USD: Market Reversal on Nonfarm Payrolls Night

Morning FX

The US Dollar Index opened July with a large bearish candlestick—yesterday, the US Dollar Index plunged by 0.7%, falling back above the 100 level; USDJPY dropped 1%, retreating to the 161 line.

Yesterday’s market was quite interesting, reflecting a lot of information:

1. The intraday decline in the US dollar occurred mainly before the Nonfarm Payrolls data release (Asian and European sessions), showing clear signs of preemptive action.

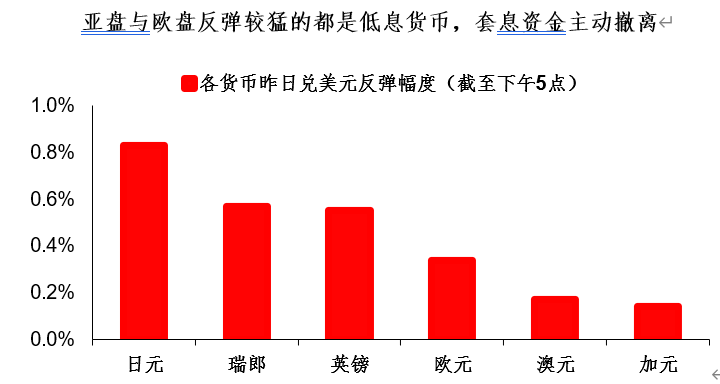

2. Currencies with the strongest intraday rebound were all low-yielding ones, such as the yen and Swiss franc. Obviously, carry trade funds are exiting.Considering the yen’s chart doesn’t look like there was official intervention from Japan, this appears more like a proactive exit by carry trade funds.

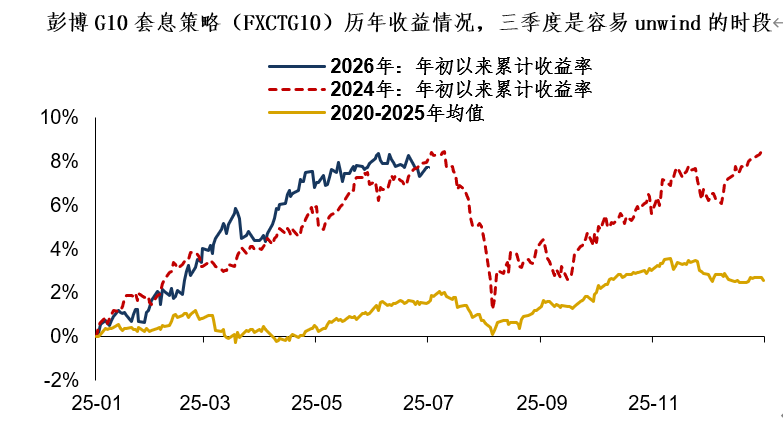

The intentions of carry trade funds are easy to understand.This is a big year for carry trades - Bloomberg’s G10 Carry Trade Strategy (FXCTG10) has accumulated a profit of 7.6% in six months. By midyear, carry trades have built up substantial floating profits, and market positioning is fairly concentrated (see “Crowded Longs on the US Dollar”). Some carry trade funds will definitely consider taking profits in stages.

After all, the case of the Carry Trade Unwind that devastated the FX market in July 2024 is a recent lesson, when the trigger was a US Nonfarm Payrolls shock and yen intervention. This year’s market environment is similar to that of 2024. Markets always have learning effects, and everyone wants to be ahead of the curve.

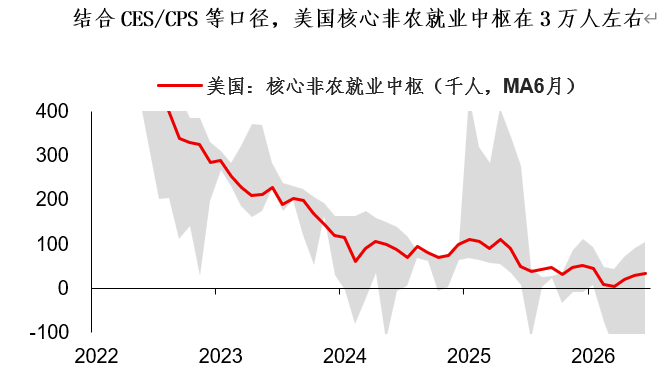

Moving into the US session, the Nonfarm Payrolls headline came in below expectations, but with clear temporary factors, so the market became “entangled” again after an initial drop.In June, Nonfarm Payrolls increased by 57,000, below the market expectation of 110,000 and even below the street whispers of around 80,000. Shrinking hiring in leisure and hospitality was the main reason for the weaker than expected NFP (World Cup + statistical factors). Last month, the sector added 40,000 jobs; this month, it decreased by 60,000—a net swing of 100,000—explaining most of the shortfall.

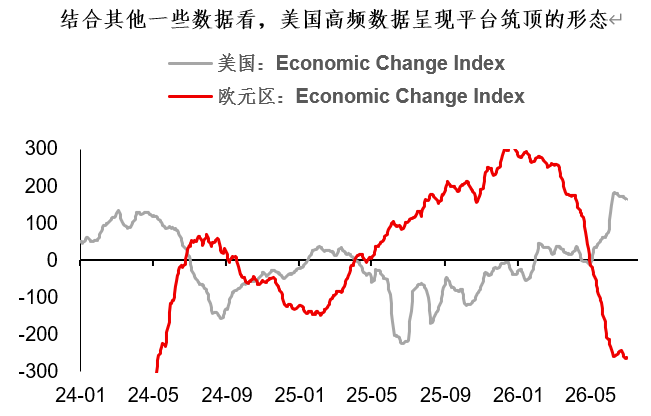

For highly volatile Nonfarm Payrolls data, a single month’s reading doesn’t say much. But, combined with other data, high-frequency data in the US indeed show a topping pattern.Previously, with the data in the euro area so weak, the market didn’t pay much attention. In my view, the more far-reaching issue with this lower-than-expected Nonfarm headline is: Has the US economy entered a post-recovery plateau?

