Bitget UEX Daily | US-Iran Talks Off to a Rocky Start, Oil Rebounds; Marvell and Others Join S&P 500, SK Hynix Eyes US Listing; Energy Fuels Secures US Government Support

2026/06/22 01:36

2026/06/22 01:36

一、Key Headlines

Federal Reserve Developments

Deutsche Bank Turns Hawkish: Expects 50bp Fed Rate Hikes in 2026

- Deutsche Bank raised its inflation forecasts and now projects the Fed will deliver two rate hikes in 2026 (totaling 50 basis points), pushing the federal funds rate to 4.1%. An earlier move as soon as July cannot be ruled out.

- Facing persistent inflation and the hawkish stance of new Chair Warsh, the bank reversed its prior dovish outlook, emphasizing a “higher for longer” macro environment.

- Market Impact: Traders have sharply raised the probability of a September hike. Short-end Treasury volatility is expected to rise while the long end stabilizes, forcing rate-sensitive assets to reprice.

International Commodities

US-Iran Talks Start Poorly, Oil Rebounds Over 2%

- After President Trump threatened strikes on Iran if Hezbollah continues attacks on Israel, early US-Iran talks in Switzerland showed tension and Iran paused parts of the dialogue.

- In early Asian trading, Brent crude surged more than 2% to around $82.30 per barrel, while WTI broke above $78. Trading volume was notably active.

- Market Impact: Geopolitical risk premium has returned, providing short-term oil support. Longer-term direction depends on negotiation progress and Strait of Hormuz restoration.

Macroeconomic Policy

Goldman Sachs and Others Monitor Warsh’s Hawkish Comments on Bond Market

- In his first post-FOMC remarks, Warsh stressed inflation-fighting as the top priority, surprising markets and prompting bets on earlier rate hikes.

- Goldman Sachs noted this would increase short-end Treasury volatility while calming the long end.

- Market Impact: Fixed-income markets face valuation adjustments. Combined with geopolitical factors, macro uncertainty is rising.

二、Market Review

Commodities & FX Performance (Real-Time)

- Spot Gold: $4187/oz, +0.77%

- Spot Silver: $65.88/oz, +1.53%

- WTI Crude: $77.53/bbl, +2.29%

- Brent Crude: $81.32/bbl, +1.77%

- US Dollar Index (DXY): 100.844, +0.08%

Driver Analysis: Early tensions in US-Iran talks have revived geopolitical concerns, driving oil’s rebound. Risks around the Strait of Hormuz persist despite partial Gulf traffic recovery; low inventories continue to provide a floor. The dollar remains relatively stable, while hawkish Fed signals (Warsh remarks and Deutsche Bank forecast) cap further upside in precious metals, though inflation expectations and safe-haven demand offer support. In the short term, the correlation between oil, gold, and silver reflects the tug-of-war between risk sentiment and macro expectations. If talks yield concrete progress, oil pressure may mount; otherwise, volatility will persist. Institutional consensus sees geopolitics dominating near-term oil moves, while the Fed path will influence precious metals and the dollar.

Cryptocurrency Performance

- BTC: $63,853, -0.66%

- ETH: $1,728, -0.60%

- Total Crypto Market Cap: $2.27 trillion, -0.60%

- Market Liquidations: 24h total ~$141 million (longs dominant)

