Goldman Sachs warns: U.S. stocks are extremely crowded, market volatility will persist

The US stock market is accumulating a new wave of volatility risk amid record-breaking capital activity and an extremely crowded position structure.

John Flood, Head of Equity Flow Strategy and Partner at Goldman Sachs, warned in the latest market assessment report that although overall investor sentiment remains relatively balanced, both long and short crowdedness are approaching their most extreme levels in the past five years. Coupled with short-term selling pressure from quarter-end pension rebalancing, investors should be prepared for sustained volatility.

Meanwhile, Goldman Sachs has lowered the probability of a US economic recession from 25% to 15%, and raised its GDP growth forecast for the second half of the year to 2%, indicating that overall fundamentals remain supportive.

The most immediate short-term pressure facing the market comes from technical selling at quarter-end. About $30 billion in US equities will be sold early next week due to quarter-end pension rebalancing, a scale that ranks at the 89th percentile of all buy-sell estimates in the past three years and at the 95th percentile since January 2000.

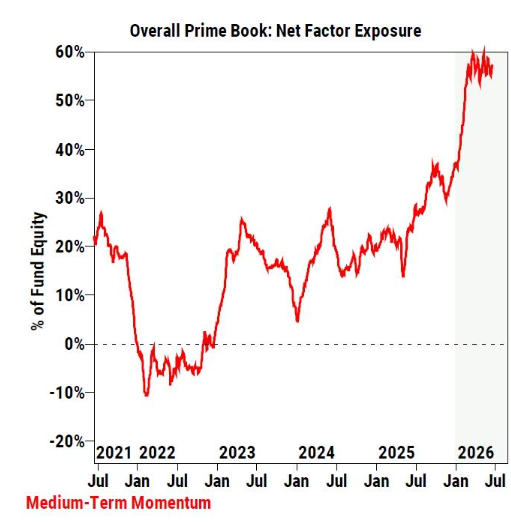

Crowdedness Approaching Five-Year Extremes, Record High Momentum Factor Exposure

John Flood, citing Prime Book data, pointed out that there are three notable thematic trends in the current market, with position crowdedness being the most acute.

Data shows that both Long Crowdedness and Short Crowdedness factor exposures are nearing five-year extremes. At the same time, intermediate-term momentum factor exposure remains near a record high at the 98th percentile over the past five years, indicating the market’s heavy reliance on trend trading. Should trends reverse, deleveraging pressures could expand rapidly.

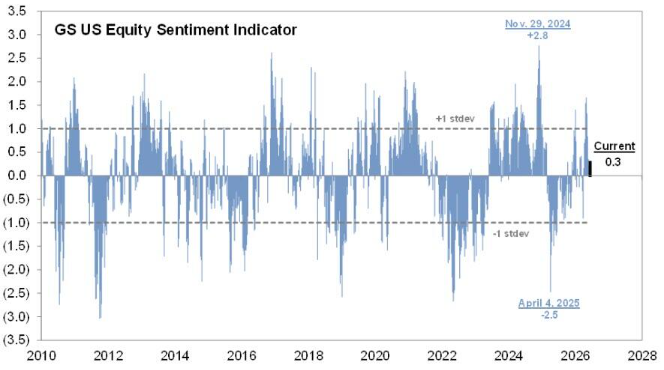

In terms of sentiment indicators, the US equity sentiment indicator currently reads +0.3, the lowest since early April. US institutional investors contribute most of the concern in the nine subindices making up the indicator. The AAII (American Association of Individual Investors) bullish sentiment index is at 36, below the year-to-date average and far below this year’s highs.

On the hedge fund front, Prime Brokerage data shows that the total leverage ratio for US long-short strategies stands at 207.3%, at the 4th percentile over the past year; net leverage is 54.5%, at the 74th percentile for the same period. Flood believes that, overall, hedge fund positions have not reached extreme levels, but the structural shift in the tech sector warrants attention—the US information technology sector exposure has surged to a five-year high, while both total and net exposure to “Mag 7” stocks have dropped to a one-year low, mainly driven by short selling since June. Flood notes that this may offer some interesting long entry opportunities.