Back to the market, what is the outlook? I believe there are several points:

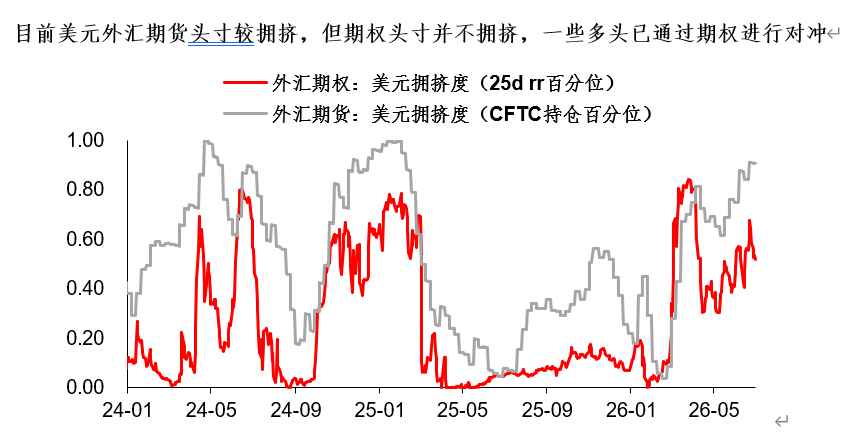

1. Asian and European sessions in early July have already shown that markets have spontaneous carry trade profit-taking demand.After all, the lessons of 2024 are recent, and Q3 is inherently a period prone to unwinds. Carry trade profit-taking is naturally bearish for the dollar and other high-yielding currencies, but many dollar longs have hedged through options strategies such as Sell Calls/buy Puts this time, so the risk of a stampede decline is not high.

2. “Has the US economy entered a post-recovery plateau?” This question is very important for US Treasuries and other rates products. Because if high-frequency data remain flat, there will be no room for the Fed to hike aggressively, and rate hike expectations would have to be revised... Currently, the market-implied probability of a Fed rate hike in September is about 60%, so there’s still room for speculation.

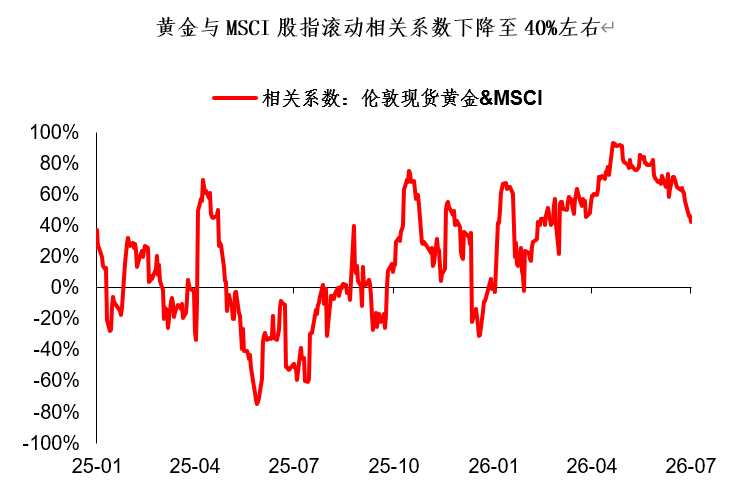

3. Some people resign and head home, while others race to the exam halls overnight. Since there is spontaneous demand for unwinding popular trades, there must be some of the “disappointed assets” from the first half of the year that can come out ahead. The key here is to watch gold and silver—both saw thorough shakeouts in Q2.Currently, the correlation between London gold spot and the MSCI equity index has dropped to around 40%, close to the healthy range; it should be a good time to allocate.

Summary of today’s sharing:

1. The US Dollar Index opened July with a large bearish candlestick, and yesterday’s market reflected a lot of information.There is spontaneous carry trade profit-taking demand, since carry trade positions in the first half of the year accumulated considerable floating profits and market positions are quite concentrated, so some carry trade funds are bound to consider staged profit-taking.

2. Moving into US session, the Nonfarm Payrolls headline missed expectations, but with clear temporary factors; after an initial dip, the market got “entangled” again. From some high-frequency data, the high-frequency economy indeed shows a topping pattern, so the deeper issue is: has the US economy entered a post-recovery plateau?

3. In FX, carry trade profit-taking is naturally bearish for the dollar and other high-yielding currencies; but the chance of a stampede in this round is low. In rates, there is room for a pullback and speculation on U.S. rate hike expectations. In precious metals, both gold and silver saw thorough shake-outs in Q2, and now should be a good allocation opportunity.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Robinhood Layer 2 integration fuels 14% Uniswap price jump

Is It Time to Buy Bitcoin? Analysts Say History May Be Repeating Itself

Is the Worldcoin Price Ready for a Reversal? WLD Rebounds After 40% Drop but Bulls Remain Uncertain

BMNR Stock Price Prediction 2026, 2027, 2030 – 2040: How High Can Bitmine Go If Ethereum Surges?