The Value of Micron's Long-term Contracts: Customers Commit $22 Billion Upfront, Contracts Are Non-cancellable, and Lock in a 'Historically High' Profit Margin!

Customers first pay a $22 billion deposit, sign non-cancellable long-term contracts, and accept a pricing framework far more favorable to Micron than at any point in history—this is the core of Micron’s latest batch of Strategic Customer Agreements (SCA).

According to The Block Trading Desk, on June 25, Barclays, Morgan Stanley, and J.P. Morgan all described these as “game-changing” agreements. J.P. Morgan semiconductor analyst Harlan Sur labeled this batch of SCAs as a “fundamental shift” in Micron’s business model—from a cyclical commodity supplier to a long-term supplier with multi-year contract protection and significant downside hedges for both revenue and profit.

The value of these contracts lies in: First, their significant coverage, accounting for about 20% of DRAM volume and about a third of NAND volume; second, price and volume are tied together, and according to the 14 agreements with minimum commitment quantity and price, they represent a cumulative minimum revenue of about $100 billion; third, customers have to provide a total $22 billion in deposits and financial commitments. Fourth, the gross margin at the contract floor price is “well above historical peaks” (which were about 62%), effectively locking in a higher profit baseline for Micron.

16 Contracts Covering 20% of DRAM and One-Third of NAND

Micron disclosed that it has signed 16 SCAs with customers spanning the data center, consumer electronics, and automotive markets.

In terms of customer distribution, there are four large customers (widely speculated to include hyperscale cloud providers and major consumer electronics OEMs), three mid-sized customers, and the other nine are smaller automotive clients.

Contract terms: Data center and consumer electronics contracts are for 5 years, covering 2026 to 2030; automotive contracts are for 3 years.

Coverage scale: These 16 agreements in total cover about 20% of Micron’s DRAM shipments and about a third of its NAND shipments.

According to Barclays research, management indicated that once all planned SCAs are signed, over 50% of company revenue is expected to come from these agreements, of which those with fixed prices or price ranges are expected to account for about 40% of revenue.

$22 Billion Deposit Raises Default Costs: Clients Pay Upfront, Micron Custodies, Refunded at Maturity

Under the 16 signed agreements, Micron will receive a combined total of about $22 billion in cash deposits and other financial commitments—$18 billion in unrestricted cash and $4 billion in letters of credit.

This cash is held by Micron, remains on its balance sheet during the contract term, and is refunded to customers at maturity, with the refund schedule “back-end weighted,” meaning large repayments occur in the later stages of the agreements.

This money is not simply prepaid revenue. Its true function is to increase the cost for customers to back out.

On the binding power of these agreements, the Morgan Stanley research note directly quoted management on the analyst call: “These contracts are non-cancellable.” If customers cannot take delivery at the agreed quantity and price, Micron can act on the deposit. For Micron, this is like requiring margin on part of forward demand for the coming years; for customers, it’s a cost of certainty in supply.

This also explains why customers accept price ranges and deposit arrangements. With demand for AI servers, data center SSDs, HBM, and high-end devices pulling up, locking in supply is valuable when memory is tight.

Pricing Structure: There’s a Cap, but Floor Pricing Locks in “Gross Margin Far Above Historical Peaks”

The SCA pricing framework splits into three categories: fixed price, a price range with floors and ceilings, or reference to market price but floating within a close band.

On the ceiling: For existing products, the ceiling references Q2 2026 market price. This clause was interpreted by some in the market as Micron “intentionally capping upside,” sparking some debate.

But the real highlight is the floor price: The associated gross margin is “far above any historical profit cycle highs.” Micron’s previous peak gross margin was about 62%, while it currently reaches 84.9%—which means even if the floor price clause is triggered, Micron’s profitability far exceeds the historical best.

However, SCA is not an “always up only” contract. Some existing products have a ceiling price, with the cap pegged to Q2 2026 market price. In other words, Micron trades some future price upside for higher certainty of revenue and a strong gross margin floor.

Analyst Joseph Moore commented that “the contract price cap being set equal to Q2 pricing” did raise concerns about “the company capping upside,” but he also noted that gross margins are pushing 90% and could likely remain in this region for a considerable period—so it’s reasonable for counterparties to seek some protection, and the real measure of value is the contract’s duration.

