Medifast's (NYSE:MED) Q4 CY2025 Sales Top Estimates

Wellness company Medifast (NYSE:MED) reported Q4 CY2025 results

Is now the time to buy Medifast?

Medifast (MED) Q4 CY2025 Highlights:

- Revenue: $75.1 million vs analyst estimates of $71.4 million (36.9% year-on-year decline, 5.2% beat)

- EPS (GAAP): -$1.65 vs analyst estimates of -$0.82 (significant miss)

- Revenue Guidance for Q1 CY2026 is $72.5 million at the midpoint, below analyst estimates of $85.5 million

- EPS (GAAP) guidance for the upcoming financial year 2026 is -$2.15 at the midpoint, missing analyst estimates by 33.5%

- Operating Margin: -10.4%, down from 0.6% in the same quarter last year

- Market Capitalization: $110.7 million

“As we enter 2026, Medifast is moving from defining its business transformation strategy to executing on a new path to growth, leading to profitability as we become wholly focused on optimal metabolic health,” said Dan Chard, Chairman and Chief Executive Officer of Medifast.

Company Overview

Known for its Optavia program that combines portion-controlled meal replacements with coaching, Medifast (NYSE:MED) has a broad product portfolio of bars, snacks, drinks, and desserts for those looking to lose weight or consume healthier foods.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

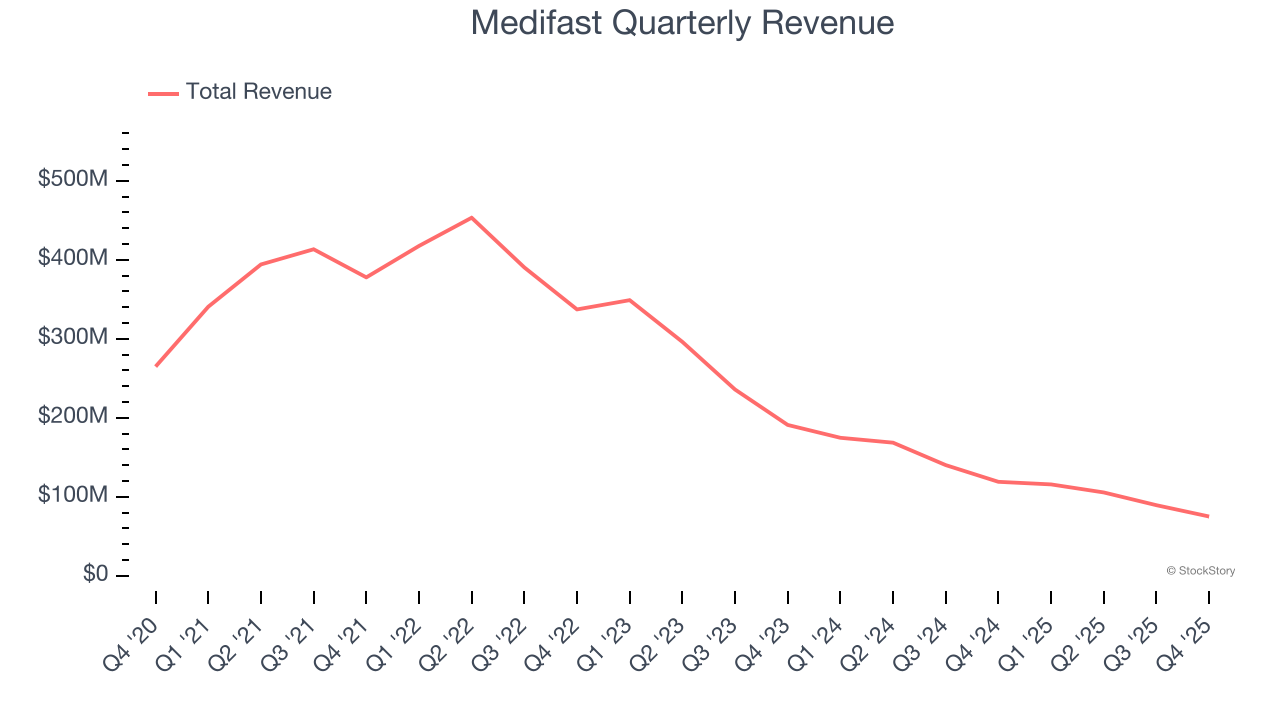

With $385.8 million in revenue over the past 12 months, Medifast is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Medifast’s demand was weak over the last three years. Its sales fell by 37.7% annually, a tough starting point for our analysis.

