Memory Supercycle Isn’t Over: 50% Upside Still Ahead?

As markets recover from the volatility triggered by Middle East tensions, Micron TechnologyMU+4.50% has reached another all-time high. The key question for investors now is: can the red-hot memory trade continue?

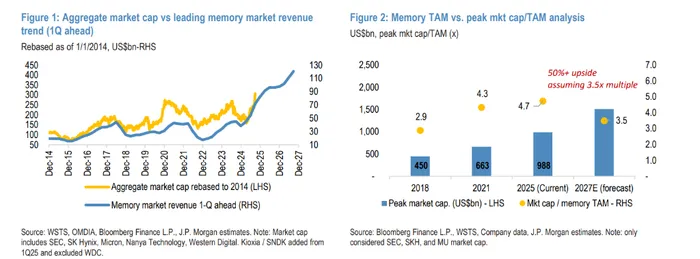

According to J.P. Morgan’s latest research, the combined market capitalization of leading memory chip manufacturers has approached $1 trillion. Based on historical valuation benchmarks, this figure could surge to $1.5 trillion by 2027, implying more than 50% upside from current levels.

The firm argues that the current cycle is likely to become the longest and strongest upcycle in memory industry history.

Cautious Capacity Expansion: DRAM Shortage Likely Through 2027

There is little doubt that the market is in the midst of a memory supercycle. However, investors remain concerned that aggressive capacity expansion by major players—Samsung Electronics, SK Hynix, and Micron—could eventually trigger another oversupply cycle.

Yet, following the painful oversupply triggered by the COVID-19 period in 2020, both Samsung and SK Hynix have become significantly more disciplined.

Samsung is reportedly adopting a more cautious approach to DRAM expansion, internally expecting the current shortage to ease only around 2028, and calibrating investment accordingly to avoid overexpansion. Senior management believes this memory supercycle could extend through 2028.

Similarly, SK Hynix has repeatedly emphasized that future capacity expansion will be guided by actual demand rather than optimistic forecasts.

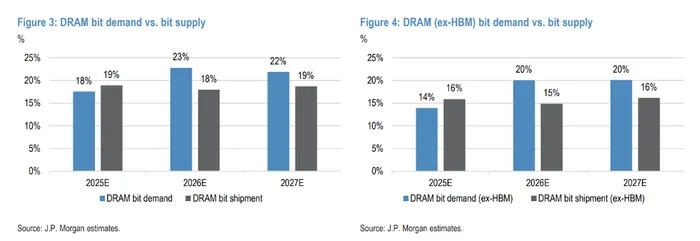

J.P. Morgan also believes that the supply shortage is unlikely to be resolved in the near term. Strong demand from cloud service providers (CSPs) is forcing manufacturers to allocate more capacity to HBM (High Bandwidth Memory).

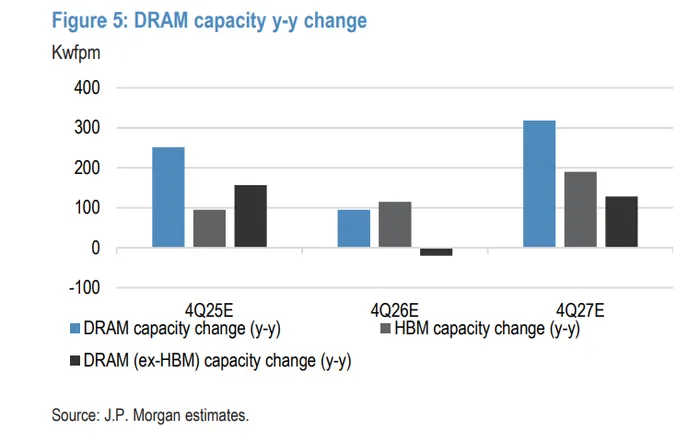

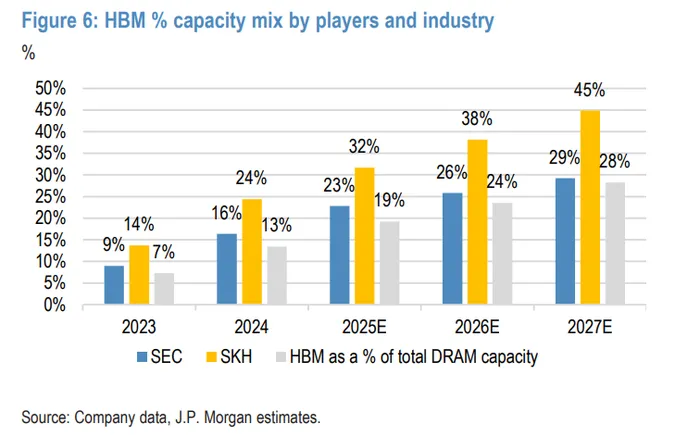

HBM’s share of total DRAM capacity is expected to rise sharply from 19% in 2025 to 28% in 2027. As a result, conventional DRAM capacity is effectively tightening. In fact, DRAM capacity is expected to decline year-over-year in 2026.