$100 Billion Revenue Floor Is Only the “Minimum”

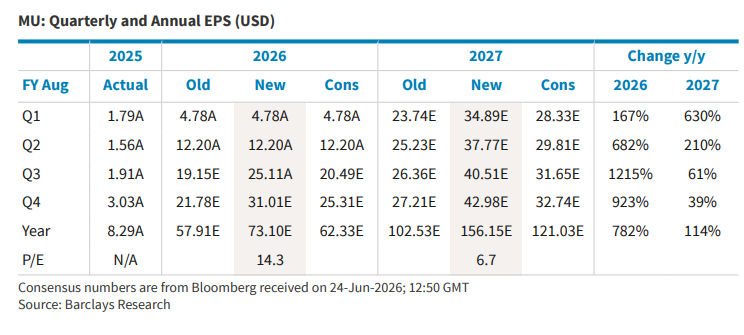

Out of 16 agreements, 14 have set pricing terms.

According to Barclays and J.P. Morgan research, the minimum committed revenue of these 14 agreements (RPO, i.e., remaining performance obligations calculated at minimum commitment quantities and prices) totals about $100 billion.

Management made it clear that actual revenue is expected to be “well above” this baseline—because that $100 billion is just the minimum calculated at the floor price; if market prices are above the floor, revenue will rise accordingly.

For new products, the agreements also reserve additional potential for price upside.

Behind the Long Contracts, Capacity Expansion Is Still Needed, CapEx Remains

Locking in demand does not mean automatic delivery.

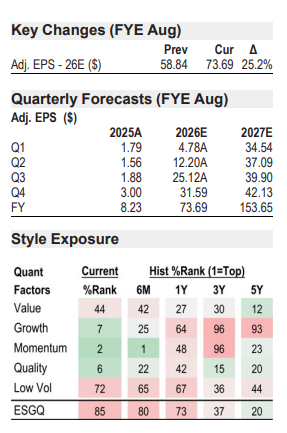

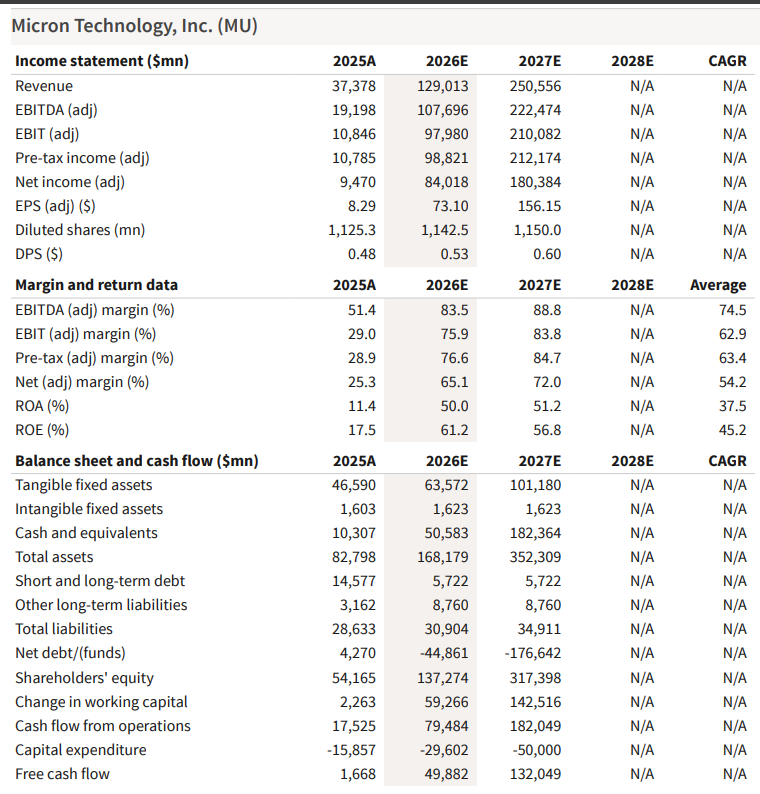

Micron raised its FY26 net capital expenditure guidance to about $27 billion, up from about $25 billion previously. FY27 quarterly capex is expected to exceed FQ4 levels, with over half of the year-on-year increase from construction-related capex for cleanroom capacity buildout in advance.