This quarter, Medifast’s revenue fell by 36.9% year on year to $75.1 million but beat Wall Street’s estimates by 5.2%. Company management is currently guiding for a 37.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 12.5% over the next 12 months. it’s hard to get excited about a company that is struggling with demand.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming.

Cash Is King

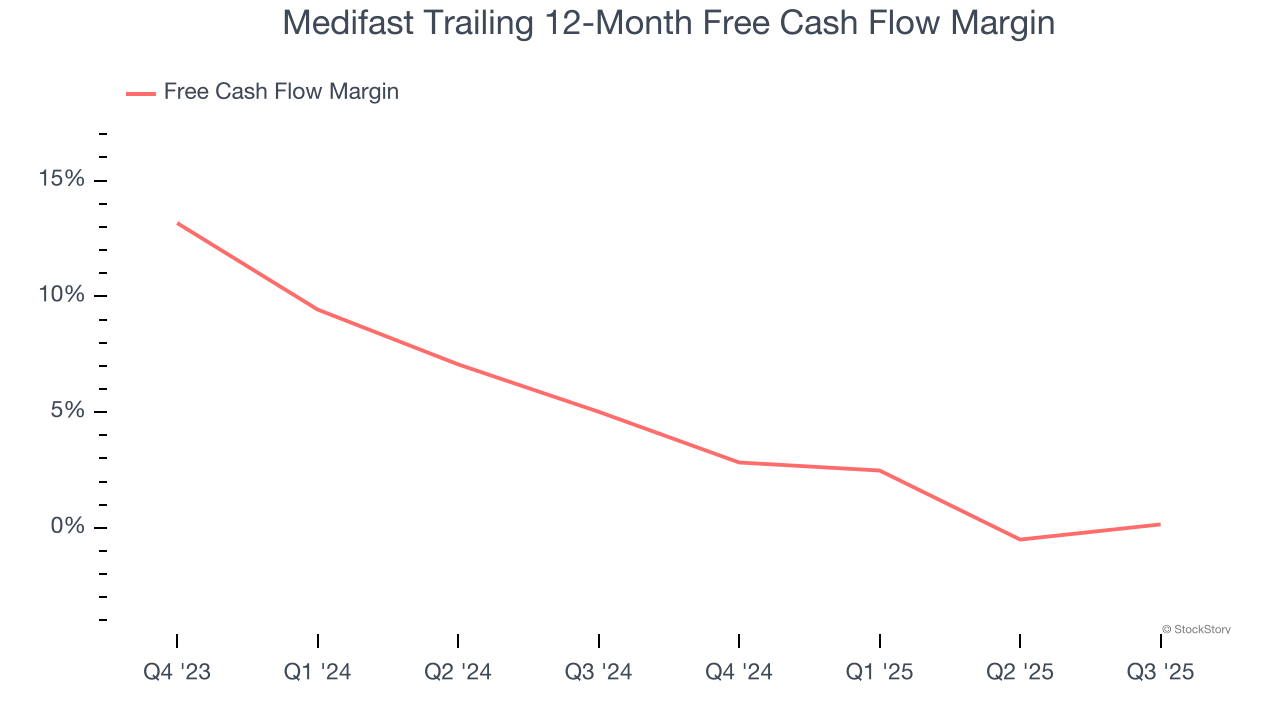

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Medifast has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.7%, subpar for a consumer staples business.

Key Takeaways from Medifast’s Q4 Results

We enjoyed seeing Medifast beat analysts’ revenue expectations this quarter. We were also happy its gross margin outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.4% to $10.52 immediately after reporting.

Medifast’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Wage Price Index, Australia, December 2025

Autodesk (ADSK) Stock Sinks As Market Gains: What You Should Know

MongoDB (MDB) Stock Falls Amid Market Uptick: What Investors Need to Know

Why Sunrun (RUN) Outpaced the Stock Market Today