Sprout Social (NASDAQ:SPT) Beats Q4 CY2025 Sales Expectations

Social media management platform Sprout Social (NASDAQ:SPT) reported Q4 CY2025 results

Is now the time to buy Sprout Social?

Sprout Social (SPT) Q4 CY2025 Highlights:

- Revenue: $120.9 million vs analyst estimates of $118.8 million (12.9% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.20 vs analyst estimates of $0.16 (26.3% beat)

- Adjusted Operating Income: $11.51 million vs analyst estimates of $10.24 million (9.5% margin, 12.5% beat)

- Revenue Guidance for Q1 CY2026 is $120.3 million at the midpoint, below analyst estimates of $121.3 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.93 at the midpoint, beating analyst estimates by 3%

- Operating Margin: -9%, up from -12.8% in the same quarter last year

- Free Cash Flow Margin: 9%, up from 7.4% in the previous quarter

- Billings: $153.9 million at quarter end, up 12.7% year on year

- Market Capitalization: $400.1 million

“Our team delivered strong results in the fourth quarter, highlighted by 15% total RPO growth and strong non-GAAP profitability," said Ryan Barretto, CEO of Sprout Social.

Company Overview

Born from the recognition that businesses needed a centralized way to handle their growing social media presence, Sprout Social (NASDAQ:SPT) provides a comprehensive software platform that helps businesses manage, analyze, and optimize their presence across various social media networks.

