dovish Debut Turns Hawkish, Half of Officials Expect Rate Hikes; US-Iran Signs Memorandum Easing Geopolitical Risks; Major US Indices Pull Back, Tech Stocks Under Pressure

Bitget2026/06/18 01:16

Bitget2026/06/18 01:16

I. Hotspot News

Federal Reserve Dynamics The Federal Reserve kept the target range for the federal funds rate unchanged at 3.5%-3.75%. However, the dot plot revealed increased divergence, with 9 officials expecting rate hikes by the end of 2026 and the median projection raised to 3.75%. Chair Warsh emphasized that inflation remains well above the 2% target and announced the formation of five special working groups on monetary policy. The new statement was streamlined, focusing on achieving price stability. Market expectations for rate hikes by year-end have risen significantly. This move reinforces dollar support but may heighten volatility in equities and risk assets.

International Commodities The US and Iran formally signed a memorandum of understanding, committing to cease military actions, lift sanctions, and reopen the Strait of Hormuz. The 14-clause agreement covers reconstruction funding, nuclear issues, and related matters. The deal eases concerns over energy supply disruptions, putting short-term pressure on oil prices while providing support for safe-haven assets like gold. It highlights the direct transmission effect of geopolitical de-escalation on commodity markets.

Macroeconomic Policy President Trump stated that the Fed holding rates steady is “also OK” and hinted at the possibility of hikes. The Fed’s projections show higher core inflation and slightly lower GDP growth, reflecting supply shocks. Policy signals have turned cautious. Combined with Middle East easing, this supports short-term risk appetite recovery, but uncertainty in the inflation path will continue to dominate future market expectations.

II. Market Review

Commodities & Forex Performance (Real-Time Update)

- Spot Gold: Approximately $4,300/oz, +1.25% in 24h.

- Spot Silver: Approximately $69/oz, +1.9% in 24h.

- WTI Crude: Approximately $75/barrel, -1.13% in 24h.

- Brent Crude: Approximately $79/barrel, -1.0% in 24h.

- US Dollar Index (DXY): Approximately 100.332, -0.05% in 24h.

Driver Analysis: The US-Iran memorandum significantly reduced risks of Strait of Hormuz disruption, driving oil prices lower, while the Fed’s hawkish pivot supported the dollar. Gold oscillated narrowly between safe-haven demand and a stronger dollar, while silver rebounded mildly on industrial demand expectations. Overall, geopolitical easing combined with higher-for-longer rate expectations is capping upside for commodities in the near term. A stronger dollar may continue to pressure emerging markets and commodities. Watch the implementation of sanction relief for its actual impact on supply-demand balance.

Cryptocurrency Performance

- BTC: Approximately $64,600, -1.85% in 24h.

- ETH: Approximately $1,750, -2.34% in 24h.

- Total Crypto Market Cap: Approximately $2.31 trillion, -1.4% in 24h.

- Market Liquidations: 24h total ~$440 million, with long liquidations ~$310 million.