Even with new capacity coming online—such as Samsung’s P4 and SK Hynix’s M15X—constraints including cleanroom limitations and increased process complexity will cap bit shipment growth at below 20%.

Where Are the Biggest Opportunities?

J.P. Morgan’s model suggests a significant increase in memory pricing:

DRAM ASP is expected to rise by 53%; NAND ASP is expected to increase by around 30%.

Looking ahead to fiscal year 2027: DRAM ASP is expected to edge up by 1%, even at elevated levels; NAND ASP may decline modestly by 6%.

The bank also expects clear price divergence from the second half of 2026 to the first half of 2027:

B2B segment (AI-driven): Prices remain resilient, supported by AI inference demand.

B2C segment (consumer): Prices face cyclical pressure due to resistance to high pricing.

HBM Demand Keeps Tightening Supply

While the debate between GPUs and ASICs remains unresolved, both architectures require HBM.

J.P. Morgan expects Google’s next-generation 2nm TPU to adopt HBM4, while Nvidia’s Rubin Pro GPU could deliver 4x memory capacity increases, further tightening supply.

HBM is expected to remain in structural shortage, with a supply-demand gap of 8%–12% through 2027, potentially extending into 2028.

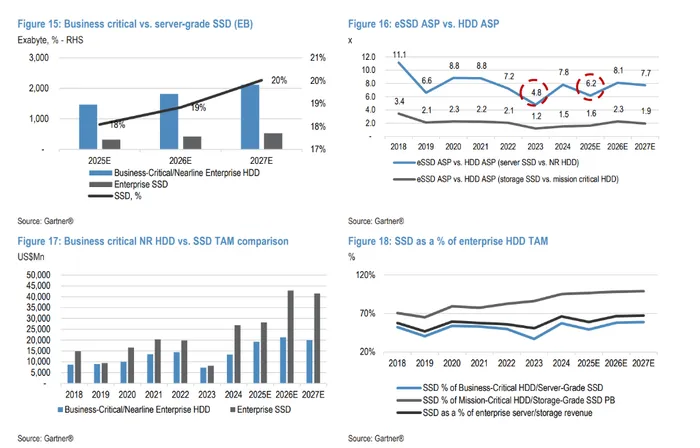

SSD: A Key Beneficiary of AI Inference

The rise of AI inference is driving rapid expansion in the enterprise SSD (eSSD) market.

AI servers typically require three times more SSD capacity than traditional servers, significantly boosting demand.

Meanwhile, HDD manufacturers have issued conservative capex guidance for 2026, limiting supply-side response.

As a result, J.P. Morgan expects eSSD to enjoy strong demand tailwinds over the next six months, supporting a 27% increase in NAND prices in 2026.

When Does the Cycle Peak? UBS Points to One Key Indicator

Every cycle eventually peaks—but how can investors identify the turning point?

UBS reviewed two decades of memory cycles and reassessed leading indicators. The bank argues that AI has fundamentally changed the industry’s underlying dynamics, making traditional valuation and pricing indicators less reliable.

Instead, operating profit has emerged as a more effective leading indicator.

Historically, investors relied on the rate of acceleration in ASP growth (quarter-over-quarter or year-over-year) to identify stock price peaks. However, UBS finds that this indicator has become unreliable—only 10 out of the last 20 peaks were correctly signaled, effectively no better than chance.

By contrast, operating profit has shown much stronger predictive power: In 90% of cases, stock prices peaked alongside or ahead of operating profit.

Typically, stock prices peak one quarter before earnings peak, UBS expects the memory industry’s operating profit to peak in Q3 2027.

All else equal, this implies that memory stocks could continue rallying through Q2 2027. UBS forecasts that Samsung, SK Hynix, and MicronMU+4.50% will generate an average ROE of 36% between 2026 and 2030, significantly higher than the 15% average over the past decade.

Key Risk: Profit Timing May Be Harder to Predict

UBS cautions that forecasting the exact timing of profit peaks remains challenging.

The structural shift driven by AI—particularly the reallocation of capacity toward HBM—complicates the relationship between pricing, supply, and profitability.

As HBM continues to crowd out conventional DRAM capacity, the timing of peak earnings may shift rapidly, making traditional cycle timing strategies less reliable.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

UK committee pushes for crypto donation ban over foreign influence risks

X's Bot Purge: How Crypto Scams Face a Liquidity Shakeup

Top 2 Industrial Stocks of the Decade for Long-Term Investment

Top Crypto Coins After Nvidia’s $1T AI Prediction: Polygon, Hedera, and APEMARS Stage 12 in Focus