Danaher (DHR) Has Fallen 4.7% Since Its Last Earnings Release: Is a Recovery Possible?

Danaher (DHR) Stock Performance and Recent Earnings Overview

Since the previous earnings announcement roughly a month ago, Danaher’s share price has declined by approximately 4.7%, lagging behind the S&P 500’s performance during the same period.

Investors are now questioning whether this downward movement will persist ahead of the next earnings report, or if a positive reversal is on the horizon. To better understand the current situation, let’s review the company’s most recent financial results and the factors influencing its performance.

Fourth Quarter 2025 Results: Earnings and Revenue Highlights

For the fourth quarter of 2025, Danaher posted adjusted earnings of $2.23 per share, slightly surpassing the consensus estimate of $2.22 and marking a 4% increase year over year. The company’s net sales reached $6.84 billion, exceeding expectations of $6.79 billion and reflecting a 4.5% annual growth, with all business segments contributing positively.

Core sales advanced by 2.5% compared to the prior year. Foreign currency movements added 2.5% to results, while acquisitions and divestitures reduced sales by 0.5%. For the full year, Danaher reported $24.6 billion in revenue, up 3% year over year, and adjusted earnings of $7.80 per share, a 4.5% improvement.

Segment Performance Breakdown

- Life Sciences: Revenue reached $2.09 billion, a 2.5% increase over the previous year and above the expected $2.06 billion. Core sales edged up 0.5%, with foreign exchange adding 2%. Operating profit for the segment was $336 million, down from $376 million a year earlier.

- Diagnostics: This segment generated $2.72 billion in revenue, up 3% year over year and slightly ahead of the $2.71 billion consensus. Core sales rose 2%, with currency effects adding another 2%, while acquisitions and divestitures reduced sales by 1%. Operating profit climbed 14.3% to $713 million.

- Biotechnology: Revenue totaled $2.03 billion, a 9% increase from the prior year and above the $2.02 billion estimate. Core sales grew 6%, and foreign exchange contributed 3%. Operating profit increased 6.3% to $540 million.

Profitability and Expense Overview

During the fourth quarter, Danaher’s cost of sales rose 8.5% to $2.87 billion, while gross profit improved 2% to $3.97 billion. The gross margin was 59.1%, slightly lower than the 59.5% margin from the previous year.

Selling, general, and administrative expenses were $2.03 billion, nearly unchanged from the prior year. Research and development spending decreased by 0.9% to $438 million. Operating profit increased 5.4% to $1.50 billion, though the operating margin declined to 19.1% from 20.4% a year earlier.

Financial Position and Cash Flow

At the end of the fourth quarter, Danaher held $4.62 billion in cash and equivalents, up from $2.08 billion at the end of 2024. Long-term debt stood at $18.4 billion, compared to $15.5 billion previously.

For 2025, the company generated $6.42 billion in operating cash flow, down from $6.69 billion the year before. Capital expenditures were $1.16 billion, a 17% decrease year over year. Adjusted free cash flow was $5.3 billion, a slight 0.3% decline. Dividend payments totaled $878 million, up 14.3% from the prior year.

Guidance for 2026

Looking ahead to the first quarter of 2026, Danaher anticipates adjusted core sales from ongoing operations will grow in the low single digits year over year. For the full year, the company expects core sales to rise between 3% and 6%, with adjusted earnings projected in the range of $8.35 to $8.50 per share.

Recent Estimate Trends

Over the past month, analyst estimates for Danaher have generally moved lower, reflecting a more cautious outlook for the company’s near-term performance.

VGM Score Analysis

Danaher currently holds a D rating for Growth, Momentum, and Value, placing it in the lower 40% among value-focused investors. The overall VGM Score is also a D, which may be most relevant for those not following a specific investment strategy.

Stock Outlook

Analyst revisions have largely trended downward, indicating a less optimistic view for the stock. Danaher is assigned a Zacks Rank #3 (Hold), suggesting that the stock is expected to deliver returns in line with the market over the coming months.

Industry Comparison: HCA Healthcare

Within the Zacks Medical Services sector, HCA Healthcare (HCA) has gained 9% over the past month. The company’s most recent quarterly report showed revenues of $19.51 billion, a 6.7% year-over-year increase, and earnings per share of $8.01, up from $6.22 a year earlier.

For the current quarter, HCA is projected to earn $7.18 per share, an 11.3% increase from the same period last year. The consensus estimate has risen by 1.7% over the past 30 days. HCA holds a Zacks Rank #3 (Hold) and boasts a VGM Score of A.

Top Stock Picks from Zacks Research

The Zacks research team has identified five stocks with strong potential to double in value in the coming months. Among these, the Director of Research, Sheraz Mian, highlights a lesser-known satellite communications company poised for significant growth as the space industry expands. Analysts are forecasting a major revenue surge for this firm in 2025. While not all top picks achieve outsized gains, this one could outperform previous winners such as Hims & Hers Health, which soared over 200%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

BlackRock's Ethereum ETF includes Galaxy in staking.

