Oshkosh’s Reputation for Ethics Is Challenged as Access Division Falters—Will Company Values Bridge Performance Shortfalls?

Oshkosh Corporation: A Decade of Ethical Leadership

Oshkosh Corporation has established itself as a leader in ethical business practices, consistently earning recognition from Ethisphere as one of the World's Most Ethical Companies for ten consecutive years, including in 2025. In addition, the company was awarded the 2026 EcoVadis Silver Medal, placing it among the top 15% of companies worldwide for responsible business conduct. This ongoing achievement is not a one-time honor but the result of a decade-long commitment to rigorous standards, with over 240 criteria covering governance, compliance, and social responsibility.

Central to Oshkosh’s approach is the “Oshkosh Way,” a set of guiding principles that influence every level of the organization—from leadership to manufacturing. These values emphasize putting people first, acting with integrity, perseverance, and collaboration. Far from being empty slogans, these principles shape the company’s culture and extend to its suppliers through a strict code of conduct. For investors, the key question is whether this deeply rooted culture provides a lasting competitive edge, especially during economic downturns.

There is evidence to support this idea. According to Ethisphere, companies recognized for their ethical standards outperformed a comparable group of large-cap firms by 7.8% between 2020 and 2025—a phenomenon known as the “Ethics Premium.” For Oshkosh, this reputation acts as a protective moat. In challenging times, a history of ethical conduct can foster stronger customer loyalty, more dependable supplier relationships, and a stable workforce—advantages that are difficult to replicate and easy to lose. Ultimately, trust built over time can deliver lasting value well beyond periods of prosperity.

Segment Performance: Strengths and Weaknesses Revealed

While Oshkosh’s ethical culture is a significant asset, its impact varies across the company’s different business segments. Recent financial results highlight a clear divide: some areas are thriving, while others are facing serious challenges, affecting overall profitability.

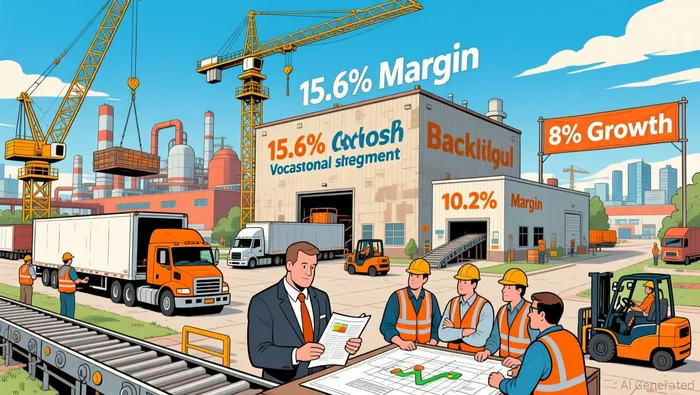

The Vocational segment stands out for its resilience and growth. With a robust $6.4 billion backlog—an 8% increase year-over-year—this segment enjoys strong visibility into future sales and cash flow. This confidence is reflected in its performance: Vocational sales rose 18.9% year-over-year, and the adjusted operating margin improved to 15.6%, up 190 basis points. Such results demonstrate the tangible benefits of a culture built on reliability and ethical conduct, strengthening relationships with customers and suppliers.

In contrast, the Access segment is experiencing significant difficulties. Revenue dropped 18.6% year-over-year to $1.1 billion, and the backlog shrank by 66%—a dramatic shift in demand, especially for products like telehandlers. This steep decline has weighed heavily on the company’s overall financial health, reducing the adjusted operating margin to 10.2%.

The Transport segment, which includes the large-scale NGDV program, adds further complexity. Although the segment has seen some growth, the NGDV program now makes up 25% of Transport’s revenue but comes with lower margins and high upfront costs typical of government contracts. This mix is putting additional pressure on profitability, even as the segment expands.

In summary, Oshkosh’s ethical foundation is bolstering its strongest divisions, but it cannot immediately resolve the challenges facing weaker segments. The company’s financial outlook now depends on whether the Access segment can recover and whether margin pressures from NGDV and Access can be alleviated.

Financial Overview: Navigating a Challenging Year

Oshkosh’s recent financial results reflect a company facing headwinds. In 2025, revenue reached $10.42 billion, a 2.9% decrease from the previous year, while net income fell 5.05% to $647 million. These declines are directly linked to the struggles in the Access segment and the margin pressures from the NGDV program. While the company’s ethical culture remains a long-term strength, it has not insulated Oshkosh from these short-term operational challenges.

Despite these difficulties, market sentiment remains cautiously optimistic. Oshkosh shares are currently trading at $149.86, with analysts setting an average price target of $166.36—a potential upside of 12.2%. This suggests that investors see the current setbacks as temporary and believe the company’s strong segments, especially Vocational, can drive a turnaround. However, recent company guidance has fallen short of Wall Street’s expectations, with delays and margin pressures in the NGDV program drawing scrutiny.

This uncertainty is reflected in the stock’s recent movements. After delivering a one-year total shareholder return of over 60%, Oshkosh shares have declined 6.3% in the past week. This volatility underscores the market’s focus on upcoming results and the effectiveness of plans to revive the Access and NGDV segments. While long-term performance has been rewarded, investors are now seeking evidence of near-term execution.

In essence, a strong ethical culture creates a foundation for success, but it does not guarantee immediate financial results. Oshkosh’s current challenge is to translate its cultural strengths and backlog into renewed growth and profitability. The market’s 12% upside target reflects confidence in the company’s potential, but recent declines signal a demand for concrete progress in overcoming operational hurdles.

OSK Stock Trend Snapshot

Ethics as a Competitive Advantage: The Moat in Practice

Oshkosh’s commitment to ethical business is a real asset, but its effectiveness as a competitive moat depends on the company’s ability to execute. The long-term financial rewards are clear: between 2020 and 2025, companies recognized for their ethical standards outperformed peers by 7.8%. This “Ethics Premium” demonstrates the value of trust and integrity in building lasting relationships with customers and suppliers, especially during challenging periods.

However, recent market reactions show that ethical leadership alone is not enough. Despite an impressive one-year return of over 60%, Oshkosh’s stock has recently fallen 6.3% in the last week, reflecting concerns over missed guidance, delays in the NGDV program, and the Access segment’s struggles. Investors are signaling that while a strong culture is valuable, they need to see tangible progress in addressing current challenges.

The crucial question is whether Oshkosh’s values—prioritizing people, perseverance, and ethical decision-making—will help the company navigate these difficulties more effectively than less principled competitors. Can this culture help manage supply chain disruptions or government contract delays with greater resilience? Will it enable the company to retain key talent and maintain customer loyalty during downturns? These are the real-world tests of the company’s competitive moat.

Balancing long-term advantages with the need for immediate results, Oshkosh’s position is mixed. Its ethical foundation is a powerful tool for building trust and attracting talent, which is especially important in a cyclical industry. However, operational challenges are currently overshadowing these strengths. The company’s future success depends on its ability to leverage its culture to drive a turnaround in the Access and NGDV segments, converting backlog into profit. The moat is in place, but Oshkosh must now demonstrate it can deliver results.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Is Agnico Eagle Mines (AEM) Performing Better Than Other Basic Materials Stocks This Year?

Is AC Immune (ACIU) Showing Better Performance Than Other Healthcare Shares This Year?

Is Sun Country Airlines (SNCY) Currently Considered a Top Value Stock?

3 Factors to Steer Clear of CAR and One Alternative Stock Worth Considering