SemiAnalysis: Half of US Data Centers to Shut Down by 2026? This is a False Alarm “Coded by AI”

A pessimistic narrative of slowed data center construction in the United States is sweeping the market, yet the data behind bearish sentiment is causing rational investors to reassess this collective misjudgment.

On June 18, independent industry research organization SemiAnalysis published an article directly countering the extreme claim widely circulated in the market that "U.S. data center construction is slowing dramatically, and half of the 2026 capacity will be canceled or delayed." The report argues that this wave of panic stems from information misreading and sample bias, as the actual U.S. data center delivery capacity for 2026 has not shown a precipitous decline, and the industry’s overall construction pace remains resilient.

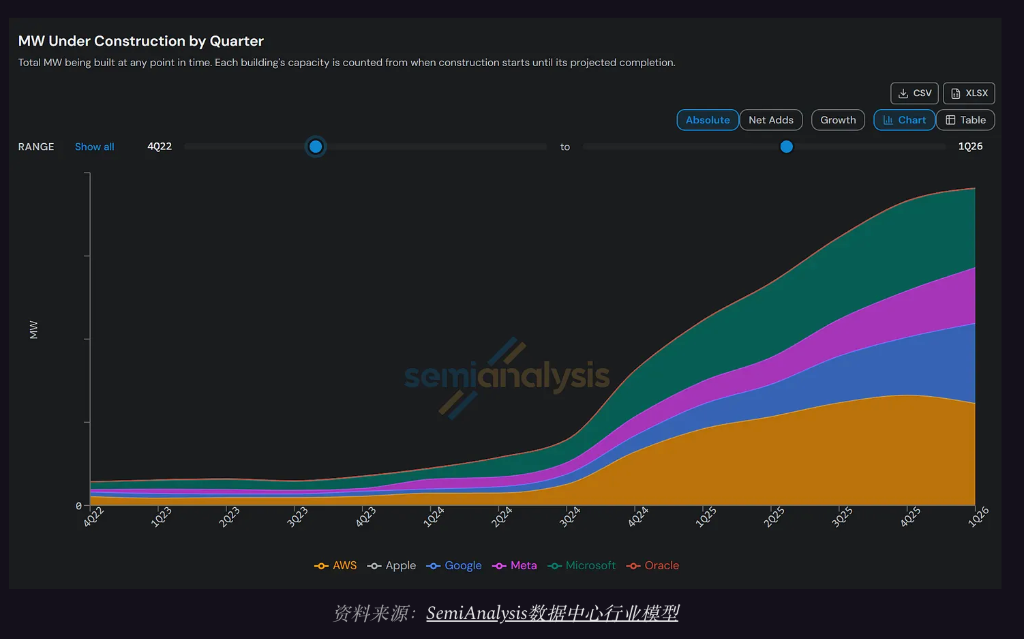

From key forecast data, in the past six months, SemiAnalysis adjusted its projection for U.S. large-scale self-built data center capacity at end-2026 by only 1%, and the fluctuation in the forecast for hosted data center capacity was less than 5%, indicating an overall stable outlook. Data shows that the industry’s capacity curve is far from the collapse suggested by market narratives.

The institution admits that localized project delays do exist, but these are normal adjustments within the large-scale infrastructure cycle and not leading indicators of declining demand. The current pessimism has been excessively amplified by the market, with sharp valuation volatility reflecting an overreaction of sentiment rather than a fundamental deterioration of the sector.

AI's "Blind Faith" in Announcements, Market "Magnifies" Panic

"Half of U.S. data center capacity will be canceled or delayed by 2026"—this statement has recently been widely circulated on financial and social media, originating from a Bloomberg report on April 1, and later amplified with more sensational headlines by multiple technology media outlets.

However, SemiAnalysis points out that this panic narrative is essentially an "AI pieced-together false alarm"—numerous so-called capacity forecast models rely solely on AI tools to scrape press releases, treat unverified GW-scale project announcements as fact, and completely ignore key variables such as actual construction timelines, grid interconnection, and approval processes.