This shows SCAs don’t bring an asset-light model, but rather a more certain rationale for expansion.

Customers are willing to commit funds, and Micron will also invest. Long-term contracts justify expansion, but if future demand or pricing diverges, capacity deployment will still be a cyclical variable.

Three Major Institutions Raise Price Targets: Behind This, the Market Is Reassessing “How Long Peak Profitability Can Last”

All three firms have raised their price targets for Micron, but the rationale is not just the better-than-expected May quarter results.

Barclays (analyst Tom O'Malley): Raised target from $1175 to $2000, based on 12x CY27 EPS of $166.74. The report said the SCA details are “better than expected” and these contracts “meaningfully de-risk the downside,” while supply-demand imbalance won’t fade anytime soon, supporting further upside.

Morgan Stanley (analyst Joseph Moore): Raised target from $1050 to $1200, based on 30x through-cycle earnings ($40/share). Through-cycle earnings estimate was raised from $35 to $40, citing the run-rate moving towards $200/share.

J.P. Morgan (analyst Harlan Sur): Raised target from $550 (Dec 2026 target) to $1540 (Dec 2027 target), based on 10x (10-year median P/E) FY28 EPS of $154. The research classifies SCA expansion as a “step change,” fundamentally transforming Micron’s business model characteristics.

Behind these model changes, the key variable is profit sustainability.

Micron’s May quarter revenue reached $41.456 billion, up 73.7% QoQ; the August quarter revenue guidance midpoint is $50 billion, with non-GAAP EPS guidance midpoint at $31. The single-quarter figures are already very high, but the SCA gives the market a new question: if prices stop rising rapidly, can Micron still maintain high gross margins and FCF?

The current framework’s answer is: a portion of revenue gets stronger protection, but not all. Price ceilings, future expansion, and sustained AI demand remain boundary conditions.

Deposits and Cash Flow Unlock Capital Return Potential, but Timing Is Constrained

SCAs also bring a balance sheet change: deposits flow into Micron, and while they ultimately must be returned to customers, in the short term they boost cash on hand.

As of the May quarter, Micron had about $26 billion in cash and investments; quarterly operating cash flow was $25.4 billion, with adjusted free cash flow of $18.3 billion. Another $10 billion in customer cash deposits is expected in the August quarter.

The capital return pathway is also coming into view. U.S. CHIPS Act restrictions limit buyback capacity in the short-term; after December 9, 2026, as the window expires, company guidance calls for gradually returning 100% of excess cash to shareholders, mainly via buybacks.

This portion is not a direct SCA revenue contributor, but is another way SCA shifts the market narrative: if profits stay high and cash accumulates quickly, Micron may not just “catch the cycle,” but enter a more stable cash return model.

Earnings Itself: Record High Gross Margin, Next Quarter Guidance Beats Again

Aside from SCAs, Micron’s May quarter (FY3Q26) financials were also strong:

-

Revenue of $41.456 billion, up 73.7% QoQ, well above market expectations of $35.6 billion

-

DRAM revenue of $31.3 billion (QoQ +67%), NAND revenue of $9.9 billion (QoQ +99%)

-

DRAM ASP rose just above +60% QoQ, NAND ASP rose by about mid-80% QoQ

-

Gross margin of 84.9%, a record high, above market expectations of about 81.8%-81.9%

-

EPS of $25.11–$25.12, well above market expectations of about $20.49

August quarter (FY4Q26) guidance:

-

Revenue guidance of $50 billion (midpoint), above market expectations of about $43.1–$43.6 billion

-

Gross margin guidance about 86%, continuing to exceed market expectations

-

EPS guidance $31.00 (midpoint), above market expectations of about $25.31–$25.72

~~~~~~~~~~~~~~~~~~~~~~~~

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Only 5% of Pump.fun tokens survive past 90 days, CoinGecko study finds

Hanging Man!

Base to Activate B20 Token Standard on Mainnet Today

Bitcoin Miners Operating at Break-Even as Industry Faces ‘Most Complex Restructuring’