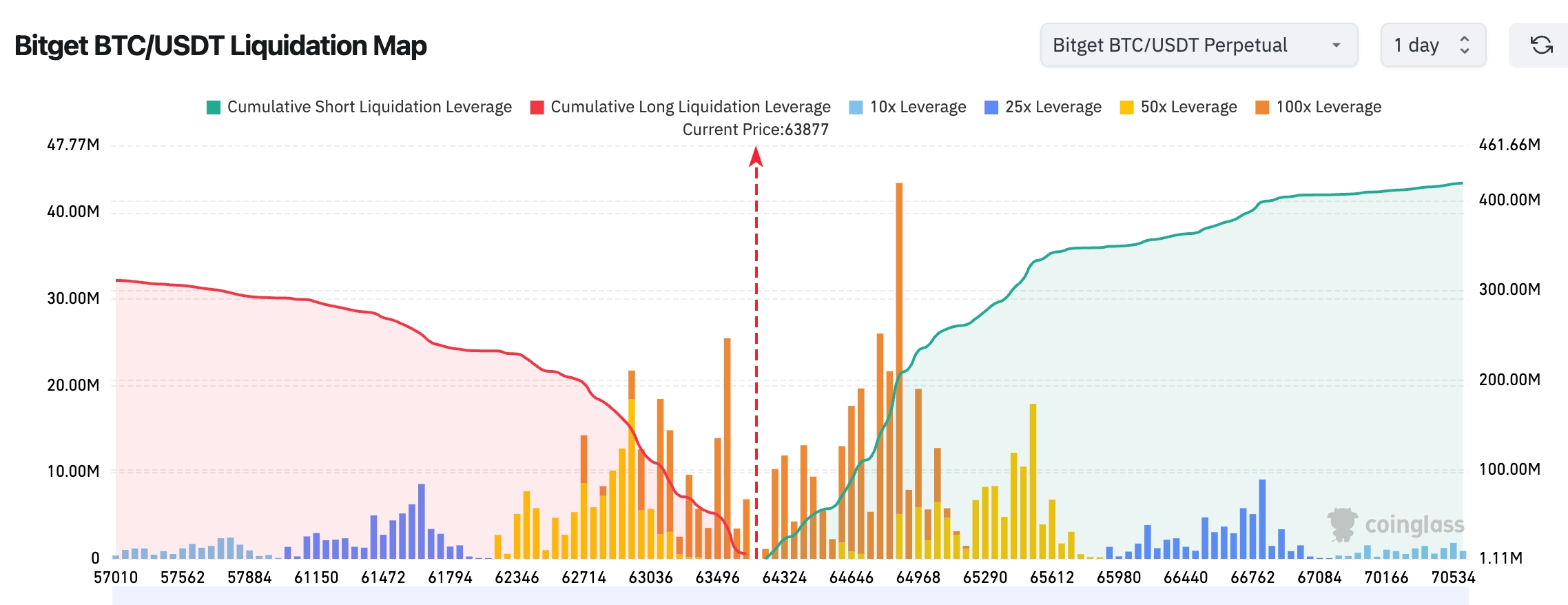

- Bitget BTC/USDT Liquidation Map: Current price around $63,877. Significant short liquidation clusters above at $64,500–$65,500 (strong upward liquidity sweep potential). Major long liquidation zone below at $62,700–$63,200; breach could trigger further downside.

Driver Analysis: Geopolitical tensions and hawkish Fed expectations are weighing on risk assets. BTC and ETH face near-term pressure, yet total market cap shows resilience. Liquidations are concentrated in longs, reflecting caution over heightened volatility. ETF flows turned negative, signaling institutional caution. Technically, BTC hovers near key support while ETH lags. Macro factors (oil rebound, Treasury yields) clash with AI narratives. Institutions believe short-term direction hinges on negotiation outcomes and Fed signals; longer term, ETF inflows and compute demand remain supportive. BTC/ETH divergence may continue—watch for post-deleveraging rebound potential.

US Stock Index Performance

- Dow Jones: ~51,564.7 points, +0.14%

- S&P 500: 7,500.58 points, +1.08%

- Nasdaq: 26,517.93 points, +1.91%

Tech Giants Performance

- NVDA: $210.69, +2.95%

- AAPL: $297.20, +0.70%

- MSFT: $399.14, +2.15%

- GOOGL: $368.03, +1.17%

- AMZN: $243.15, -0.51%

- META: $577.22, +1.67%

- TSLA: $398.50, +0.55%

Performance Summary & Driver Analysis: Tech sector broadly advanced, led by a >6% surge in the semiconductor index with multiple chip stocks hitting record closes. Legacy players like Intel diverge from AI leaders like Nvidia: the former benefits from advanced packaging and glass substrate roadmaps, while the latter dominates compute demand. Amazon’s talks to sell Trainium chips, along with Google and Broadcom copying Nvidia’s financing playbook, signal a shift from single-supplier dominance to multi-vendor closed-loop ecosystems in AI infrastructure. Valuation pressures and company-specific events (e.g., SpaceX bond issuance, Meta data-center deals) drive differentiation. Overall momentum remains AI-commercialization led, but investors must watch for macro tightening risks.