The organization acknowledges that local project delays do exist, but the vast majority of projects labeled as "canceled or delayed" are in early stages—they lack financing, regulatory approvals, or equipment orders, and never truly had the conditions necessary for 2026 delivery.

A Mathematical Error in "Half Delayed": The Problem Lies in the Denominator

SemiAnalysis believes that the widely cited market conclusion of "50% of 2026 capacity delayed or canceled" has its main issue not in the numerator of "canceled projects," but with the denominator in the statistical sample, as sample limitations severely distort the conclusion.

According to Sightline Climate statistics quoted by the market, of the planned 12GW U.S. capacity for 2026, only 5GW is under construction. But SemiAnalysis, through independent verification with satellite imaging models, found that the self-built, in-progress capacity of the two largest U.S. hyperscale cloud providers alone has already surpassed 5GW, without even counting the multi-GW scale projects under development by third-party developers.

This means that Sightline’s calculation scope only covers major public "lighthouse" projects and does not encompass the entire industry development pipeline. Such publicly announced early projects by nature have high uncertainty and are prone to delays or cancellations.

Therefore, the claim that "half of capacity is delayed" only applies to niche speculative announcement projects and does not represent the overall U.S. data center construction landscape or define the real industry climate.

Delays Are Real, but Causes Are Clear and Impact Is Controllable

SemiAnalysis does not deny the presence of delays in the industry and had previously warned of project risks for STACK Infrastructure, Oracle, Nebius, Core Scientific, and others. However, the organization clearly states that the industry delays are not systemic shutdowns but are concentrated in certain scenarios, and divides market delay cases into three core types.

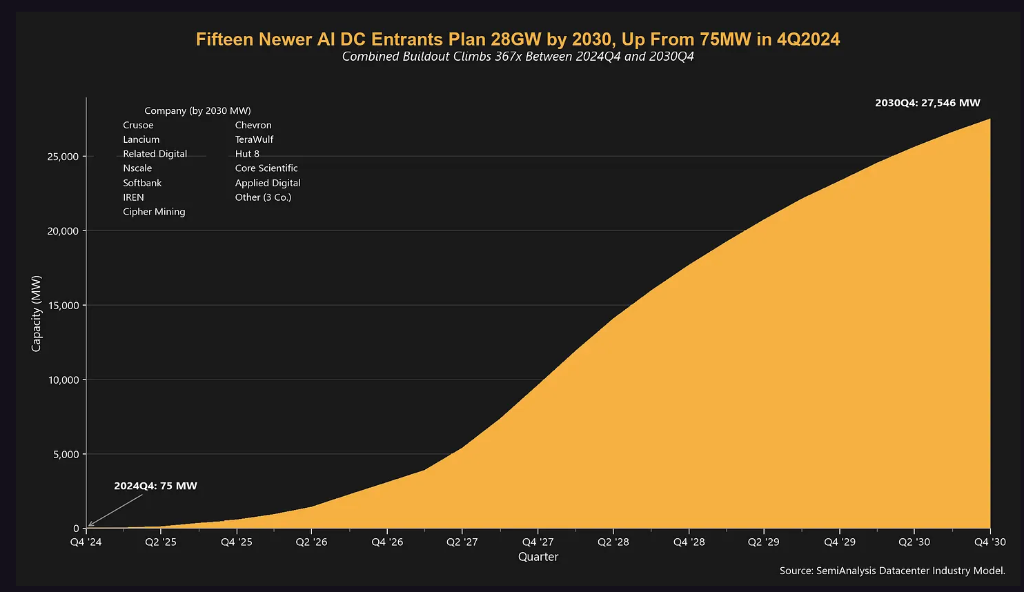

- The first type is early-stage speculative projects, usually launched by new industry entrants. These have aggressive blueprints and unrealistic delivery timelines and have not entered substantial implementation.

- The second type involves scheduling deviations in mature projects, where developers underestimate factors such as equipment delivery, weather, and MEP commissioning, leading to overoptimistic views of the construction cycle.

- The third type is compliance-related delays, where, in the later stages of construction, projects face regulatory or local sentiment hurdles, forcing redesigns or power source changes, thus extending the delivery cycle.

