ChargePoint (CHPT): Should You Buy, Sell, or Hold After Q4 Results?

ChargePoint's Challenging Half-Year

ChargePoint has experienced a tough six months, with its share price plummeting by 48.3% to $5.42. This sharp decline has unsettled many investors, prompting questions about whether now is the right moment to invest or if caution is warranted.

Should you consider adding ChargePoint to your portfolio, or is it better to stay on the sidelines?

Why We’re Not Enthusiastic About ChargePoint

Although the current price may seem attractive, we’re choosing not to invest in ChargePoint at this time. Below are three reasons for our hesitation, along with a stock we prefer.

1. Declining Revenue

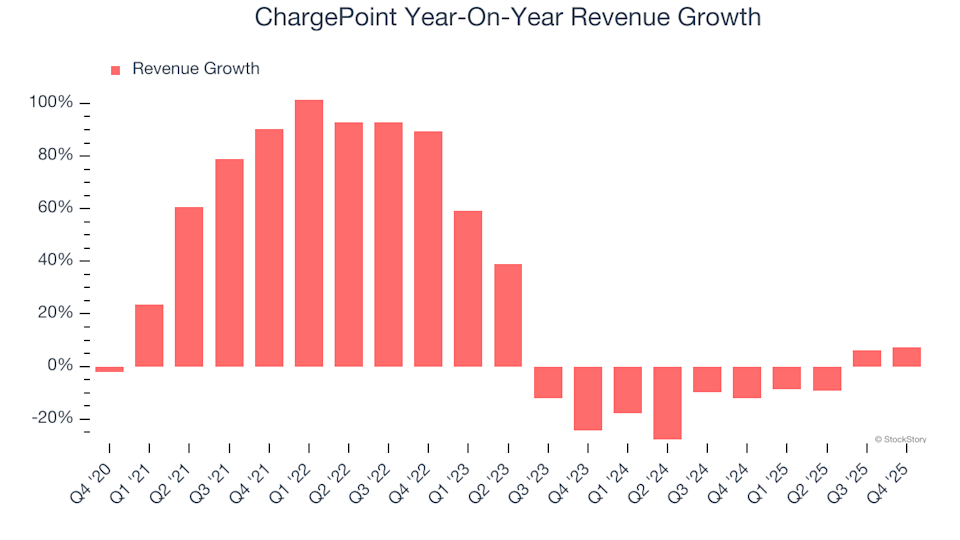

While long-term growth is crucial, focusing solely on historical performance can overlook emerging trends and shifts in demand. ChargePoint’s recent results show a significant departure from its five-year trajectory, with annual revenue decreasing by 9.9% on average over the past two years.

2. Heavy Cash Outflows Raise Red Flags

Free cash flow is often overlooked in financial reports, but it provides a clear picture of a company’s financial health by factoring in all operational and capital expenses. In this regard, ChargePoint’s substantial reinvestments over the last five years have severely depleted its cash reserves, restricting its ability to reward shareholders. The company’s average free cash flow margin stands at negative 50.5%, meaning it burned $50.53 for every $100 earned in revenue.

3. Limited Access to Funding Heightens Risk

Debt can enhance returns but also introduces significant risk if mismanaged. As investors with a long-term perspective, we avoid companies that rely too heavily on borrowing, as this can lead to financial distress. ChargePoint reported a negative EBITDA of $82.7 million over the past year, and its debt of $260.9 million far outweighs its cash holdings of $142 million. This imbalance is a major concern, as companies losing money and carrying substantial debt are especially vulnerable.

Investors should proceed with caution. If ChargePoint continues to operate at a loss, credit agencies may downgrade its rating, making future borrowing more expensive and further limiting growth opportunities. The company could face serious challenges if market conditions deteriorate. We hope ChargePoint can turn its profitability around, but for now, we remain wary.

Our Verdict

ChargePoint isn’t fundamentally flawed, but it doesn’t meet our investment criteria. Following its recent decline, the stock is priced at $5.42 per share, with a forward price-to-sales ratio of 0.3. The market values ChargePoint based on expected profits over the next year, but forecasts suggest continued losses. Given the limited upside and considerable risk, we believe there are better investment opportunities. Consider exploring one of Charlie Munger’s favorite companies instead.

Alternative Stocks Worth Considering

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The ideal time to invest in a standout stock is when the market begins to recognize its potential. These companies not only possess strong fundamentals but are also experiencing positive momentum right now.

Discover which stocks our AI platform is highlighting this week. Access the list of Strong Momentum stocks—completely free.

Our selections include well-known names like Nvidia, which soared by 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Kadant, which achieved a 351% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

NZ Current Account Deficit Surpasses 16 Billion, Red Flags Rise

Rimini Street at ROTH: An Unlikely Event to Monitor Ahead of Earnings

Is Editas Medicine Headed Toward Zero?

Amphenol (APH): 3 Key Factors That Make This Stock Appealing