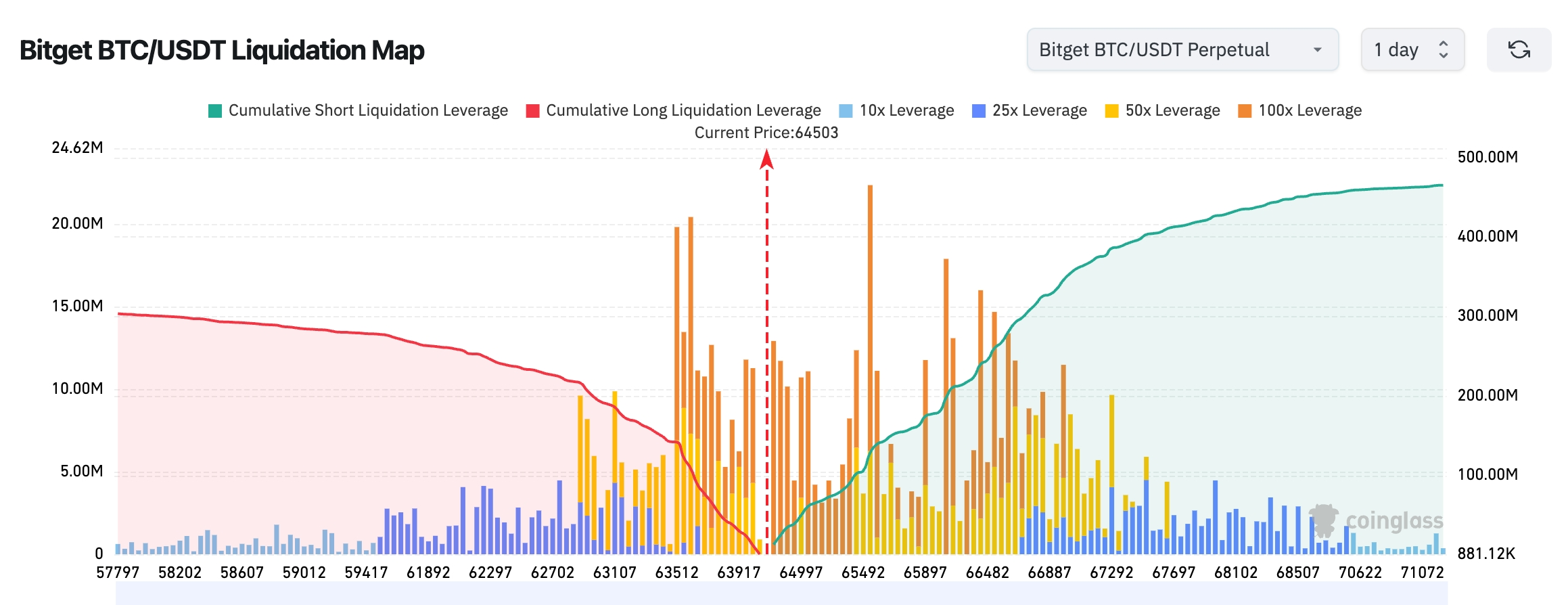

- Bitget BTC/USDT Liquidation Heatmap: Current price around 64,503 USDT, near the lower edge of major liquidation clusters. Above, the $65,500–$66,900 zone holds significant 50x and 100x short positions, with cumulative short liquidation size far exceeding longs below. Short-term upside to sweep short liquidity is possible. Below, the $63,500–$64,000 zone has long liquidations but on a smaller scale. The map suggests the market is more inclined to test the $65,500–$66,500 short liquidity zone first.

- Spot ETF Net Flows: BTC spot ETFs recorded a net inflow of $10.2 million as of yesterday’s close.

Driver Analysis: The Fed’s hawkish signals and Warsh’s communication shift triggered deleveraging, while the US-Iran deal eased risk sentiment. BTC and ETH declined in tandem, but the total market cap held key levels. ETF flows remained relatively stable, with liquidations dominated by longs. Technically, BTC is testing critical support. Macro uncertainty and geopolitical easing create a counterbalance, leading to short-term range-bound trading. Focus on institutional adaptation to the higher-rate environment and capital rotation.

US Stock Indices Performance

- Dow Jones: Closed around 52,000 points (-0.6%).

- S&P 500: Closed around 7,511 points (-0.57%).

- Nasdaq: Closed around 26,376 points (-1.15%).

Tech Giants Performance

- NVDA: ~$206.11, -0.02%.

- AAPL: ~$296.36, -0.96%.

- MSFT: ~$379, -1.5%.

- GOOGL: ~$365.94, -1.96%.

- AMZN: ~$239.85, -2.50%.

- META: ~$580, -1.2%.

- TSLA: ~$401.35, -0.82%.

Performance Summary & Driver Analysis: US indices diverged, with the Dow benefiting from defensive characteristics to hit records, while the Nasdaq was dragged by tech weakness. Among the Magnificent Seven, some AI-related names faced valuation pressure from Fed signals, while Tesla showed relative resilience on event-driven factors. Overall, the sector remains cautious amid hawkish policy and geopolitical easing. The long-term AI narrative retains resilience, but short-term leverage and rate sensitivity have amplified individual stock differentiation.