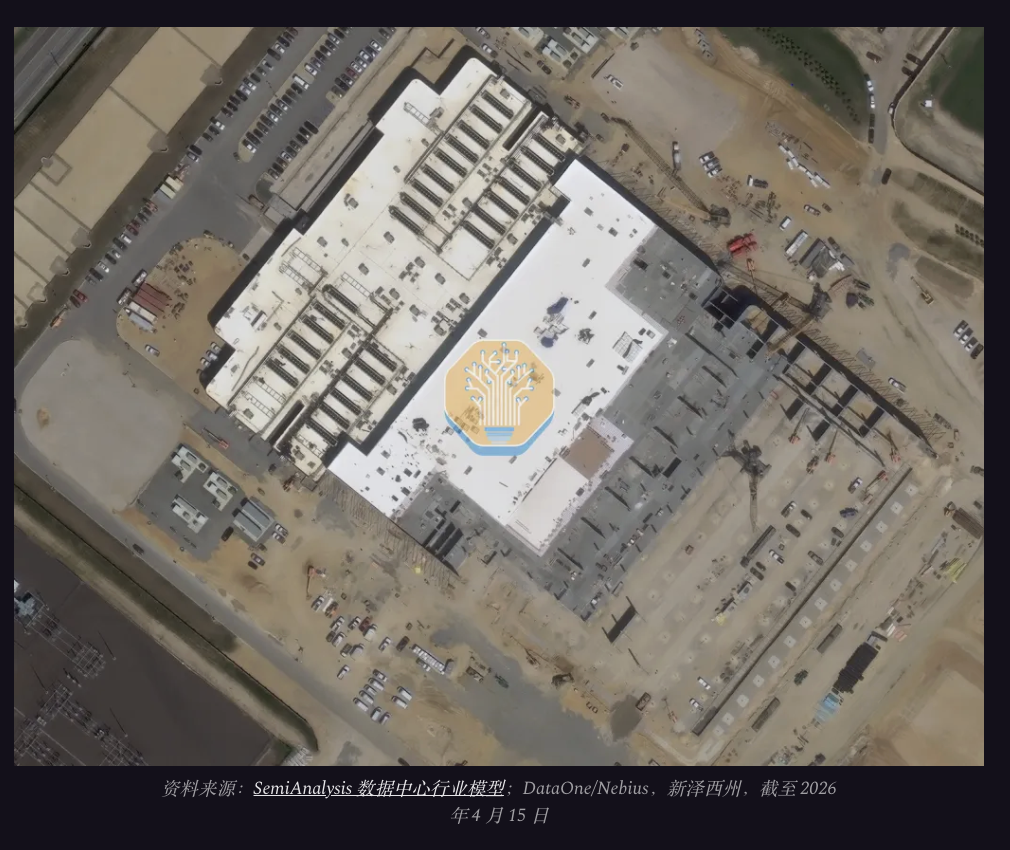

Take the Nebius New Jersey campus as an example: its first-phase 50MW was originally planned to go live in four months but eventually took ten months to deliver—a typical second-type delay case. Core Scientific’s Denton campus, due to regulatory blockages, design changes, and supply chain interruptions, missed its 250MW annual delivery target—an overlap of type one and two delays.

The Oracle/STACK New Mexico project is a classic third-type delay case—pipeline constraints and emissions review delays pushed the go-live date from 2026 straight to 2029. All three cases point to the same conclusion: delays are real, but their scope is relatively concentrated and their causes are traceable.

Essence of Market Panic: Three Types of Ineffective Noise Disrupt Core Judgments

According to SemiAnalysis, the current round of market-wide panic essentially stems from three types of "noise information" without substantive industry impact, which have exaggerated the sector’s short-term risk.

The first is local construction moratorium policies. By April 2026, twelve U.S. states had introduced regulatory bills, but these only apply to early-stage planning projects and do not affect 2026’s core delivery capacity. The Maine ban involves less than 5MW in planned capacity and has virtually no impact.

The second is regional sentiment resistance. Local protests, zoning rejections, or enterprises withdrawing are mostly limited to paper plans without land, equipment, or grid agreements, and were never counted as effective delivery capacity—they do not affect real contracts.

