3 Reasons to Steer Clear of LAUR and 1 Alternative Stock Worth Buying

Laureate Education: Outperforming the Market, But Is It Worth Buying?

Since March 2021, the S&P 500 has returned 66.7%. However, Laureate Education has far surpassed this benchmark, climbing 139% over the past five years to reach $33.96 per share. The company’s strong quarterly performance has continued to drive its momentum, with shares rising 14.3% in the last half-year—outpacing the S&P by 13.8%.

Should investors consider adding Laureate Education to their portfolios now, or is caution warranted?

Why We Believe Laureate Education May Not Perform Well

Despite its recent gains, we’re choosing not to invest in Laureate Education at this time. Here are three reasons we’re steering clear—and a stock we prefer instead.

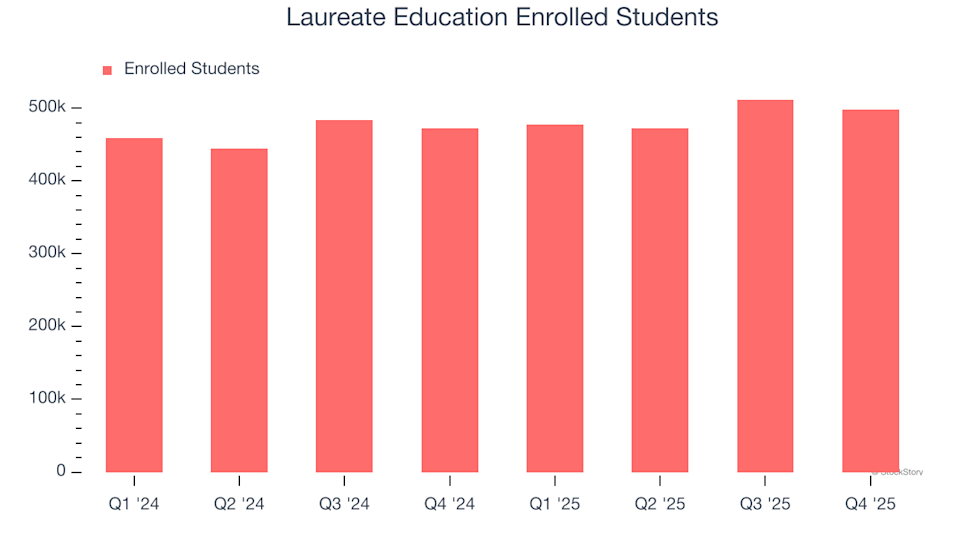

1. Modest Growth in Student Enrollment Signals Weak Demand

Revenue increases can result from higher prices or greater volume. For Laureate Education, the key volume metric is student enrollment. While both factors matter, enrollment is crucial since price hikes have their limits.

In the latest quarter, Laureate Education reported 497,700 enrolled students, with average annual growth of 5.3% over the past two years. This sluggish pace suggests the company may need to cut prices or invest in enhancing its offerings to boost growth—moves that could impact short-term profits.

2. Declining Earnings Per Share

Tracking earnings per share (EPS) over time reveals whether increased sales are translating into real profits. Sometimes, revenue growth is driven by heavy spending on marketing, which doesn’t always improve profitability.

Unfortunately, Laureate Education’s EPS has dropped by 14% annually over the past five years, even as revenue grew by 10.7%. This indicates that the company’s expansion has not resulted in higher earnings per share.

3. Unimpressive Free Cash Flow Outlook

At StockStory, we prioritize free cash flow because it’s essential for covering expenses—unlike accounting profits. Analysts expect Laureate Education’s free cash flow margin, currently at 15.5% for the past year, to remain unchanged over the next twelve months.

Our Verdict

We support companies that serve everyday consumers, but when it comes to Laureate Education, we’re staying on the sidelines. Although its stock has outperformed recently and trades at a reasonable 16.2× forward P/E (or $33.96 per share), our confidence in the company is limited. There are more promising investment opportunities available right now. Consider exploring our top semiconductor picks.

Better Alternatives to Laureate Education

Top 9 Market-Beating Stocks: The best-performing stocks consistently outpace the market, boasting strong revenue growth, increasing free cash flow, and impressive returns on capital. These companies have already been recognized by investors.

Our AI-driven platform suggests that these winning streaks are far from over. Discover which nine stocks made our list this week—absolutely free.

Our selections feature well-known names like Nvidia, which soared 1,326% between June 2020 and June 2025, as well as lesser-known companies such as Exlservice, which delivered a 354% five-year return. Find your next standout investment with StockStory.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

GBP/USD steadies ahead of back-to-back Fed and BoE decisions

Bhutan Government is Selling Its Bitcoin Again Despite Price Recovery

Viewpoint: Strategy Financing Models Shift, Preferred Stock Becomes the Main Force for Bitcoin Purchases