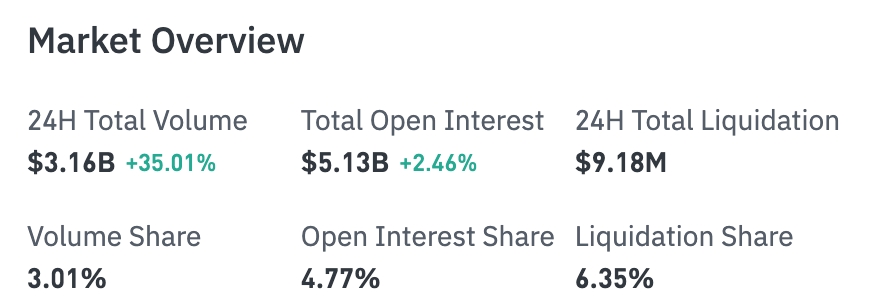

Crypto-Related Stock Contracts Overview

- 24H Total Volume: $3.16 billion (+35.01%)

- Total Open Interest: $5.13 billion (+2.46%)

- 24H Total Liquidations: $9.18 million

- Proportions: Volume 3.01%, OI 4.77%, Liquidations 6.35%

Sector OI Performance (Major Sectors)

- Technology: $2.64 billion

- Financials: $169 million

- Consumer: $70.34 million

- Industrials: $30.95 million

- Biotechnology: $17.30 million

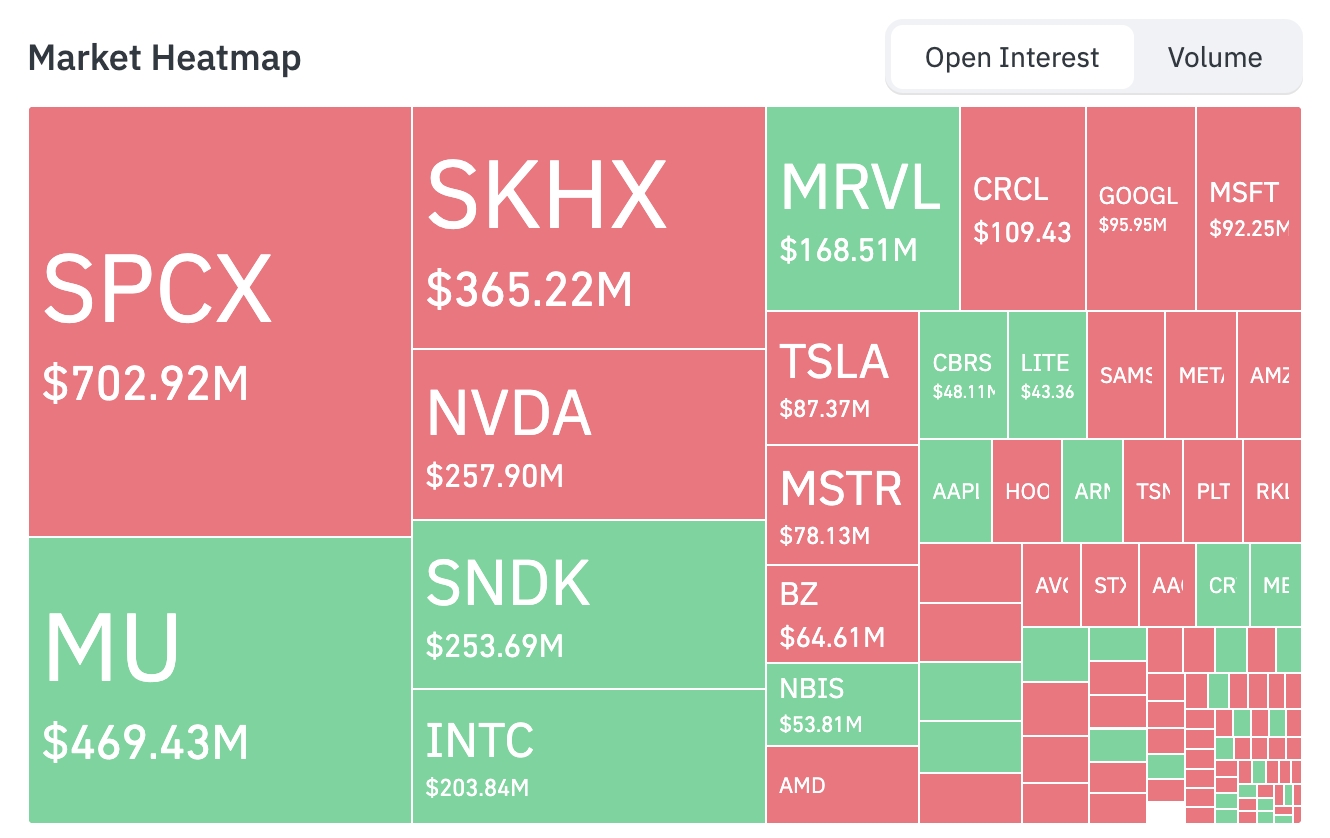

Market Heatmap (OI-Focused) Top Asset OI Rankings (in $100 million):

SPCX: 7.03 | MU: 4.69 | SKHX: 3.65 | NVDA: 2.58 | SNDK: 2.54 | INTC: 2.04 | MRVL: 1.69 | CRCL: 1.09 | GOOGL: 0.96 | MSFT: 0.92 | TSLA: 0.87 | MSTR: 0.78

Funds flowed into semiconductor-related names such as MU, MRVL, SNDK, and INTC (increased positioning), while SPCX, SKHX, NVDA, TSLA, MSTR, AMD, GOOGL, and MSFT saw position reductions.

Sector Rotation Highlights Semiconductor Sector Up Over 6%

- Representative stocks: SanDisk +11%, Intel +10%, Micron +8%, TSMC/Qualcomm +6%, NXP/Broadcom/Western Digital/Applied Materials/AMD +4%, ASML +3%, NVIDIA +2.95%. Multiple stocks hit all-time closing highs.

- Drivers: AI inference demand is accelerating from model training to commercial deployment, with compute shortages far exceeding supply. Bernstein senior analyst Rasgon called this the first “true chip supercycle” of his career — semiconductor industry revenue has jumped from over $800 billion last year to a 2026 target of $1.3 trillion. Capacity bottlenecks are spreading from GPUs to HBM high-bandwidth memory, semiconductor equipment, power supply, and custom ASICs. NVIDIA GPUs and custom chips from Broadcom and others will coexist long-term to absorb massive compute demand. Amid geopolitical and macro uncertainty, AI stands out as a “deterministic” growth narrative, driving capital inflows across the entire semiconductor supply chain.

