3 Key Reasons to Consider Selling VMC and One Alternative Stock Worth Buying

Vulcan Materials: Recent Performance Overview

Since September 2025, Vulcan Materials' stock has remained relatively flat, delivering a modest 3.1% return and hovering near $301.49 per share.

Is this a good moment to invest in Vulcan Materials, or should you approach with caution?

Why We’re Not Enthusiastic About Vulcan Materials

At this time, we’re choosing to stay on the sidelines. Here are three reasons we’re not adding VMC to our portfolio, along with an alternative stock we prefer.

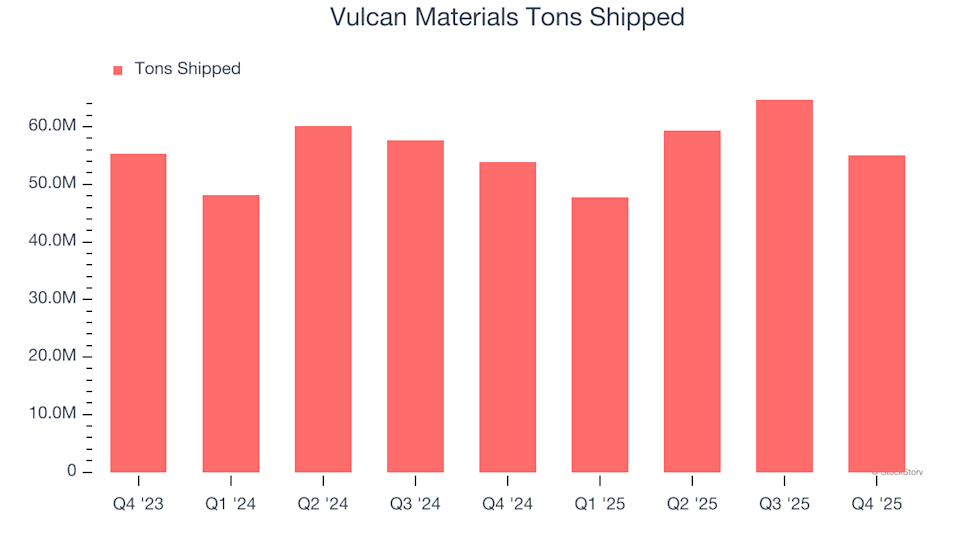

1. Sluggish Volume Growth Signals Weak Demand

When evaluating revenue growth, both pricing and sales volume matter. For Vulcan Materials, the key metric is tons shipped. While price increases have limits, volume growth is crucial for long-term success.

In the most recent quarter, Vulcan Materials shipped 55.1 million tons, with an average annual growth rate of just 2% over the past two years. This lackluster performance suggests the company may need to cut prices or enhance its products to boost growth—steps that could pressure short-term profits.

Vulcan Materials Tons Shipped

2. Limited Revenue Growth Expected

Analyst forecasts provide a glimpse into a company’s future prospects. While predictions aren’t always perfect, accelerating growth tends to lift valuations and share prices, whereas slowing growth can have the opposite effect.

Wall Street expects Vulcan Materials’ revenue to increase by just 1.2% over the next year, which is not much higher than its 10.3% annualized growth over the past five years. This outlook suggests that new products and services are unlikely to drive significant top-line growth in the near term.

3. Margins Indicate Structural Profitability Challenges

We favor companies with strong gross margins, as these often reflect pricing power or unique offerings that can support higher profits.

Vulcan Materials, however, has struggled with profitability. Over the past five years, its average gross margin was only 25.2%, meaning the company spent $74.82 on suppliers for every $100 in revenue. This leaves less capital to reinvest in innovation or expansion.

Vulcan Materials Trailing 12-Month Gross Margin

Our Verdict

While Vulcan Materials is not a poor business, it doesn’t meet our standards for quality. The stock currently trades at a forward P/E of 32.9 (about $301.49 per share). Investors willing to take on more risk might find it appealing, but we believe there are better opportunities elsewhere. For those seeking alternatives, we recommend considering our top semiconductor pick.

Stocks We Prefer Over Vulcan Materials

WHILE YOU’RE HERE: Discover 9 Top-Performing Stocks. The best companies consistently outperform the market, boasting strong revenue growth, increasing free cash flow, and impressive returns on capital. These businesses have already been rewarded by investors.

But according to our AI platform, the momentum isn’t over. See which 9 stocks made our list this week—completely free.

Our selections include well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years. Start your search for the next big winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

TREE Lags Q4 Earnings Estimates, Stock Up 23.9% on Revenue Growth

Stryker Unveils Next-Gen Orthopedic Innovations at AAOS 2026

FN Jumps 25% in a Month: Is There More Room for the Stock to Grow?

Ireland’s Treasury Moves Into Deficit, Sparking Worries Over Public Finances