Crypto Stock Contracts Overview

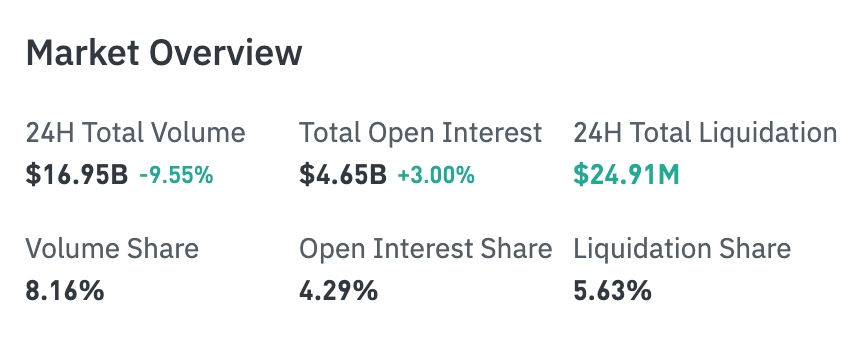

- 24H Trading Volume: $16.942 billion (-9.60%)

- Total Open Interest: $4.651 billion (+3.00%)

- 24H Liquidation Amount: $24.9123 million

- Volume Share: 8.15%

- OI Share: 4.29%

- Liquidation Share: 5.63%

Sector Performance

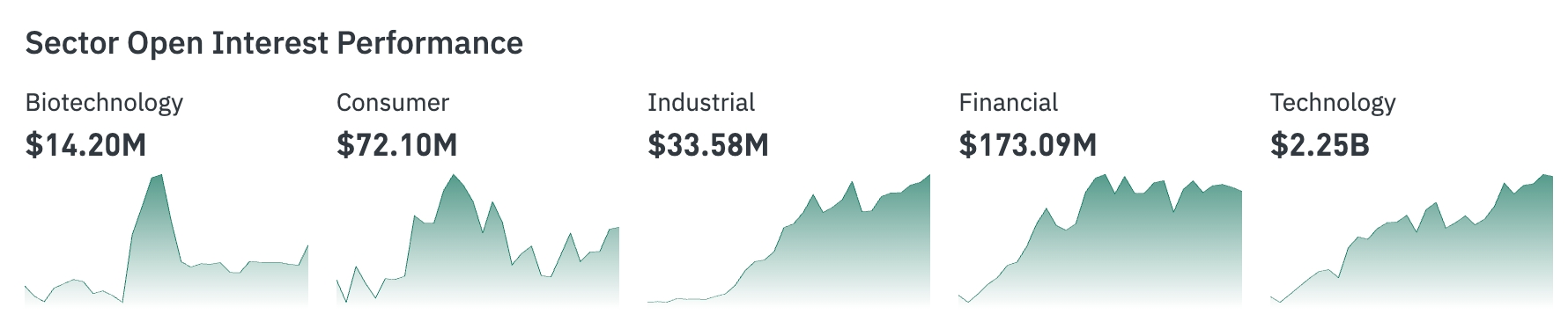

- Tech sector highest OI: $2.246 billion

- Financials: $173 million

- Biotechnology: $14.2055 million

- Consumer: $72.1029 million

- Industrials: $33.6049 million

OI Heatmap

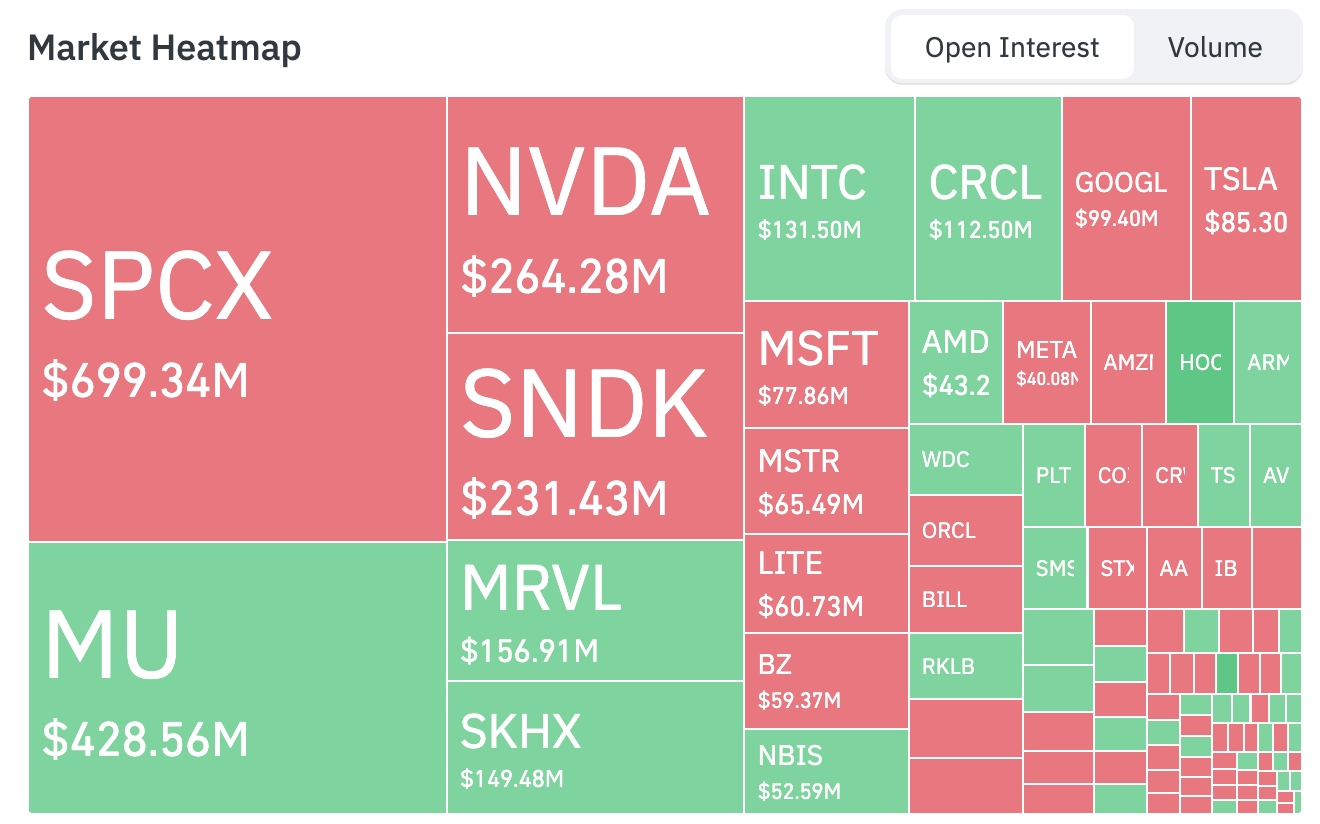

- SPCX: $699 million

- MU: $428 million

- NVDA: $264 million

- SNDK: $231 million

- MRVL: $157 million

Sector Movers Observation Semiconductor/Chip Sector — Mixed performance with notable sub-sector divergence.

- Gainers: ARM surged over 5%, Western Digital (WDC), Applied Materials (AMAT), and Broadcom (AVGO) rose over 4%.

- Losers: Sandisk-related names, NXP Semiconductors (NXPI), and NVIDIA (NVDA) fell over 1%. Drivers: Chair Warsh’s hawkish debut, raised rate projections, and streamlined statement made markets more cautious on long-term growth and capital costs, pressuring high-valuation AI/chip growth stocks. However, ARM demonstrated resilience in edge computing and agentic AI trends; Broadcom benefited from diversified applications and enterprise orders. Memory/storage names were weighed by cost pass-through and cyclical concerns. Intel’s 18A-P process entering risk production provided some supply-chain support, but the sector as a whole remains influenced by macro rate paths and is likely to retain high-beta characteristics in the near term.