Market Implications: This move is not just short-term sentiment release but reflects deepening of the AI capital expenditure cycle and supply chain restructuring. In the short term, it benefits equipment, materials, and foundry segments. In the medium to long term, it will test companies’ execution on capacity expansion and yield ramp-up. Investors should monitor the potential impact of Fed policy on capex pace and opportunities among diversified suppliers beyond NVIDIA.

III. In-Depth U.S. Stock Analysis

1. Intel (INTC) – CEO Sets Ambitious Long-Term Goals Event Overview: In a podcast interview, Intel’s new CEO Lip-Bu Tan outlined his strategic vision for the first time, setting an ambitious goal of 10x returns within 5–10 years. The company is systematically restructuring its technology roadmap through EMIB advanced packaging, glass substrate innovation, and synthetic diamond materials to break through traditional silicon-based physical limits. The explosion of Agentic AI is driving a CPU demand recovery. The foundry business focuses on yield improvement and rebuilding customer trust, while collaborating with Musk-related projects on initiatives like Terafab. The market expects Intel’s true potential to be realized after 2030, with differentiated positioning in data centers and AI edge computing gradually materializing. Market Interpretation: Institutions generally endorse this systematic transformation path, viewing it as aligned with the current shift in AI compute from training to inference, while building long-term moats through materials and packaging innovation. Analysts are watching its potential in hybrid GPU/CPU ecosystems, especially its strategic value in finding niche breakthroughs under NVIDIA dominance. Despite short-term execution risks and competitive pressure, long-term growth catalysts are clear. Investment Implications: In the short term, closely track process yield improvements and Terafab collaboration progress. Long term, Intel’s differentiated positioning in AI infrastructure deserves strategic allocation for investors bullish on semiconductor cycle recovery.

