3 Key Motives to Offload VMC and One Alternative Stock Worth Purchasing

Vulcan Materials: Recent Performance and Investment Outlook

Since September 2025, Vulcan Materials' stock has remained relatively flat, delivering a modest 3.1% return and hovering near $301.49 per share.

Is this a good moment to invest in Vulcan Materials, or should you approach with caution before adding it to your portfolio?

Why We're Not Enthusiastic About Vulcan Materials

At this time, we’re choosing to stay on the sidelines. Here are three reasons we’re avoiding VMC, along with a stock we prefer instead.

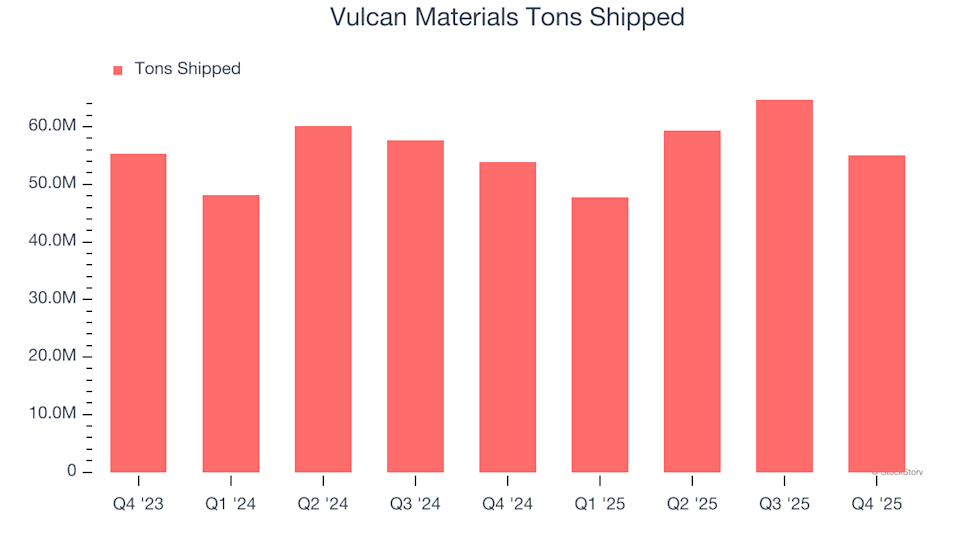

1. Sluggish Growth in Tons Shipped Signals Weak Demand

For companies like Vulcan Materials, revenue is influenced by both pricing and the volume of goods sold, with tons shipped being a key metric. While both factors matter, volume growth is especially important since price increases have their limits.

In the most recent quarter, Vulcan Materials shipped 55.1 million tons. Over the past two years, the company’s year-over-year growth in tons shipped averaged just 2%. This slow pace suggests Vulcan may need to cut prices or enhance its products to boost growth—moves that could pressure short-term profits.

Vulcan Materials Tons Shipped

2. Revenue Growth Forecasts Remain Tepid

Wall Street’s revenue projections offer a glimpse into a company’s future potential. While forecasts aren’t always spot-on, accelerating growth tends to lift valuations and share prices, whereas slowing growth can have the opposite effect.

Analysts expect Vulcan Materials’ revenue to increase by just 1.2% over the next year, which is not much higher than its 10.3% annualized growth rate over the past five years. This outlook doesn’t inspire confidence and suggests that new products and services aren’t likely to drive significant top-line growth in the near term.

3. Narrow Gross Margins Limit Profitability

We favor companies with strong gross margins, as these typically reflect pricing power or unique offerings that can lead to higher operating profits.

Vulcan Materials’ financials reveal challenging unit economics for an industrial firm. Over the last five years, its average gross margin was just 25.2%, meaning the company spent $74.82 on suppliers for every $100 in revenue. This leaves less capital to reinvest in innovation and expansion.

Vulcan Materials Trailing 12-Month Gross Margin

Our Verdict

While Vulcan Materials is not a poor-quality business, it doesn’t meet our standards for investment. Currently, the stock trades at 32.9 times forward earnings (about $301.49 per share). Investors willing to take on more risk might find it appealing, but we believe the downside risk outweighs the potential rewards. We’re confident there are stronger opportunities available.

Alternative Stocks to Consider

DISCOVER: 9 Top-Performing Stocks. The most successful stocks consistently outperform the market, fueled by robust revenue growth, increasing free cash flow, and exceptional returns on capital. These companies have already been recognized by the market for their achievements.

But according to our AI platform, the momentum isn’t over yet. See which 9 stocks made our list this week—absolutely free.

Our selections feature well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Exlservice, which delivered a 354% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin, Ethereum and XRP Rally: Why is Crypto Market Going Up Today?

Distillate Shortage Shifts Advantage to Energy Sector Instead of Automotive Industry

XRP Price Prediction Eyes $1.50 in March While BNB Holds and Pepeto Presale Crosses $7.4M With 209% APY Staking