Is Lemonade, Inc. (LMND) A Good Stock To Buy Now?

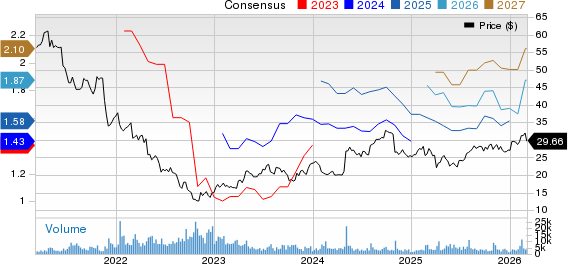

We came across a on Lemonade, Inc. on Danny’s Substack by Danny Green. In this article, we will summarize the bulls’ thesis on LMND. Lemonade, Inc.'s share was trading at $51.74 as of February 27th.

Lemonade, Inc. (LMND) is emerging as a leading tech-driven insurtech, leveraging AI and digital transformation to streamline underwriting, claims processing, and customer onboarding. The company has seen strong growth in in-force premiums, with Q3 2025 revenue up ~42% YoY and IFP exceeding $1.16 billion, signaling market acceptance of its digital insurance solutions. AI adoption has enhanced operational efficiency, improved gross profit, and lowered loss ratios, yet net profitability remains elusive, with losses persisting despite narrowing negative EBITDA.

Lemonade’s competitive edge lies in its AI-driven stack and proprietary data, which create unit economics advantages, cost efficiencies, and customer stickiness. However, legacy insurers with deep capital and distribution networks, along with tightening regulations on AI and data use, temper the durability of this emerging moat. Management has prioritized aggressive growth, expanding into car insurance and European markets, while strategically reducing reinsurance cessions to improve margins, though high customer acquisition costs and continued negative cash flow demand disciplined capital allocation.

Key risks include sustained unprofitability, regulatory constraints, and competitive pressures from both incumbents and emerging startups, any of which could materially impact valuation and growth trajectory. The upside, however, is significant: successful scaling of car insurance, cross-selling across products, and AI-driven efficiency gains could enhance margins and customer lifetime value.

Catalysts such as achieving adjusted EBITDA breakeven or positive free cash flow in 2026, combined with rapid U.S. and European expansion and improved loss ratios, could drive rerating. Valuation reflects growth expectations more than current earnings, making LMND suitable for tactical exposure with high-risk tolerance, while setbacks in profitability or regulation remain key downside triggers.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Philips Unveils Rembra CT Scanner to Speed Up Medical Imaging

UVIX Jumps 13% As VIX Nears 'Fear Zone' Of 30, Volatility ETFs Surge

Boeing close to 500-Jet Order with Trump-Xi Summit, Bloomberg News reports