2. Amazon (AMZN) – Expanding Custom AI Chip Sales Event Overview: Amazon is actively negotiating the sale of its Trainium and other custom AI accelerators to external companies, aiming to further weaken NVIDIA’s dominant position in the AI chip market. AWS AI head Peter DeSantis stated that AI infrastructure is evolving rapidly, with third-generation Trainium accelerators largely sold out and strong demand for the fourth generation. The company intends to leverage its internal scale to expand custom chip business from self-use to external sales, building a more complete AI supply chain closed loop. Market Interpretation: This expansion is seen as Amazon directly copying and challenging NVIDIA’s playbook, potentially reshaping cloud services and AI hardware supply chains. Institutions believe Amazon, with its massive data center demand and financing capabilities, can accelerate the industry’s transition from NVIDIA monopoly to multi-vendor competition, though it faces challenges in iteration speed and ecosystem compatibility. Investment Implications: Watch Amazon’s diversification potential in the AI ecosystem. Intensified competition may reshape industry profit distribution. It can be viewed as a long-term realization of its cloud + hardware integrated advantages.

3. SpaceX – Plans Large-Scale Bond Issuance Event Overview: Following its record IPO, SpaceX plans to hold an investor call as early as this week to issue at least $20 billion in investment-grade USD bonds to refinance a $20 billion bridge loan due in 2027. The bridge loan was provided by Bank of America, Citigroup, JPMorgan, Goldman Sachs, Morgan Stanley, and others, who will also lead the bond underwriting. The plan remains subject to adjustment but demonstrates proactive capital structure management. Market Interpretation: Institutions view this as a key step in transitioning from high-cost bridge financing to long-term investment-grade debt, reflecting strong growth prospects and debt management capabilities. Successful issuance will lower financing costs and provide more flexible funding for future expansion (Starship, satellite networks). Investors will assess cash flow stability and valuation support. Investment Implications: Bond issuance will significantly enhance financial flexibility and support long-term valuation. Suitable for long-term investors focused on aerospace and high-growth technology infrastructure.

4. Energy Fuels (UUUU) – U.S. Government Support for Rare Earth Project Event Overview: The U.S. government signed a $725 million conditional loan agreement with Energy Fuels to support the construction of domestic rare earth separation and processing capacity, aiming to reduce reliance on external supply chains. The deal is intended to strengthen domestic critical minerals self-sufficiency. Shares rose over 8% on the news. Market Interpretation: Institutions see this as an important step in U.S. supply chain security strategy. Against the backdrop of current geopolitical tensions, demand for rare earths — critical materials for AI, EVs, and defense — continues to grow. Energy Fuels is positioned to benefit from policy dividends and long-term contracts. Investment Implications: Short term, monitor loan disbursement and project execution. Long term, structural opportunities from U.S. domestic rare earth capacity expansion are favorable for investors focused on commodities and national security themes.

5. Meta Platforms (META) – Data Center AI Compute Agreement Event Overview: Meta reached a new agreement with data center developer Crusoe to purchase approximately 1.6 GW of computing power across two sites to support AI infrastructure expansion. Crusoe’s previously contracted capacity stands at 4.9 GW, with the total pipeline exceeding 40 GW. Market Interpretation: Institutions view this as a continuation of Meta’s large-scale AI investment, demonstrating proactive compute acquisition to strengthen content recommendation, advertising algorithms, and Llama model training capabilities, maintaining a leading position in the competitive AI space. Investment Implications: Monitor the efficiency of AI capex conversion. Long term, Meta’s synergistic advantages in social + AI integration deserve attention for investors bullish on digital advertising and generative AI growth.