Aerospace/Emerging Tech Sector

- SpaceX fell ~4.95% in its first trading day post-listing. Drivers: As a high-valuation new listing, it faced profit-taking pressure amid the Fed’s hawkish turn and rising cost-of-capital expectations. Despite strong long-term monopoly advantages in Starlink and launch services, initial post-IPO volatility was amplified by a temporary pullback in market risk appetite.

III. In-Depth US Stock Analysis

1. ASML - Supply Warning for Terafab Project Event Overview: ASML’s CEO noted the need to avoid supply bottlenecks when serving Musk’s Terafab and similar new projects. It represents a major wafer fab opportunity but requires careful management. Market Interpretation: Institutions focus on the company’s leadership in equipment for AI infrastructure expansion, with supply management capability being key. Investment Insight: Long-term beneficiary of the semiconductor cycle, but monitor supply chain execution. Short-term volatility may offer entry points.

2. Apple (AAPL) - iPhone Air Upgrade and Pricing Strategy Event Overview: Apple is advancing the second-generation iPhone Air (launching spring 2027) with added rear ultra-wide camera and improved battery life, powered by a custom A20 Pro chip. CEO Cook confirmed product price increases due to surging memory and storage chip costs. Market Interpretation: Analysts view it as a move to enhance product appeal; cost pass-through reflects supply chain pressures. Investment Insight: Watch innovation cycles and pricing power; the services ecosystem provides a buffer.

