3 Reasons to Steer Clear of OCUL and One Alternative Stock Worth Buying

Ocular Therapeutix: Recent Performance and Investment Outlook

Over the last half year, Ocular Therapeutix shareholders have faced significant losses, with the stock price falling by 29.1% to $8.62. This decline has been influenced by weaker-than-expected quarterly results, leaving investors uncertain about the best course of action.

Is Ocular Therapeutix a potential bargain, or does it pose too much risk for your portfolio?

Why We Believe Ocular Therapeutix May Underperform

Even with its lower share price, we remain cautious about Ocular Therapeutix. Here are three key reasons why we see more attractive alternatives to OCUL in the market.

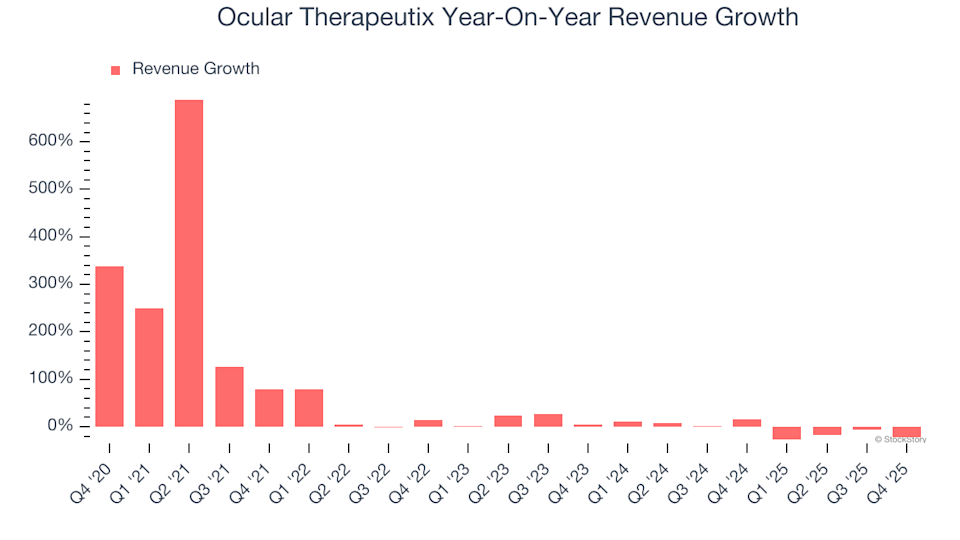

1. Declining Revenue

While long-term growth is crucial, especially in the healthcare sector, recent results can reveal important shifts. Ocular Therapeutix has experienced a notable reversal from its previous five-year trajectory, with revenues decreasing at an average annual rate of 5.7% over the past two years.

Ocular Therapeutix Year-On-Year Revenue Growth

2. Worsening Adjusted Operating Margin

The adjusted operating margin is a vital indicator of a company’s profitability, reflecting the portion of revenue remaining after covering core expenses such as production, marketing, and salaries. It also allows for fair comparisons across companies by excluding one-time costs, interest, and taxes.

Ocular Therapeutix has seen its adjusted operating margin deteriorate sharply over the last five years. This trend is concerning, as revenue growth should typically help offset fixed costs and improve profitability. Instead, the company’s costs have risen faster than its ability to generate revenue, resulting in a trailing 12-month adjusted operating margin of negative 520%.

Ocular Therapeutix Trailing 12-Month Operating Margin (Non-GAAP)

3. Falling Free Cash Flow Margin

Although free cash flow is often overlooked in financial reports, it provides a clear picture of a company’s ability to generate cash after all expenses and investments. In this case, Ocular Therapeutix’s free cash flow margin has dropped significantly over the past five years. Any further decline is troubling, as the company is already operating at a cash deficit. If this pattern persists, it may indicate a period of heavy investment. For the last 12 months, the free cash flow margin stood at negative 417%.

Ocular Therapeutix Trailing 12-Month Free Cash Flow Margin

Our Verdict

While we appreciate companies that contribute to better health outcomes, we do not see a compelling case for investing in Ocular Therapeutix at this time. The stock is currently priced at $8.62 per share, with a forward price-to-sales ratio of 35.1×. The market is projecting continued losses for the company in the coming year, and we believe the potential rewards do not outweigh the risks. There are more promising opportunities elsewhere. Consider exploring our top picks in software and edge computing.

Alternative Stocks to Consider

WHILE YOU’RE HERE: Discover the Top 9 Market-Beating Stocks. The most successful stocks consistently outperform the market, boasting strong revenue growth, increasing free cash flow, and exceptional returns on capital. These companies have already been recognized by the market for their achievements.

Our AI-driven platform suggests that the momentum for these stocks is far from over. See which nine companies made our list this week — absolutely free.

Our selections include well-known leaders like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known success stories such as Exlservice, which delivered a 354% return over five years. Start your search for the next standout stock with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

GBP/USD steadies ahead of back-to-back Fed and BoE decisions

Bhutan Government is Selling Its Bitcoin Again Despite Price Recovery

Viewpoint: Strategy Financing Models Shift, Preferred Stock Becomes the Main Force for Bitcoin Purchases