IV. Market & Project Updates

- Institutional reports note that Bitcoin held the $59,200 cycle low after multiple tests and rebounded 3.54% this week to close at $65,655. The rise was driven more by exhausted selling pressure than new demand. Open interest in futures has fallen significantly from May highs. Short-term holders sold at a loss, and exchange balances hit a seven-year low, indicating a phase of deleveraging and selling pressure release. Short-term holders remain in ~17%–19% unrealized losses, with potential overhead supply still heavy. Bitcoin is currently trapped between a lower support near the $54,000 cycle realized price and overhead resistance around $68,000 from short-term holders taking profit. The market structure is “selling pressure paused but buying not yet confirmed.”

- Crypto mining company Ionic Digital released its May 2026 mining and operations update, reporting output of 24.77 BTC (up 21.1% MoM). It sold no Bitcoin, maintained zero debt, and increased total holdings to 2,861 BTC.

- 10x Research analysis suggests that BlackRock’s Bitcoin yield-enhanced ETF (BITA) may have design flaws. Its strategy of selling call options for yield could cause the fund to underperform spot Bitcoin in most market environments and may not deliver desired absolute returns.

- Data: Tokens including H, XPL, and SAHARA experienced large unlocks this week. H’s unlock was worth approximately $54.8 million.

- Yesterday, Bitcoin treasury company Strategy’s founder and executive chairman Michael Saylor once again posted Bitcoin Tracker information. Following past patterns, Strategy typically discloses Bitcoin purchases the day after such announcements.

V. Market Calendar

June 23 (Monday) Index Adjustments Effective

- MRVL (Marvell Technology) joins S&P 500

- FLEX (Flex) joins S&P 500

- ALAB (Astera Labs) joins Nasdaq 100

- CRWV (CoreWeave) joins Nasdaq 100

- NBIS (Nebius) joins Nasdaq 100

- RKLB (Rocket Lab) joins Nasdaq 100

- TER (Teradyne) joins Nasdaq 100

June 24 (Tuesday) U.S. Earnings

- FDX (FedEx) reports after market close

June 25 (Wednesday) U.S. Earnings

- MU (Micron Technology) after close

- Expected EPS: $20.7

- Expected Revenue: $35.56 billion

- TCOM (Trip.com) after close

June 26 (Thursday) U.S. Macro Data

- U.S. May PCE Price Index

- U.S. Q1 GDP Final

- U.S. Initial Jobless Claims

Key Events

- NVDA (NVIDIA) 2026 Annual Shareholder Meeting

- Blackwell chip capacity progress

- Vera architecture chip progress

- AI ecosystem commercialization progress

- Capital return plans

June 27 (Friday) U.S. Macro Data

- University of Michigan June Consumer Sentiment Final

Events to Watch (Date TBD) OpenAI

- GPT-5.6 series models possibly releasing next week (Mini, Standard, Pro versions)

SK Hynix

- SEC expected to approve ADR listing application as early as the week of June 22

- U.S. listing as early as August

Institutional Views: Prominent investment bank analysts generally believe the short-term market is dominated by uncertainty in US-Iran negotiations and hawkish Fed signals. Oil prices receive geopolitical support, but risk assets face pressure overall. Upward revisions to rate hike expectations by Deutsche Bank and others reinforce the “higher for longer” narrative, which is negative for precious metals and growth stocks. Goldman Sachs is monitoring bond market volatility transmission. The tech and AI sectors show clear differentiation. The semiconductor supercycle logic remains recognized, but valuation and competition risks require caution. Crypto market leverage reduction provides potential rebound space, while ETF outflows reflect cautious sentiment. Overall, institutions recommend focusing on data validation and negotiation progress, maintaining neutral-to-cautious positioning, and prioritizing defense against geopolitical and policy risks.

Disclaimer: The above content is compiled by AI search and manually verified for release. It does not constitute any investment advice. Data in the text may inevitably contain deviations — please refer to real-time market data.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Charles Hoskinson Tests Zero-Knowledge Wallet Recovery for Cardano

Bitcoin Sell-Off Risk Grows as Key On-Chain Metric Turns Negative, Analyst Warns

Dark Defender Says “I Am Adding More XRP to My Bag”. Here’s why

Bitget Launches Third Anti-Scam Month With Multi-Asset Fraud Report