3. Intel (INTC) - Process Progress and AI CPU Outlook Event Overview: 18A-P process entered risk production with improved performance/power efficiency. Bernstein raised price targets, highlighting that agentic AI will significantly boost CPU demand. Market Interpretation: Institutions are optimistic about the CPU/GPU configuration rebalancing in the AI 2.0 era. Investment Insight: Process breakthroughs could reshape competitiveness; monitor foundry client migration.

4. Amazon (AMZN) - Quantum Computing Prospects Event Overview: Executives predict the first commercially practical quantum computer will emerge in 5-7 years, with development trajectories similar to semiconductors. Market Interpretation: Long-term technology positioning is well-recognized, strengthening cloud/AI competitiveness. Investment Insight: Quantum investments have long cycles; focus on milestone progress.

IV. Market Dynamics

- Strategy’s preferred stock STRC closed at $89 on Wednesday, down 11% from its $100 par value, hitting an intraday low of $88.50 for its lowest close since listing. STRC currently offers an effective dividend yield of 12.9% and aims to maintain stability around $100 through monthly rate adjustments. The plan to issue new shares to buy Bitcoin when trading above par has been paused while trading at a discount.

- Goldman Sachs Asset Management analyst Kay Haigh noted that today’s rate decision confirms the Fed’s recent hawkish shift is not solely tied to energy price increases. Despite recent oil declines, half of FOMC members expect hikes as early as this year, reflecting a strong labor market and inflation data. The base case remains that the Fed can narrowly avoid hikes, but the path is narrow and future inflation data will carry heavy weight.

- “Fed Whisperer” Nick Timiraos on the rate decision: The dot plot showed a clear hawkish tilt. Of 18 officials, 9 expect at least one hike this year, with 6 anticipating multiple hikes.

- The Bhutan government address transferred 533.2 BTC ($34.52 million) to a CEX. Over the past year since June last year, the address appears to have sold approximately 10,451 BTC for $979 million at an average price of $93,738.

- Research firm K33 noted in its report that Bitcoin rebounded after two weeks of double-digit declines. Long-term holders’ holdings hit a record high, potentially signaling the end of the bear market. Research head Vetle Lunde said reduced old-coin transaction activity indicates lower selling willingness among long-term holders, with patient participants steadily absorbing supply — further evidence that the bear market may be ending. Supporting this, 79% of Bitcoin’s circulating supply is now held by long-term holders, a record high, reflecting ongoing accumulation and a gradually more positive market environment.

V. Today’s Market Calendar

June 18 (Thursday)

- US Economic Data: Initial jobless claims for week of June 13, Philadelphia Fed Manufacturing Index, etc.

- Earnings: Accenture (ACN), Kroger (KR), etc. (focus on consumer and tech services sectors). ★★★★

June 19 (Friday)

- US markets closed for Juneteenth federal holiday.

Key Themes This Week: “Fed Focus Week” — Kevin Warsh’s first FOMC meeting + retail sales and other data + Accenture/Kroger earnings will dominate macro policy expectations and sentiment. SpaceX (SPCX) first full trading week post-IPO (impact on space/tech-related concepts).

Institutional Views: Prominent investment bank analysts believe Chair Warsh’s hawkish tone in his debut, combined with the upwardly revised dot plot, has heightened short-term rate uncertainty. However, the US-Iran memorandum has significantly eased energy risks, providing a buffer for markets. Dollar strength and falling oil prices create positive linkages, favoring defensive US stock sectors while growth/tech faces valuation pressure. Crypto markets face near-term pressure but retain solid ETF foundations. Long-term, a soft-landing macro scenario supports risk asset recovery. Overall, maintain a neutral-to-cautiously-optimistic stance and monitor data validation along with geopolitical implementation progress.

Disclaimer: The above content is compiled by AI search and manually verified for release. It does not constitute any investment advice. Data in the text may inevitably contain deviations; please refer to real-time market data.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Charles Hoskinson Tests Zero-Knowledge Wallet Recovery for Cardano

Bitcoin Sell-Off Risk Grows as Key On-Chain Metric Turns Negative, Analyst Warns

Dark Defender Says “I Am Adding More XRP to My Bag”. Here’s why

Bitget Launches Third Anti-Scam Month With Multi-Asset Fraud Report