DFP's 7% Return Encounters Financial Industry Beta Challenges as Discount Margin Tightens

Overview of DFP: A High-Yield Closed-End Fund

DFP stands out as a classic example of a high-yield closed-end fund (CEF). Its primary objective is to deliver total return, prioritizing substantial current income by holding a diversified mix of preferred stocks and other income-generating securities from both U.S. and international issuers. This targeted strategy shapes the fund's risk and reward characteristics, making it a potential choice for investors seeking income within a broader fixed-income portfolio.

Current Performance and Yield

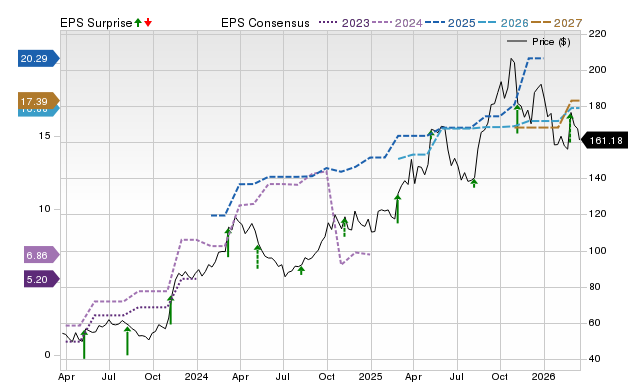

As of March 17, 2026, DFP shares closed at $20.93, providing an annualized forward yield of 7.00%. While this attractive yield is a key draw, it should be considered alongside the fund’s valuation. Currently, the shares are priced at a 7.13% discount to their net asset value (NAV) of $22.54. This discount is slightly narrower than the fund’s average 7.30% discount over the past year, indicating that shares are trading at a small premium compared to their typical discount range.

Portfolio Structure and Risk Considerations

Investing in DFP requires a careful evaluation of risk-adjusted returns. The current discount offers some downside protection, but the fund’s use of 37.38% effective leverage and its heavy allocation to the financial sector (over 25% of assets) introduce notable market risks. The portfolio’s average coupon rate is 7.35%, supporting its income potential, but the underlying securities are sensitive to shifts in interest rates and credit spreads.

Ultimately, DFP provides an enhanced income opportunity, but investors should be mindful of its volatility and the fund’s tendency to move in line with broader financial and credit markets.

Risk-Adjusted Returns and Portfolio Role

DFP’s risk profile is shaped by its price volatility and concentrated exposures. Over the past year, its share price fluctuated between a low of $18.20 and a high of $22.11—a swing of nearly 21%. The current price of $20.93 remains about 18% below the high, highlighting the potential for significant drawdowns. Such volatility is a crucial factor in assessing risk-adjusted returns, as it increases the fund’s overall risk relative to its yield.

The fund’s mandate requires that at least 80% of managed assets be invested in preferred and other income-producing securities. With more than a quarter of assets in the financial sector, DFP is highly sensitive to changes in interest rates and sector-specific credit events, which can impact valuations and spreads.

Geographically, DFP’s holdings span developed markets, including Canada, the UK, and France. While this global reach offers some diversification, it does not offset the fund’s core sector concentration. As a result, DFP’s returns are likely to move in tandem with other financial and high-yield credit assets. This correlation can provide some diversification against pure equity or government bond exposure, but it also means the fund may not serve as an effective hedge during periods of broad market stress.

In summary, DFP is best used as a tactical allocation within a fixed-income or alternative income segment, rather than as a core holding for capital preservation. Its high leverage amplifies both potential gains and losses, so careful portfolio positioning is essential to avoid excessive concentration risk.

Valuation Insights and Discount Dynamics

DFP’s valuation story centers on balancing its appealing yield, a moderate discount to NAV, and the inherent risks tied to credit and interest rates. The current 7.13% discount to NAV offers a potential margin of safety for disciplined investors, as the market is valuing the fund’s portfolio at a slight markdown. This discount could narrow if investor sentiment improves or if the fund continues to deliver on income expectations.

However, this discount is not without reason—it reflects some investor caution regarding the portfolio’s quality and risk management. The fund’s price-to-earnings ratio of 11.13 may appear reasonable, but for a CEF, it is less meaningful than the discount to NAV. The current discount is narrower than the 52-week average, and the fund’s historical discount has been more volatile, reaching as wide as 12.26% over the past year. This suggests that the current discount is not a deep value opportunity, but rather typical for the fund.

For investors, this means that while the discount provides some buffer, it is not wide enough to serve as a strong catalyst for price appreciation. The fund’s performance will be more influenced by the underlying portfolio and the consistency of its distributions than by a dramatic narrowing of the discount.

Key Catalysts, Risks, and Portfolio Implications

DFP’s investment outlook depends on several important factors. The main potential catalyst is the possibility of the current 7.13% discount narrowing. While there is limited room for further compression, improvements in the financial sector or renewed interest in preferred securities could drive the discount lower, adding a capital gain component to the fund’s total return alongside its 7% yield.

The primary risk is that the discount could widen if the financial sector underperforms, which would negatively impact both NAV and share price. The fund’s high leverage magnifies these moves, so in a risk-off environment, the discount could revert to its 52-week low of 12.26%, resulting in both capital losses and a wider valuation gap.

Given its sector concentration, DFP’s returns are likely to move in line with broader equity and credit markets, especially during periods of market stress. This limits its effectiveness as a portfolio hedge. However, its high yield and sensitivity to financial sector trends can make it a useful tactical tool. For example, if equity volatility rises but financials remain stable, DFP’s income could help stabilize returns. Still, its correlation with major indices like the S&P 500 means it may decline alongside equities in a broad sell-off, offering limited diversification.

Strategic Takeaways for Portfolio Managers

- DFP is best suited as a tactical, not core, holding due to its volatility and sector focus.

- Its primary appeal is yield enhancement, but allocations should be sized carefully to reflect its higher risk profile.

- The current discount offers some protection, but limited potential for further narrowing means distributions will drive most returns.

- Investors should monitor the discount and sector fundamentals closely, adjusting exposure if risks increase or if the discount widens significantly.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Wall Street experts predict HCI Group (HCI) may climb by 43.73%: Check this out before making your investment

Justin Sun Pitches TRON Inc as Cheaper Circle With MicroStrategy Model