Sweden's property boom masks a delicate gap in bid premiums across Stockholm

Swedish Housing Market: Signs of a Fragile Revival

Sweden's real estate sector is beginning to show renewed activity, but the heightened public interest points to a tentative and region-specific rebound rather than a widespread surge. Recent data places the market at a pivotal moment, with price increases fueling a spike in online searches that may reflect shifting attitudes among buyers and investors.

The most notable indicator is a pronounced monthly rise: in October, apartment values climbed 1.7% compared to September, marking the strongest monthly growth in twelve months. This aligns with a broader stabilization, as the national house price index recorded 1.61% year-over-year growth in Q3 2024 following six quarters of decline. However, when factoring in inflation, real house prices remained unchanged over the year, and the Riksbank's business survey indicates that Swedish households remain cautious. The recovery is still in its early stages and, in real terms, stagnant.

This delicate price movement has become a focal point in online search trends. Both public and investor interest have soared, with searches for "Sweden housing market" increasing by 120% in the past month. This surge is a direct reaction to the market's first clear upward shift in over a year. While heightened search activity signals strong attention, it also brings headline risk, as intense interest can amplify both optimism and anxiety, making the market more sensitive to news and speculation.

In summary, the Swedish housing market is stabilizing, but search data reveals a story of cautious optimism and localized strength. The 1.7% monthly price jump and the first annual increase in years are driving renewed interest, while the viral surge in searches underscores the fragile nature of the recovery. Every new data point and headline is closely watched, with the market poised for further shifts.

Regional Disparities: Where Activity Is Concentrated

While headline price figures paint a picture of recovery, actual transaction data reveals a more fragmented reality. There is a clear gap between national averages and the intense bidding wars in certain hotspots, even as overall household confidence weakens.

The most striking evidence of this divide comes from bid premium statistics. In March, Stockholm's average bid premium hit +4.8%, its highest since June 2022, reflecting fierce competition among buyers in the capital. Nationally, the average bid premium was only +1.1%. In many regions, such as Värmland and Kronoberg, final sale prices were more than 5% below the initial asking price. This creates a split market: Stockholm sees strong, competitive bidding, while much of the country remains a buyer's market with lower prices.

This regional divergence is also reflected in household sentiment. Expectations for price increases have dropped significantly: in January, 42% of buyers anticipated price rises in the coming months, but by December, that figure had fallen to 33%. This decline in confidence suggests that, despite some price stabilization, buyers are less willing to pay premiums.

Ultimately, the market's strength is uneven. Stockholm's robust activity lifts national averages, but most regions continue to favor buyers. The weakening sentiment among households adds vulnerability; if confidence erodes further, it could quickly undermine the competitive bidding that currently supports prices in the capital. For now, the market is marked by regional extremes and a delicate shift in psychology.

Interest Rates: The Key Driver of Market Change

The main force behind the market's tentative recovery is the Riksbank's transition from raising to lowering interest rates. For years, aggressive rate hikes pushed prices downward and triggered a significant correction. With the central bank now signaling rate peaks and potential cuts, the pressure is easing, and recent price gains reflect this new monetary environment.

Market participants are now focused on the Riksbank's upcoming policy meeting, which is expected to be a decisive factor for renewed confidence. The central bank's guidance on future rate cuts is crucial for a market that has been waiting for positive signals. Any change in its approach—whether slowing cuts, pausing, or refocusing on inflation—could quickly disrupt the fragile recovery. The surge in online searches about housing is a direct response to this anticipation, with every hint of policy change magnified in the public eye.

This sets the stage for a potential shift in momentum. The broader economic outlook is improving, with investment activity benefiting from renewed international interest and clearer pricing in 2026. This positive macro environment provides support, but the housing market's recovery remains uneven. National averages are rising, but the real action is concentrated in Stockholm's bidding wars. The Riksbank's next decision will determine whether this momentum spreads or stalls. For now, the central bank's policy meeting is the headline event that will shape the market's next move.

Key Indicators: Monitoring Search Trends and Market Signals

For investors, real-time signals extend beyond price charts to the search volume driving them. The viral buzz around Sweden's housing market means certain metrics will serve as early warnings for broader shifts in capital flows. Here are the main indicators to watch:

- Bid Premiums in Major Cities: Keep an eye on bid premiums in Stockholm and other urban centers. If these premiums consistently exceed +5%, it would signal that the recovery sentiment is spreading. The current peak of +4.8% in March shows strong competition, but the trend remains fragile. Sustained increases could create a cycle of rising prices and greater buyer interest, while a decline would indicate the bidding war is more speculative than sustainable.

- Riksbank Communications: Monitor the central bank's statements for any dovish shifts. The upcoming policy meeting is a major catalyst, and changes in guidance—such as pausing cuts or emphasizing inflation—could quickly impact confidence and market activity. The market is highly sensitive to these headline risks.

- Price Index vs. Transaction Volume: Watch for discrepancies between national price indexes and transaction volumes. If prices rise while transaction volumes fall, it suggests a fragile, speculative rebound driven by a few hot deals rather than broad demand. This scenario could lead to a volatile correction. While the national price index is stabilizing, underlying transaction activity remains inconsistent. If volume fails to keep pace with price increases, it signals that the recovery is vulnerable to shifts in sentiment.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

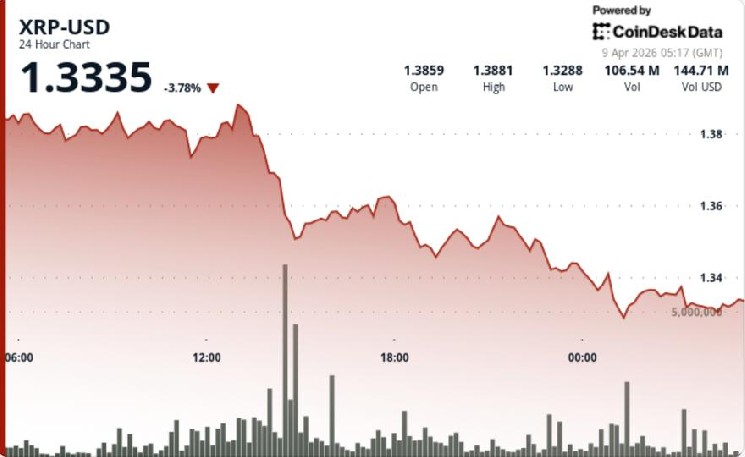

XRP slips 4% as selling pressure builds despite ETF inflows

Massive News: Cathie Wood Just Unloaded This Huge AI Semiconductor Stock