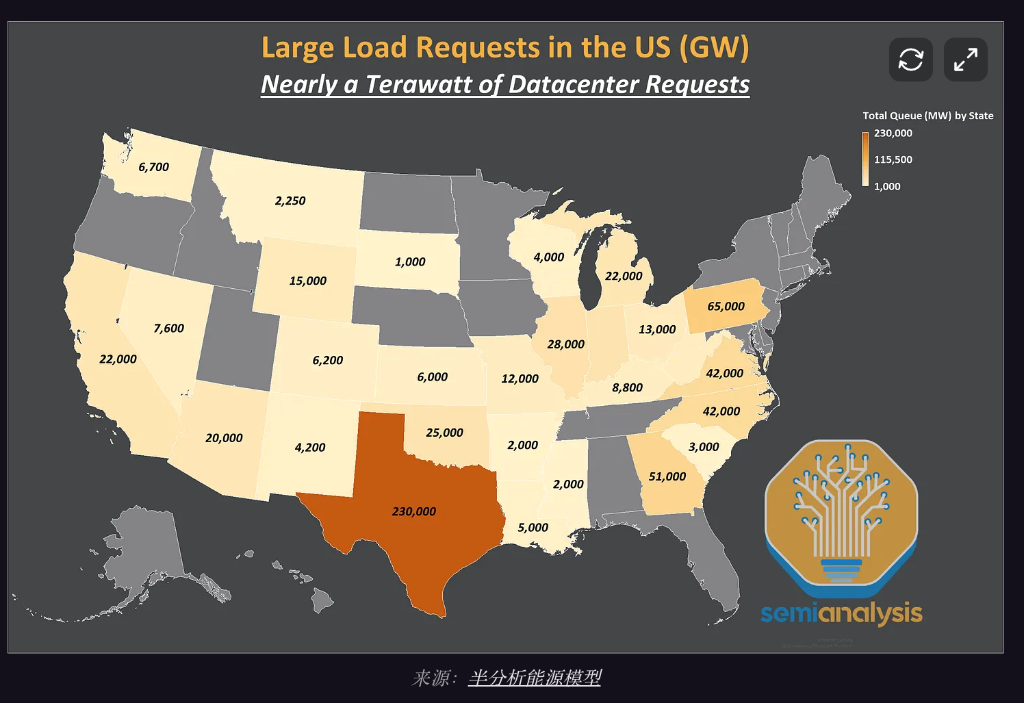

The third is an abundance of invalid project announcements. The grid interconnection application queues are filled with "virtual capacity." For example, Texas’s ERCOT has received over 410GW of data center load applications—five times the historical peak—with SemiAnalysis estimating about 311GW is speculative and cannot be converted into real capacity.

Risk Is Being Purged, Not Demand Collapsing

SemiAnalysis believes that the fundamental cause of market pessimism is the failure to distinguish between different levels of project risk.

The projects delayed or canceled in this cycle are heavily concentrated among early-stage speculative players—structural surplus in the industry—while the core 2026 delivery capacity comes from high-certainty, premium projects, all of which generally have secured land tenure, set power solutions, finalized compliance approvals, locked-in long-term equipment orders, and substantial construction progress.

Leading operators have already developed mature solutions to industry-wide bottlenecks. In policy terms, they work closely with local governments and communities, withdraw early from high-resistance regions, and turn to policy-friendly or brownfield development. On hardware, they address pain points such as seven to ten years for grid connections or more than one year for core equipment by directly investing in the grid, securing electrified land, deploying distributed generation, pre-paying to lock in equipment capacity, and adopting modular prefabricated construction—effectively hedging supply chain and infrastructure constraints to ensure core projects progress on schedule.

Therefore, panic stems more from risk misjudgment; the industry’s fundamental support has not wavered.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Aave Proposes Cross-Chain sGHO Stablecoin Expansion

BlackBerry stock surges 23% as QNX software powers AI and robotics

Ethereum Outlook Weakens as Key Support Faces Pressure

Analyst Diana said $XRP’s path to $50 depends on demand consistently outpacing supply