Record Capital Market Activity Smoothly Digested by the Market

Despite the increasingly extreme positioning, the US stock market has shown considerable resilience in the face of recent record-breaking capital market activity.

On June 3, Google’s parent company Alphabet completed a $40 billion equity financing, setting a record for the largest primary market fundraising by a US corporation, surpassing Boeing’s $25 billion in 2024. However, this record lasted only six trading days, as SpaceX completed a $75 billion IPO on June 12, setting a new record. The two deals together injected over $115 billion in stock supply into the market, which was smoothly absorbed within less than two weeks.

Flood noted that prior to the SpaceX IPO, there were concerns that long-only institutional investors would sell existing holdings to free up capital. However, Goldman Sachs trading desks did not observe significant fundraising-driven selling by asset managers or sovereign wealth funds. Mutual funds currently hold about $170 billion in cash, roughly in line with historical averages, indicating there is still ample “dry powder” in the market.

The continued buying from retail investors is another key support. On June 18 (coinciding with the Russell Rebalance and SpaceX’s listing), a record 33 billion shares were traded in US equity markets in a single day, exceeding the previous record of 30 billion set on “Liberation Day,” April 9, 2025. Flood believes that strong retail buy flows will persist through year-end, serving as a tailwind for the market.

Semiconductor Holdings at Record High, Signs of Broader Sector Rotation

According to Prime Book flow data, the semiconductor and semiconductor equipment sectors continue to attract strong inflows. This sector was already the globally most bought subsector in 2025, reclaimed the top spot in the first half of 2026, and its net allocation has doubled year-to-date to a record high. This year’s buying activity has been mainly driven by Asian chipmakers.

Meanwhile, since June, US single-stock flows have shown notable broadening—eight out of eleven sectors have seen net inflows, with financials, industrials, and consumer discretionary leading the way, while information technology and energy have the highest net outflows. Flood believes that if this broadening trend continues into the second half of 2026, it would be a positive signal for the market.

Inflation and Rate Hike Risks Emerge as Chief Concerns for H2

On fundamentals, there remains optimism about earnings prospects. In Q1, S&P 500 constituent EPS grew 18% year-over-year (excluding one-offs), with the median stock’s profit growth at 14%, making it one of the strongest quarters in a decade. Should the S&P 500 break 8,000 points in 2026, earnings will be the core driver, with AI infrastructure-related stocks expected to contribute about half of the S&P 500’s profit growth this year.

However, inflation and rising interest rate risks have become the primary concern heading into the second half. Flood points out that newly appointed Fed Chair Warsh’s first FOMC meeting was more hawkish than the market expected—of the 18 participants submitting rate forecasts, half expect one or more hikes during the remainder of 2026, and the median forecast for core PCE inflation in Q4 2027 has risen to 2.5%.

In response, Goldman Sachs economists maintain their baseline forecast, seeing no rate hikes as the most likely scenario. Their reasons: roughly half the rate hike forecasts come from regional Fed presidents without voting rights, while most voting members still lean towards holding or cutting rates; in addition, rapid improvement in the Middle East and a sharp drop in energy prices may render these forecasts outdated. Simultaneously, they have reduced the probability of a US recession from 25% to 15% and raised the sequential GDP growth forecast for the second half to 2%.

Flood concludes with a quote from Benjamin Disraeli: “There is no education like adversity.” His conclusion is straightforward: be prepared for sustained volatility.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

SPX Blocks Musk's Loss-Making SPCX

Bitcoin tumbles to new multi-year low of $58,000, but a short-squeeze setup emerges

Bitcoin Treasury Companies Are ‘Textbook Bubble Chart’ as MSTR Loses $100

Analyst Argues the Fed Could Catch Everyone Off Guard and Explains How It Would Affect Bitcoin