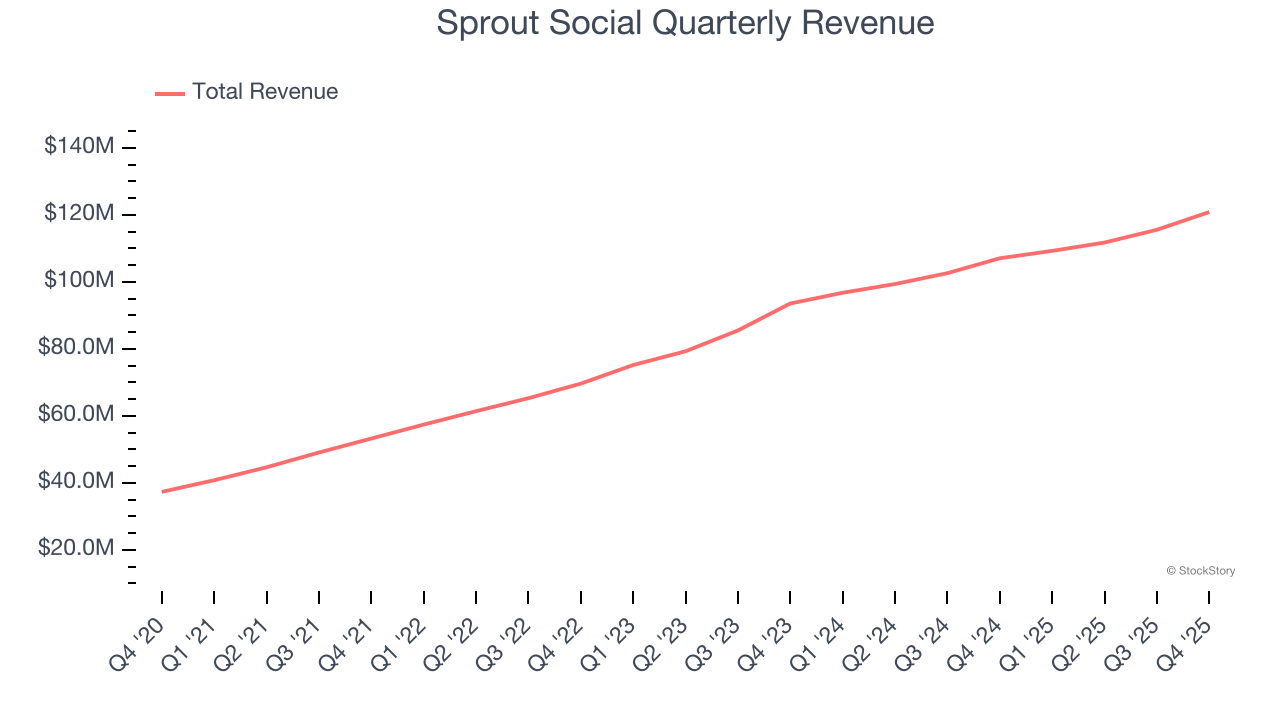

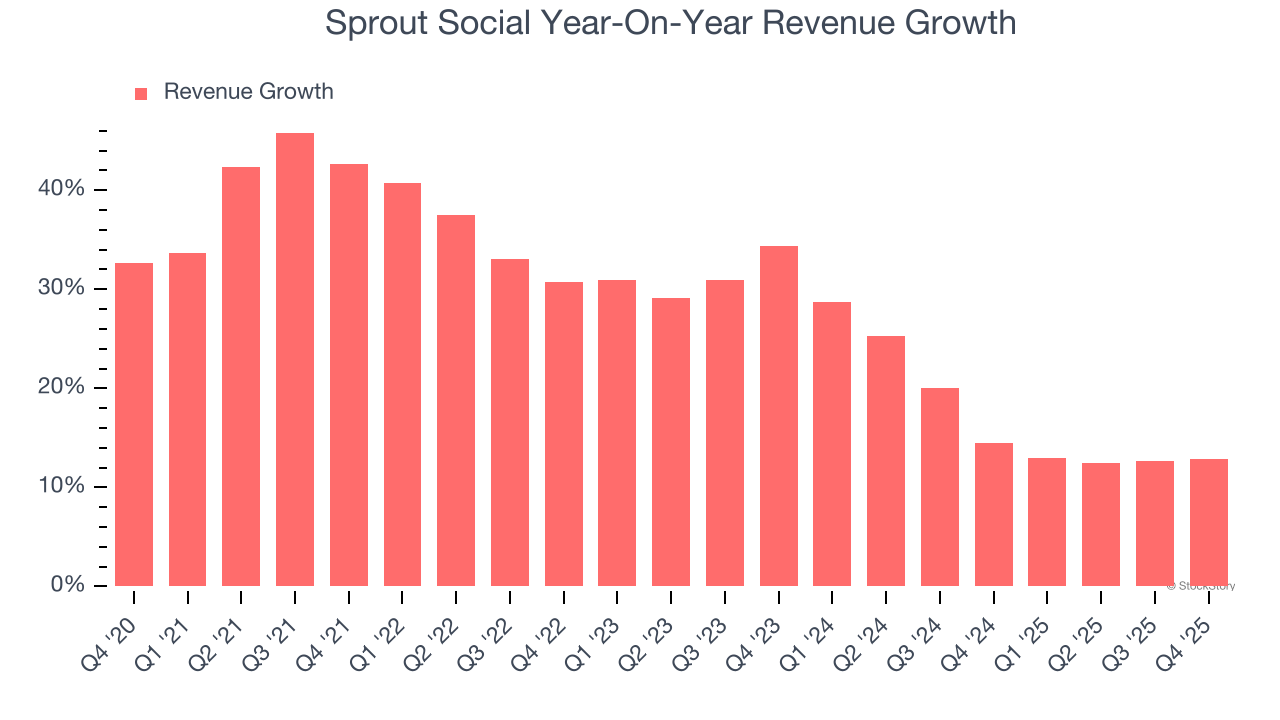

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Sprout Social grew its sales at an impressive 28% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Sprout Social’s annualized revenue growth of 17.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Sprout Social reported year-on-year revenue growth of 12.9%, and its $120.9 million of revenue exceeded Wall Street’s estimates by 1.8%. Company management is currently guiding for a 10.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking.

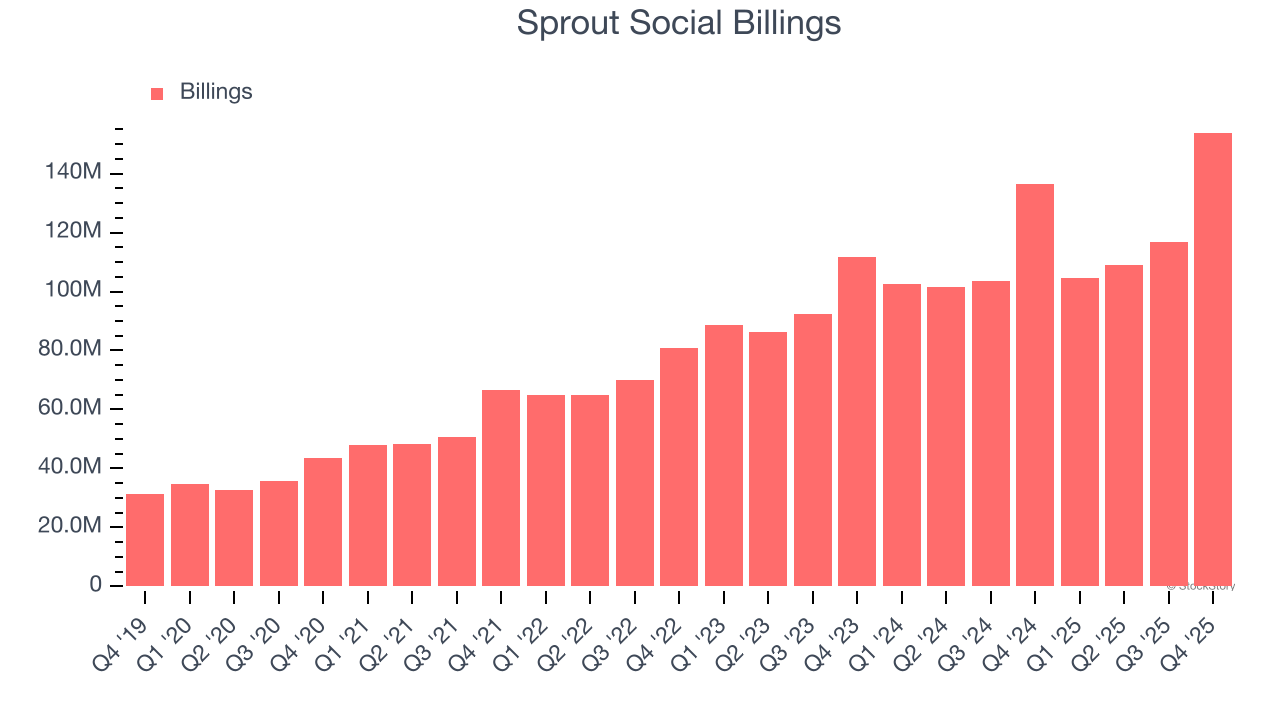

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Sprout Social’s billings came in at $153.9 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 8.7% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

Key Takeaways from Sprout Social’s Q4 Results

It was great to see Sprout Social’s full-year EPS guidance top analysts’ expectations. We were also glad its billings outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.7% to $7.01 immediately after reporting.

Sprout Social underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Ripple Prime Executive Confirms: XRP Is Being Used As Collateral Right Now

EU lawmakers urge assessing DeFi, staking, NFT regulation

US Spot Ethereum ETFs Extend Outflow Streak to Seven Days as BlackRock’s ETHA Leads Losses

Why July 2’s RBI Meeting Could Define India’s Crypto Path?