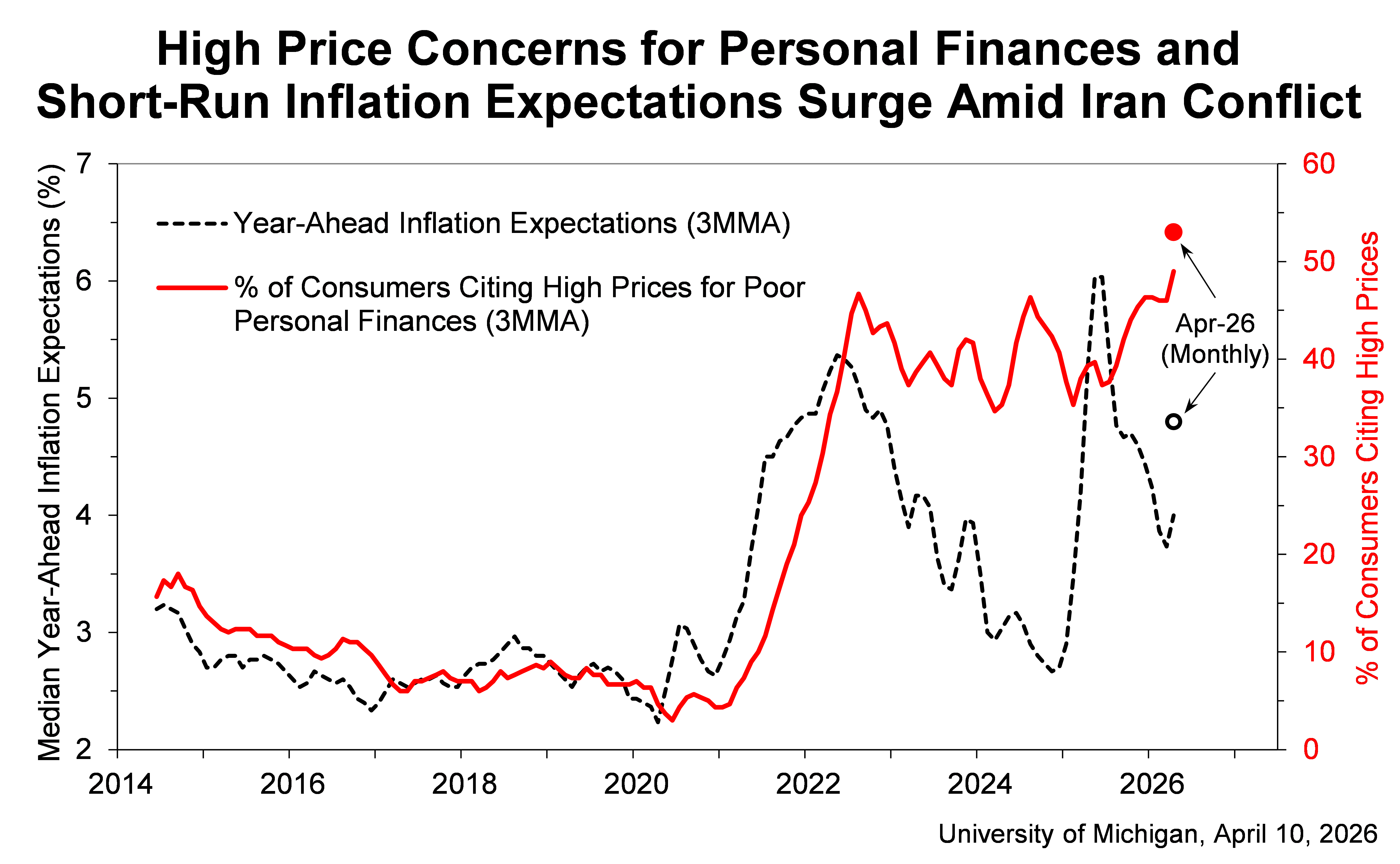

Spot gold at session highs after Consumer Sentiment falls to 47.6, one-year inflation expectations shoot to 4.8%

Improve Your Retirement Earnings with These Three Highly Rated Dividend Stocks

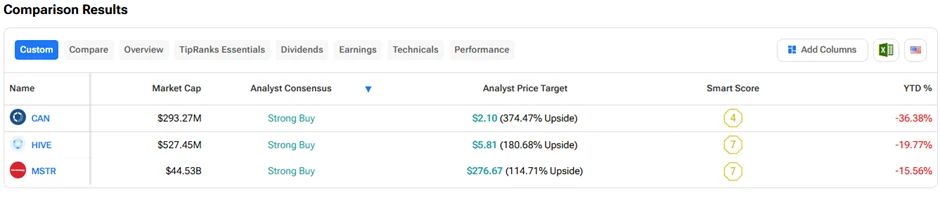

3 ‘Strong Buy’ Crypto Stocks with Over 100% Upside Potential, 4/10/26